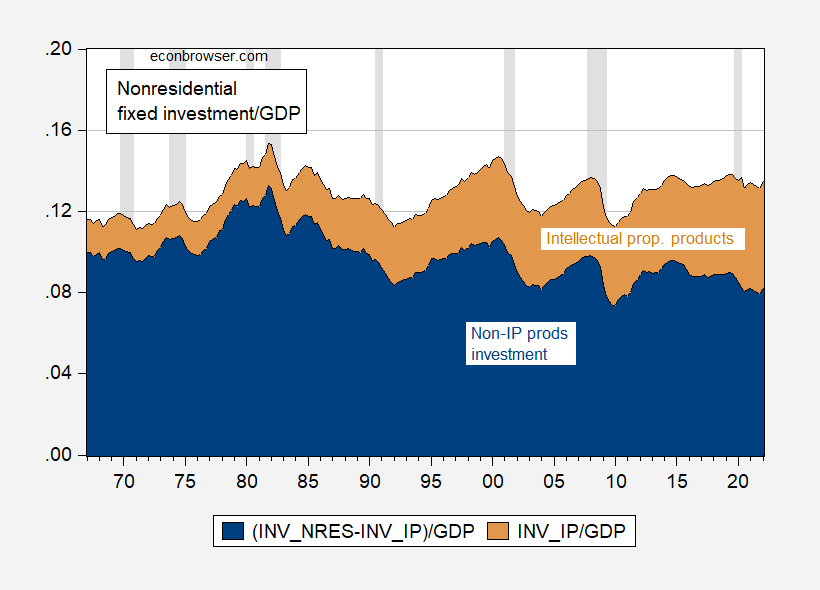

An interesting aspect of the current recovery is the relatively small rebound in nonresidential fixed investment.

figure 1: Share of non-residential fixed investment in nominal GDP in non-IP products (blue) and investment in IP products in nominal GDP (tan), SAAR. The NBER uses shades of grey to define the peak and trough dates of the recession. Source: BEA, author calculations.

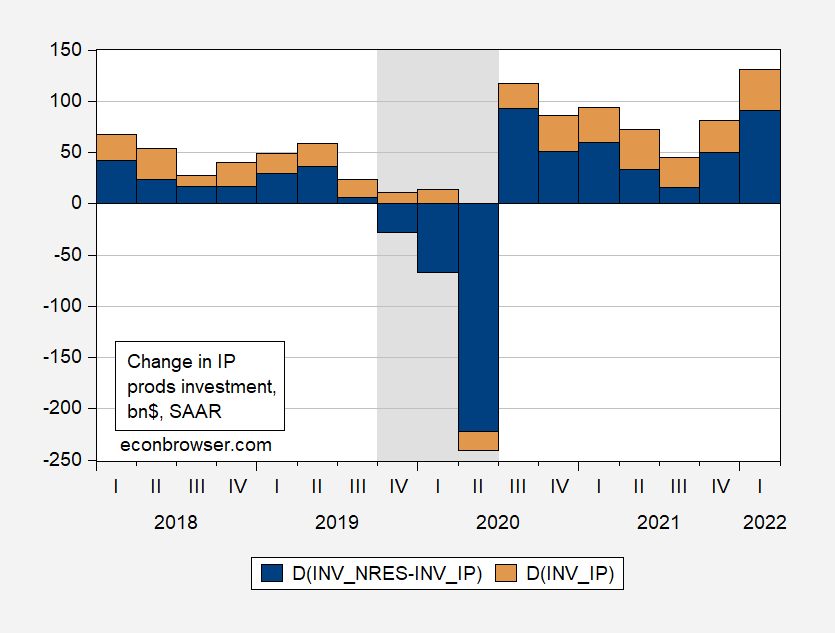

Note that the decline in nonresidential investment was small and the rebound was relatively small. Perhaps more interestingly, the share of IP product investment has increased over time. Investment in IP products has grown in importance in terms of nominal GDP growth – before Covid-19. In Figure 2, I show the q/q change, but the share of GDP impact shows the same pattern.

figure 2: Quarter-on-quarter change in non-IP product non-residential fixed investment (blue) and IP product investment (tan), SAAR. The NBER uses shades of grey to define the peak and trough dates of the recession. Source: BEA, author calculations.

Note that I’ve used BEA’s aggregated family of IP products in these figures (components are software, R&D, entertainment, and literary originals).For more information on IP product investment heterogeneity, see Fixler and Francisco (2022).

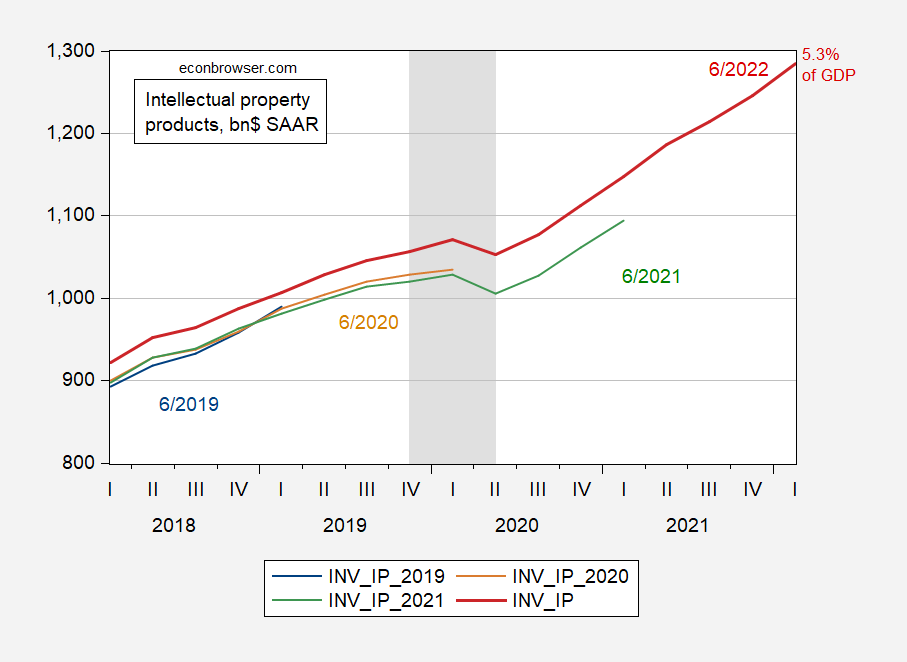

Now, two implications can be drawn from this observation. The first has to do with what the final Q1 and Q2 GDP numbers might end up looking like. In some cases, intellectual property investment has been revised upward significantly.

image 3: IP product investments released in June 2019 (blue), June 2020 (tan), June 2021 (green) and June 2022 (red bold), all in billions of dollars, SAAR. The NBER uses shades of grey to define the peak and trough dates of the recession. Source: BEA, author calculations.

Not only is the WHO series revised up with the July 2021 report’s baseline revision (about a quarter of a percentage point of GDP), but – importantly for GDP growth rates – Variety Investments in intellectual property products typically increase.Therefore, I think GDP growth is May be revised up in 2022 Because GDP figures are benchmark-corrected.

The second observation has to do with the impact of tightening monetary policy. Views that intangible capital investments are less sensitive to changes in interest rates (e.g., Cruzer and Eberly, 2019) means that monetary policy may need to be tightened more than otherwise to achieve the stated goal of reducing aggregate demand.

{kind=link}

{kind=link}