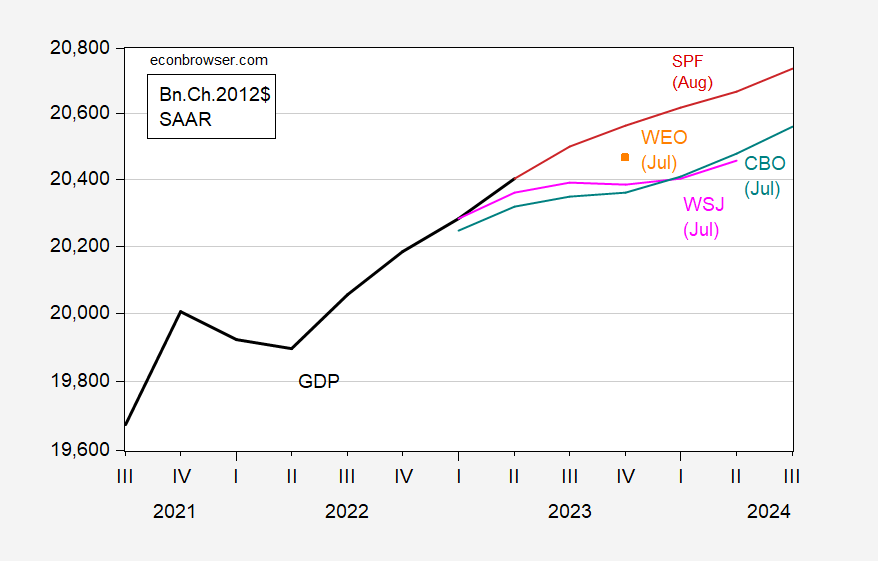

Contrary to July’s Wall Street Journal survey, the just-released survey of professional forecasters averages no negative GDP forecasts.

figure 1: GDP (black bold), August SPF (red), July WSJ survey (pink), CBO forecast (teal), World Economic Outlook (orange squares), all in billions. 2012 $SAAR. Sources: BEA, Philadelphia Fed, WSJ survey, Congressional Budget Office July Economic Outlook Update, IMF July World Economic Outlook Update, and authors’ calculations.

The SPF forecast is much higher than the WSJ forecast, in part because it incorporates the actual second-quarter advance forecast. Respondents to the Wall Street Journal’s July survey, as well as Congressional Budget Office and IMF staff, did not have advance estimates for the second quarter at the time of their forecasts.

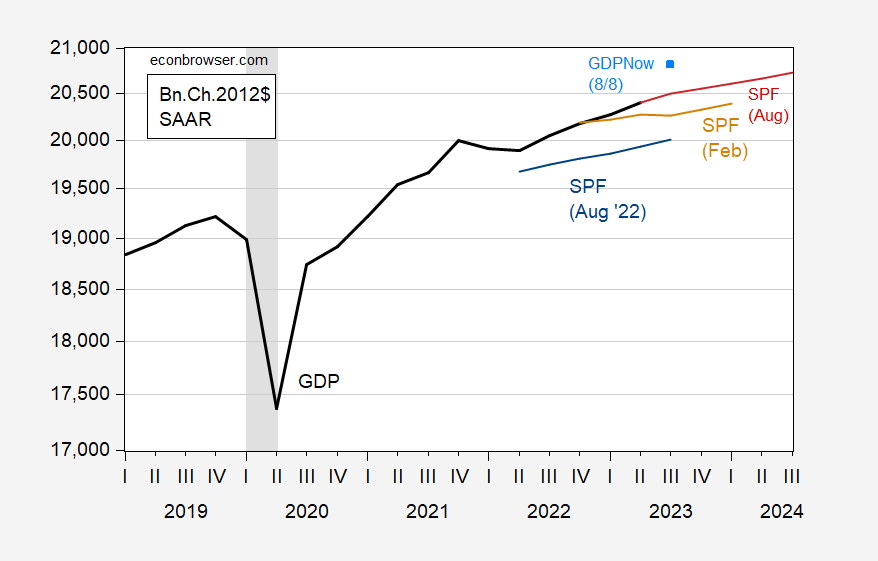

The August SPF indicated faster growth and higher production levels compared to the February SPF, which was again higher than the August SPF (albeit at a slower pace).

