Gianluca Benigno Note that the New York Fed’s GSCPI, used for this Post on Forecasting Inflation Using the Naive Expectations Augmented Phillips Curvecan be independently used to predict inflation, such as Akinchi et al. “To what extent can improved GSCPI help reduce inflation” (February 2023).

First, both global supply and global demand factors are correlated with intermediate demand commodity PPI inflation, consistent with the global trade nature of the commodities in the index. Second, in addition to the supply component captured by the GSCPI, US-specific demand factors are also related to CPI inflation. Third, as expected, the GSCPI is more correlated with commodity CPI inflation than with headline inflation.

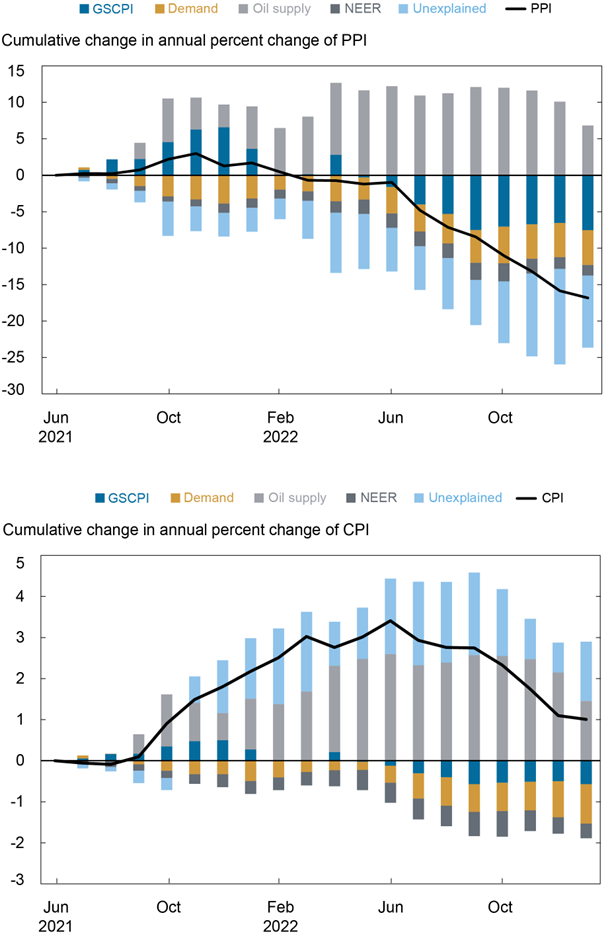

The chart below shows oil, supply chain stress and unexplained impacts.

It will be interesting to see how much oil contributes to upward inflationary pressures, with the GSCPI contributing in 2021 and turning negative in the second half of 2022. In other words, a large part of the current inflation is due to higher oil prices.While their methodology excludes inflation expectations, Benigno observed to me that the Michigan indicator is highly correlated with oil prices (see here).

BTW, this point should motivate people to try to de-correlate the inflation expectations measure I used with changes in oil prices to mitigate the multicollinearity problem in the regressions used in this paper postal.

{kind=link}

{kind=link}