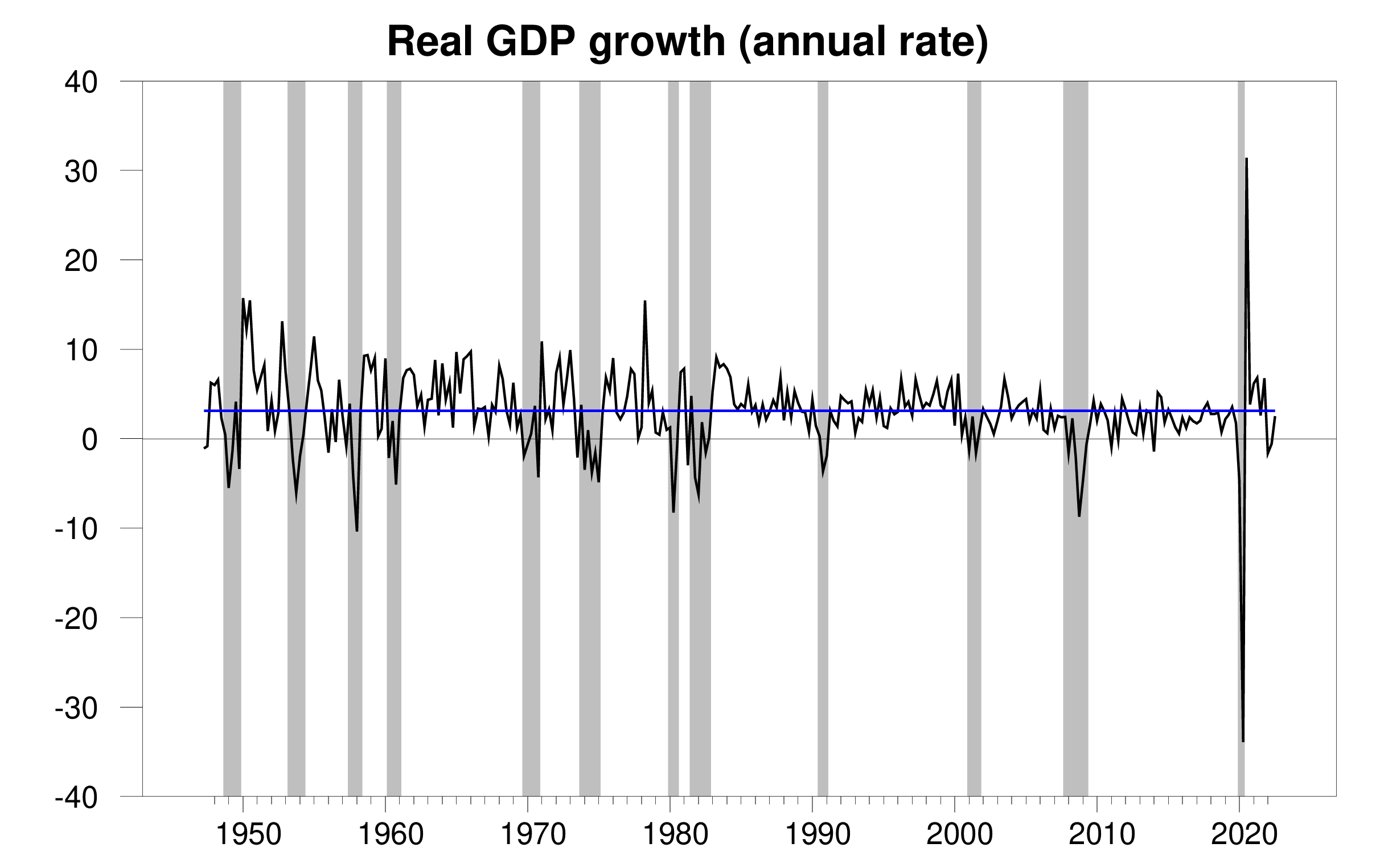

This Bureau of Economic Analysis Announced today, the seasonally adjusted third quarter U.S. real GDP growth rate was 2.6%. This is close to the historical average (3.1%) and is a welcome sequel to the two quarters of GDP declines we started at the beginning of the year.

Real GDP annual growth rate, 1947:Q2-2022:Q3, blue is the historical average (3.1%). Calculated as 400 times the natural log difference from last quarter’s GDP.

