Oil prices have doubled from a year ago and could rise even more if the amount of Russian oil entering world refineries falls sharply. This is the first in a two-part series on what these events could mean for the U.S. economy. Today I’ll focus on the effect on inflation, and in a follow-up article I’ll discuss the effect on real GDP.

Oil prices had risen sharply ahead of Russia’s intentional invasion of Ukraine. The factors behind the earlier rise are similar to those behind many other price surges: Demand is recovering faster than production.

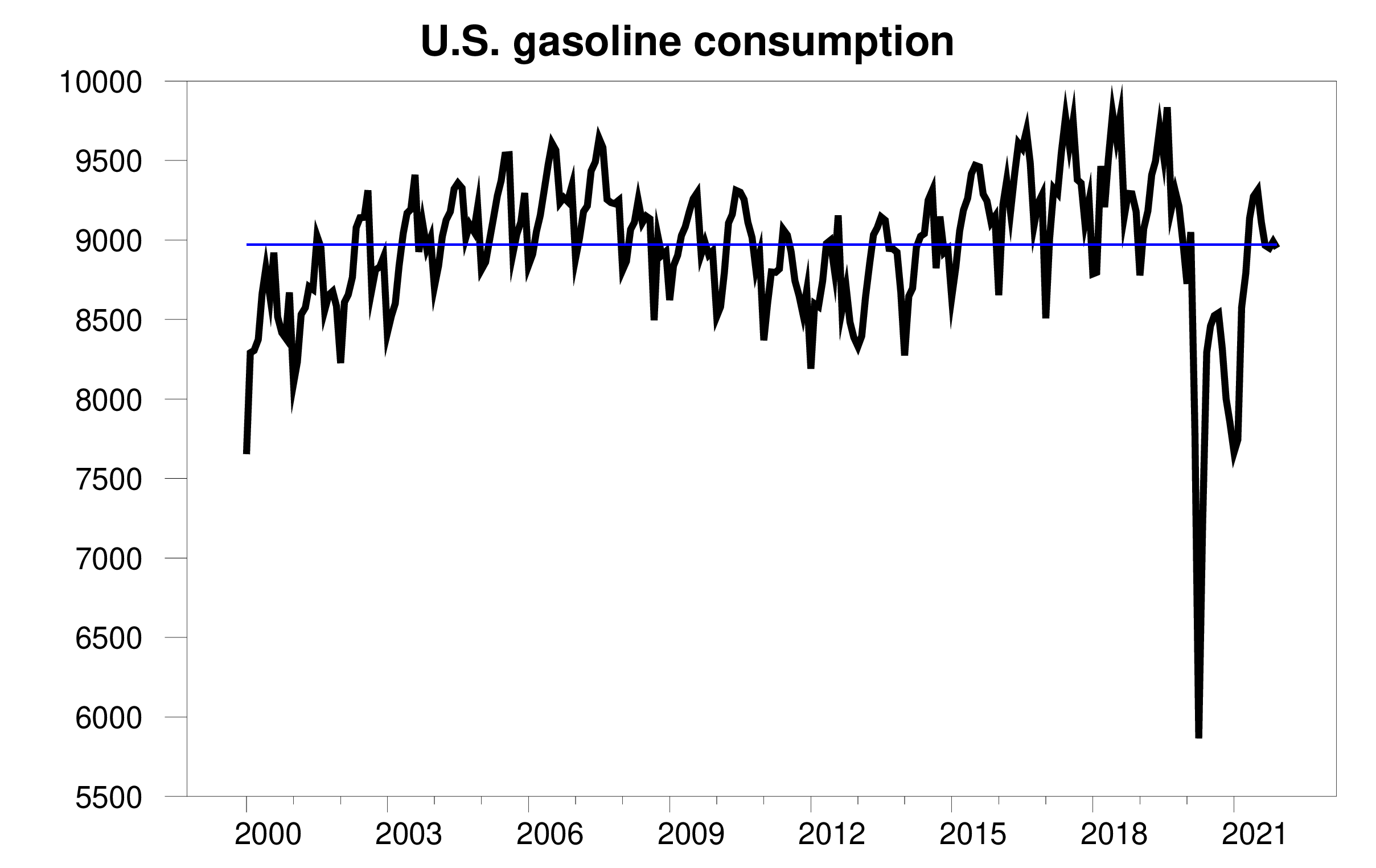

The graph below plots an estimate of monthly gasoline consumption in the United States. The usual seasonal patterns were severely disrupted by COVID. But by December, U.S. gasoline consumption had recovered to December 2019 levels. If gasoline prices do not rise significantly, I expect strong seasonal increases in gasoline demand this spring and summer.

