Don’t pay too much attention to headline changes in employment.

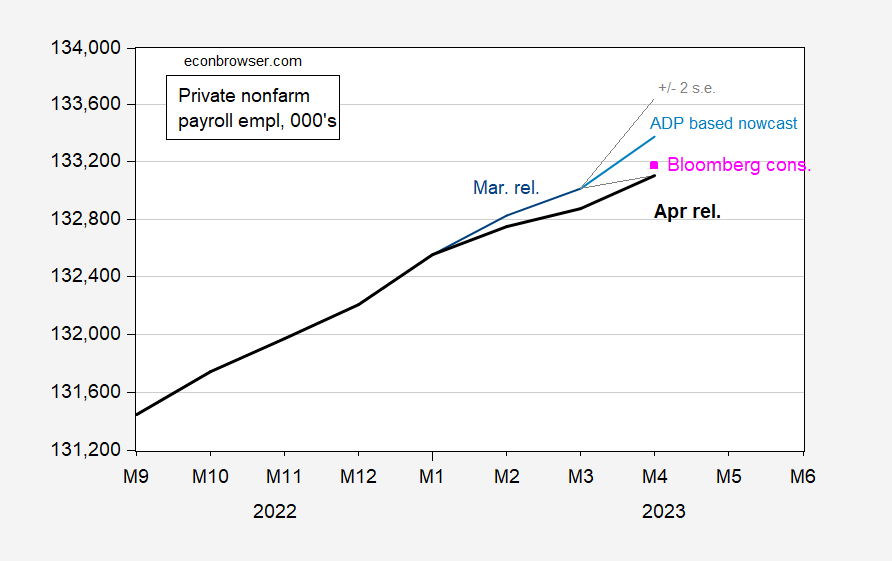

The jobs report focused on the net change in April (which was higher than market expectations), but a more nuanced assessment pointed to a downward revision. The following two graphs highlight the difference between growth rates and levels. The first image shows the difference.

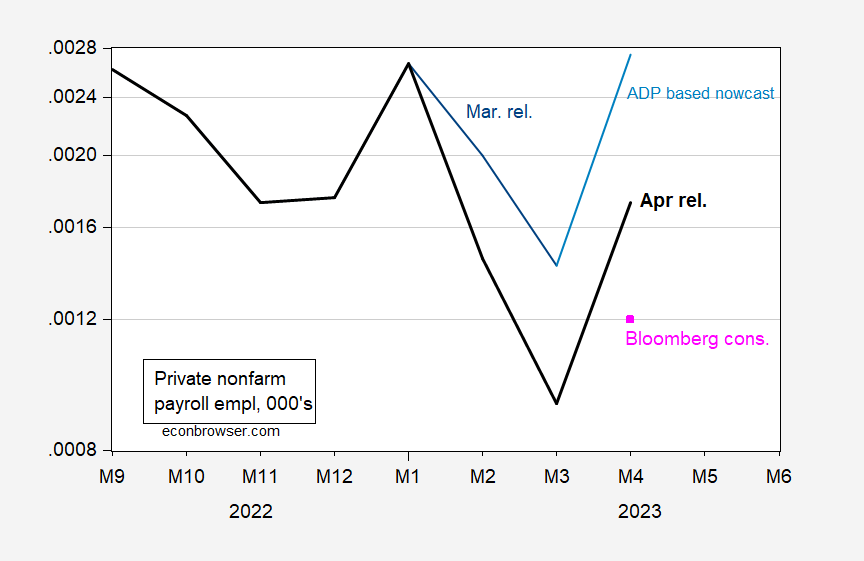

figure 1: Private nonfarm payrolls month-on-month growth, April release (bold black), March release (dark blue), Bloomberg consensus 5/5 (pink squares), and authors’ ADP-based nowcast (sky blue), All calculations are log differences. Source: BLS via FRED, Bloomberg, author’s calculations.

The actual change in private NFP growth exceeded the Bloomberg consensus relative to the unrevised March. In that sense, the announcement was surprising. (mine Nowcasting based on ADP data Far beyond reality. ). The actual m/m change is 0.17%, compared to 0.12% for Bloomberg and 0.27% for the ADP-based nowcast.

The previous months were revised downwards (shown by the black line). At the level, the situation is completely different. Second picture:

figure 2: Private Nonfarm Payrolls, April release (bold black), March release (dark blue), Bloomberg consensus of 5/5 (pink squares), and authors’ near-term forecast based on ADP (sky blue) +/- Two standard errors (gray line). Source: BLS via FRED, Bloomberg, author’s calculations.

Figure 2 shows that while the April change in private NFP was a surprise, the actual level was lower than implied by the Bloomberg consensus (assuming no revisions in the prior month – we don’t actually know what the forecasters think about this).

ADP-based nowcasts were reduced by 0.206% (274,000), of which 0.105 (139,000) were corrected.

Clearly, net job creation is slowing, with the 3-month moving average falling to 182k/mo from 271k/mo in January.

{kind=link}

{kind=link}