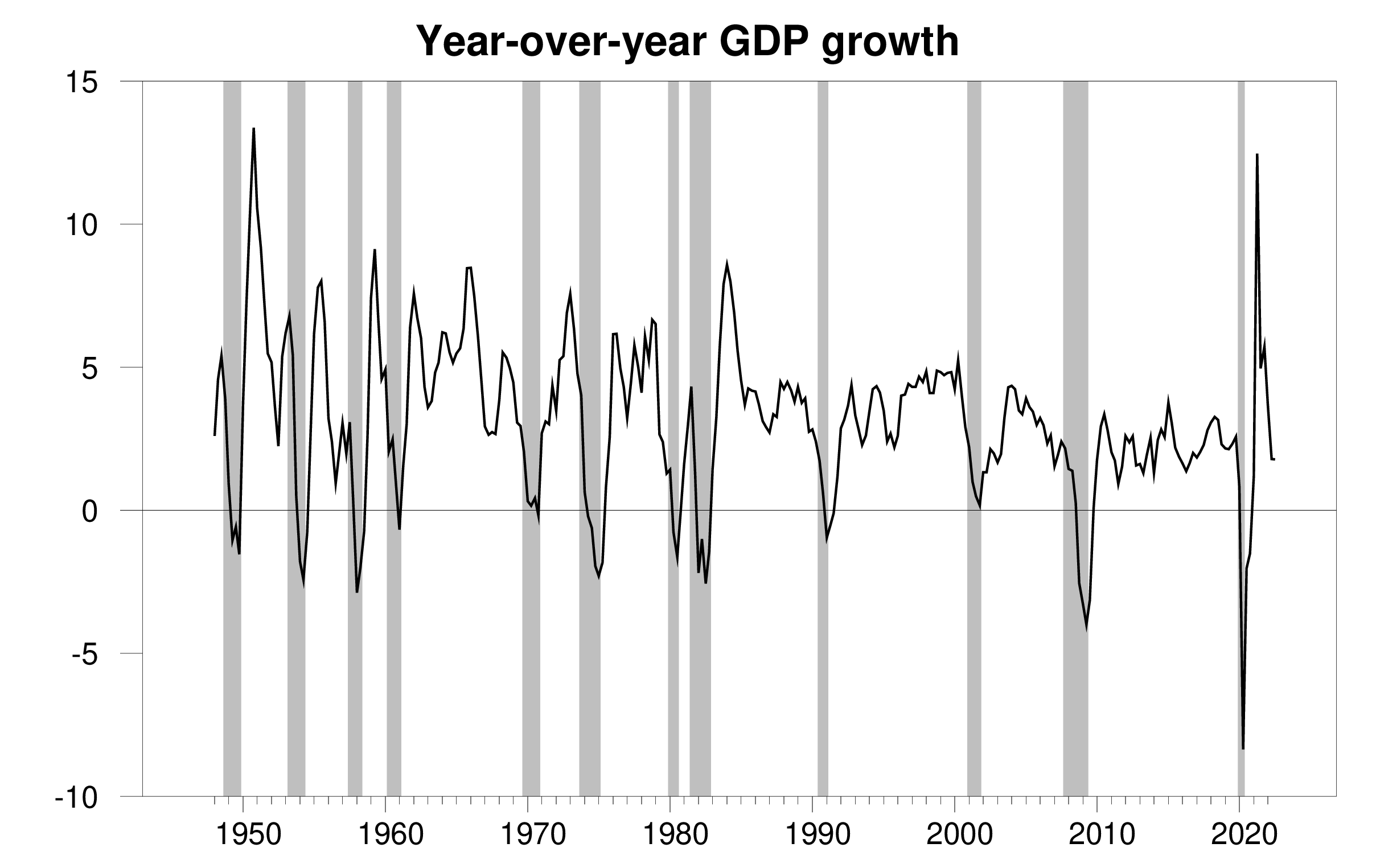

Here’s what the data looks like when plotted against annual growth rates.