Monthly supply of U.S. finished motor gasoline products in thousand barrels per day from January 2000 to December 2021. source: EIA A horizontal line drawn with December 2019 values.

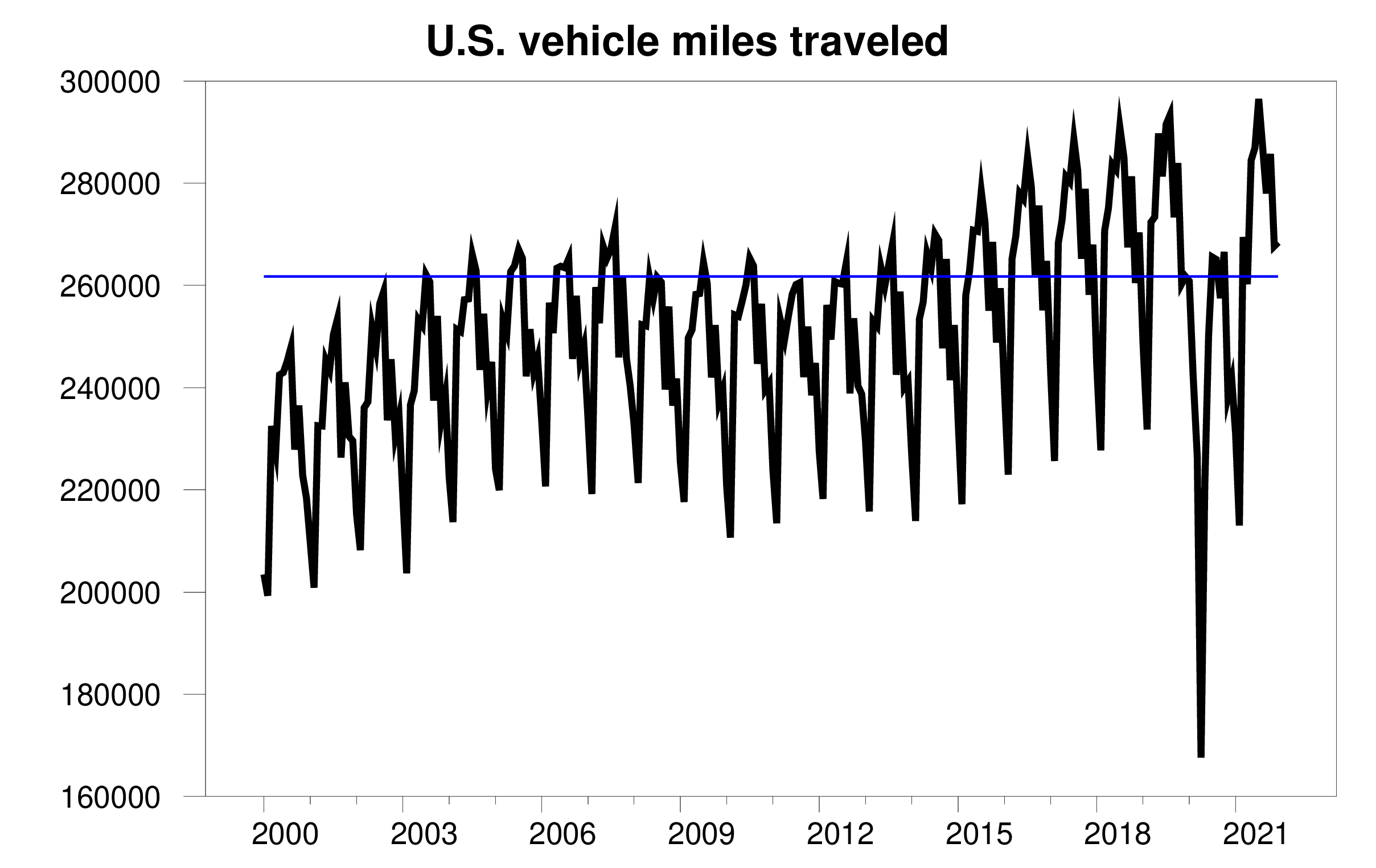

The same pattern appears in estimates of the number of vehicles on the road based on the miles Americans drive. Compared with two years ago, it increased by 2.5%.