figure 2: GDP (black bold), Aug SPF (red), Feb SPF (tan), Aug SPF (blue), GDPNow is 8/8 (sky blue squares), all in billions. 2012 $SAAR. Recession peak-to-trough dates as defined by NBER are grayed out. Sources: BEA, Philadelphia Fed, Atlanta Fed, NBER, and authors’ calculations.

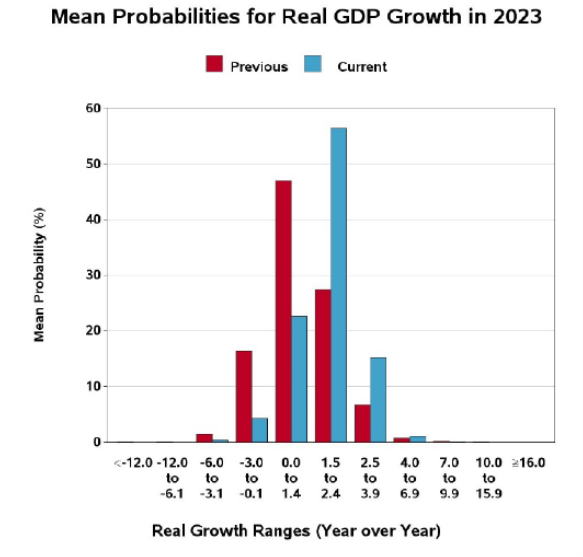

Since the survey in May, the distribution of year-on-year growth rates has shifted significantly upward.

source: SPF (August 2023).

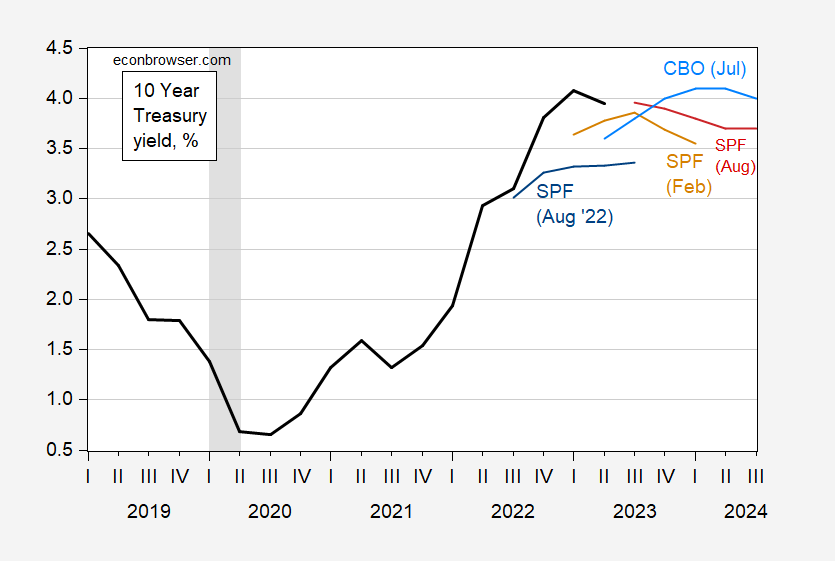

Note that while economic growth has proven resilient, forecasted 10-year yields have risen (though still below the CBO’s 2024 forecast).

image 3: 10-Year Treasury Yield (bold black), Aug SPF (red), Feb SPF (tan), Aug SPF (blue), CBO (sky blue), all in %. Recession peak-to-trough dates as defined by NBER are grayed out. Sources: BEA, Philadelphia Fed, CBO July Economic Outlook Update, NBER, and authors’ calculations.

{kind=link}

{kind=link}