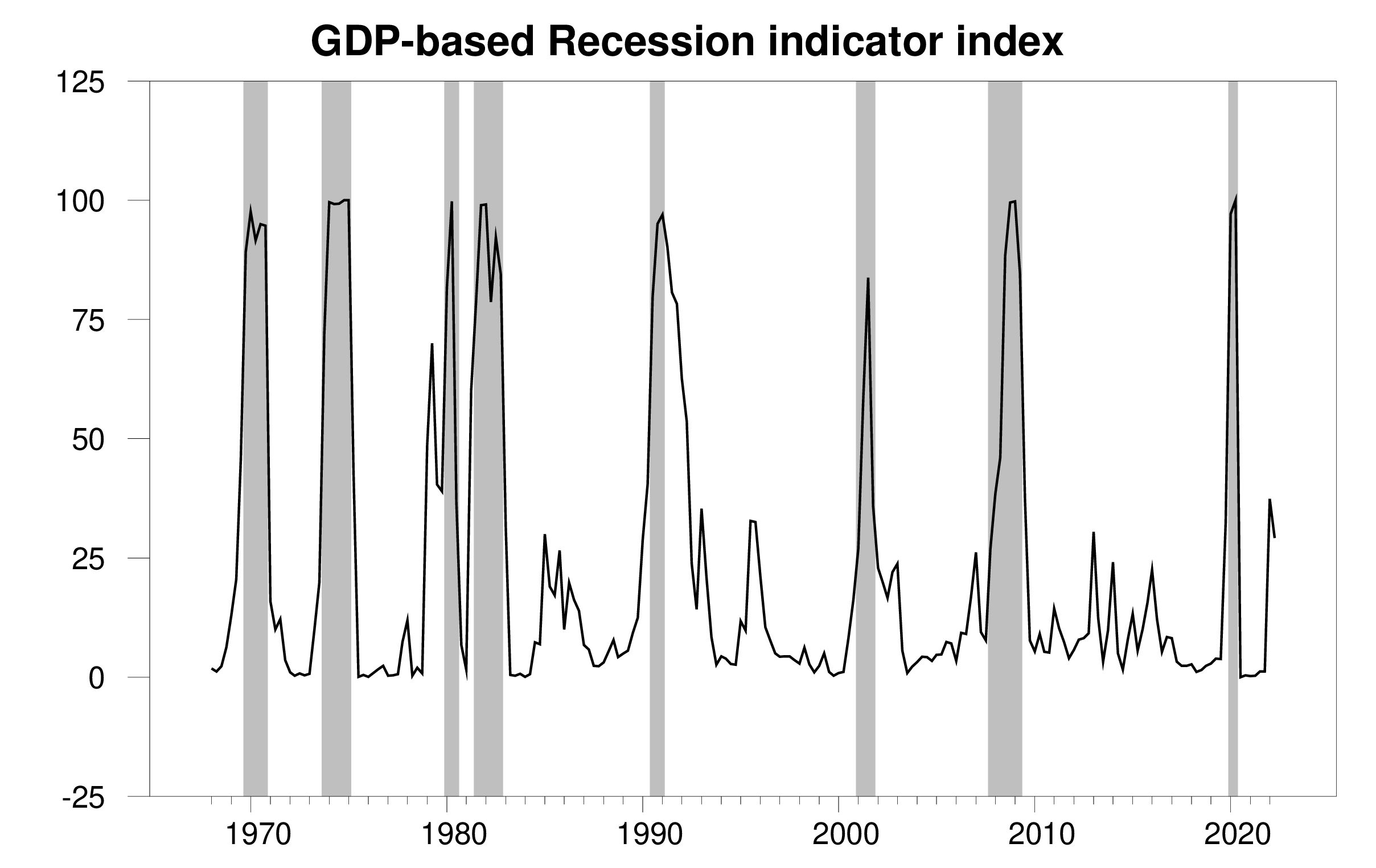

new data help Economic Browser Recession Indicator Index It fell slightly to 29.2%. This is an assessment of the economic situation in the previous quarter, the second quarter of 2022. The index takes into account the fact that growth was positive in the third quarter to refine its assessment of the state of the economy in the previous quarter.When Marcelle Chauvet and I The index was first developed 17 years ago, we announced that we would only declare a recession when the index rose to 65% (see pages 14-15) Our original paper).

The index itself is never revised, although quarterly updates and revisions to GDP allow for an improved assessment of the state of the economy a few quarters ago and the value of the index that we publish in real-time based on the initial GDP report. If subsequent data sends the real-time indicator above 65%, we will use the full revised historical data available for that date to announce the date when the recession is likely to begin.it’s here Economy browser Since the data has been released in real-time for the past 17 years, we have followed this procedure and have successfully determined the start and end dates of two recessions since we started this blog.

GDP-based recession indicator index. The plotted values for each date are only based on publicly available GDP data as of the quarter following the date shown, the last date shown on the chart is 2022:Q2. The shaded areas represent NBER’s decline dates, which were not used in any way to construct the index.

The recent rate hike sent the U.S. housing market down rapidly. The decline in new home construction reduced 2022:Q3 annualized GDP growth by 1.4%.

Another channel through which higher interest rates can slow GDP growth is a stronger dollar, which dampens U.S. exports and encourages U.S. imports. But surprisingly, exports rose while imports fell in the third quarter, boosting annual GDP growth by 2.8%. Nearly half of the growth in exports came from oil and products, as the U.S. filled the gap created by disruptions to Russian shipments. supply chain issues Probably the reason for the drop in imports. With headwinds from a stronger dollar, it’s hard to see trade continuing to make a huge positive contribution.

Mild weather eased some Challenges facing Europe At least for now, Russia is cutting off gas. However, the European energy situation in 2023 is still severe, dragging down the European and even the world economy. China’s continued efforts to contain the Covid-19 outbreak is another very serious headwind for global economic growth. Combined with the ongoing impact of monetary tightening, the likelihood of a recession next year is clear.

So while third-quarter GDP growth was welcome, our small economy watcher Still very worried.

{kind=link}

{kind=link}