GDPNow was down slightly on a revised basis in Q3 (4.9% SAAR), and GS was about the same (3.2%).

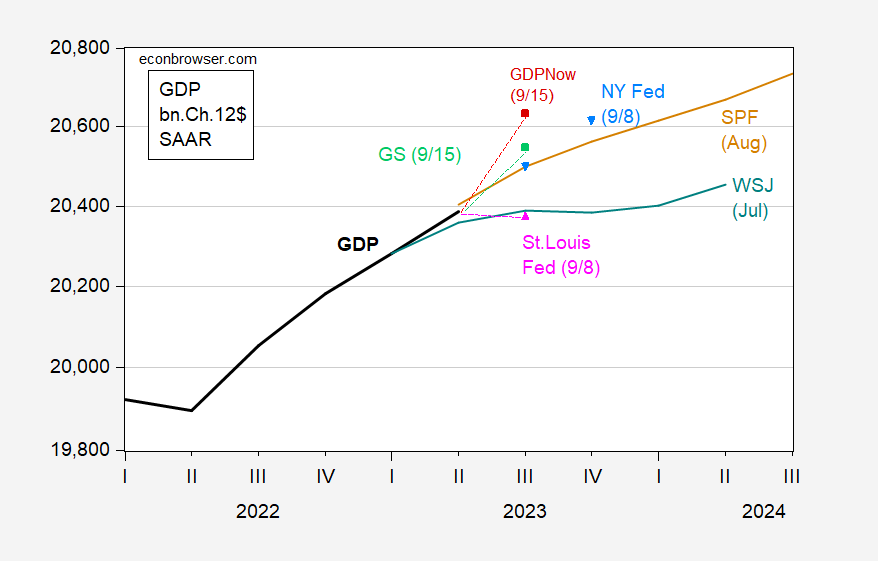

figure 1: GDP (bold black), Professional Forecaster Survey median (tan), Wall Street Journal July average (cyan), GDPNow 9/15 (red square), Goldman Sachs 9/15 (light green square), St. Louis Fed Economic News Index 9/8 (pink triangle), New York Fed Live Forecast 9/8 (light blue triangle), all in billions of 2012 SAAR dollars. Source: BEA 2023Q2 Second Release, Philadelphia Fed, Atlanta Fed, St. Louis Fed via FRED, Fed.

The shift in the July WSJ report (prepared before the early release of Q2 2023) and the August SPF report (prepared after the early release of Q2 2023) highlights the improved outlook. Both levels and growth rates have risen sharply (the Congressional Budget Office’s July forecast, compiled in June, is close to the Wall Street Journal’s July forecast).

Although the Atlanta Fed’s immediate forecast is about 5.7% lower than the SAAR, it is still above the median SPF, as is the GS tracker.

An unexpected rise in industrial production in August (+0.4% month-on-month versus 0.1% Bloomberg consensus) further supported prospects for continued growth.

{kind=link}

{kind=link}