Monthly vehicle miles driven in the United States, in millions of miles, from January 2000 to December 2021. source:

Fred. A horizontal line drawn with December 2019 values.

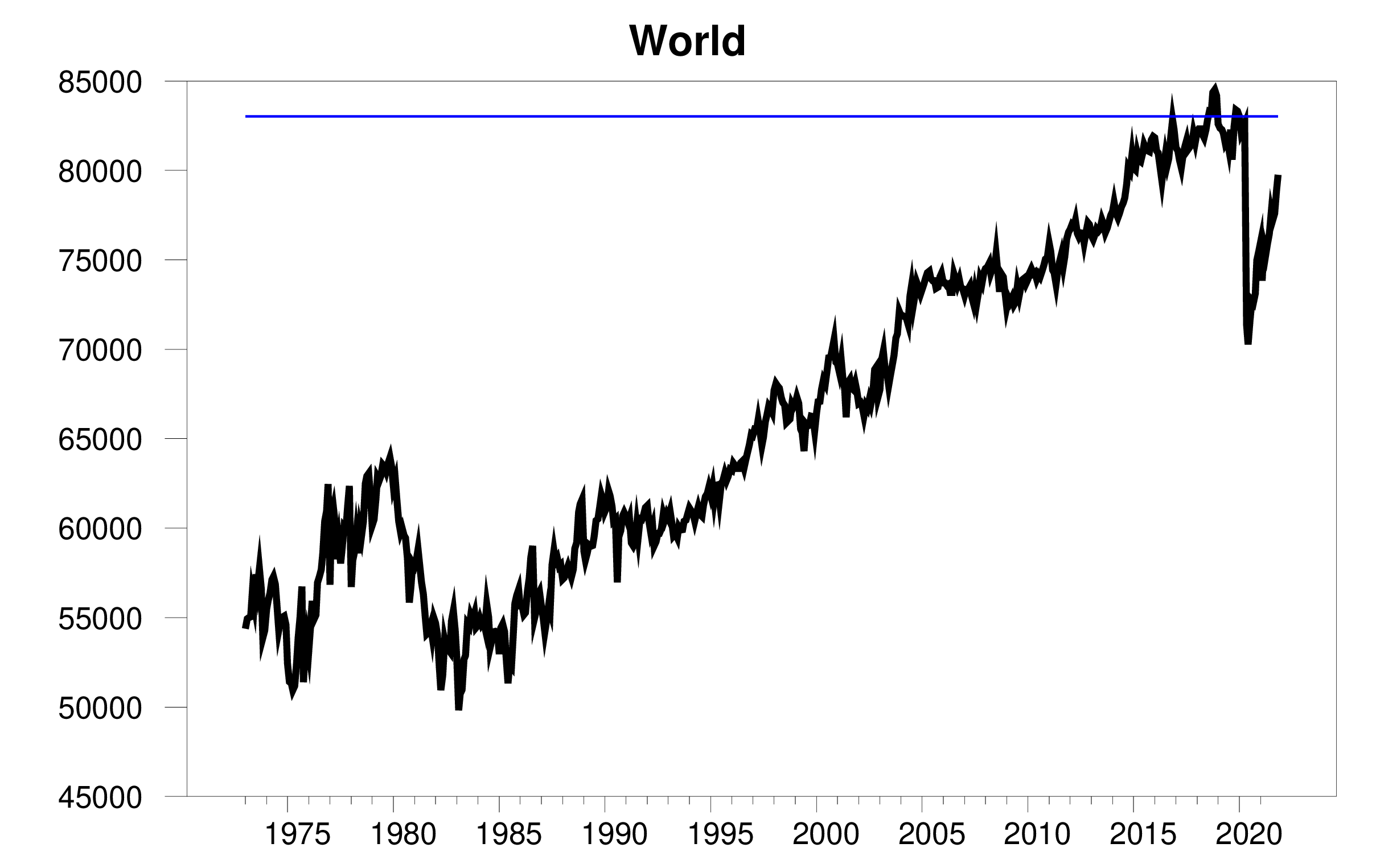

While demand may have returned to pre-COVID levels, supply has not. Even before any developments in Ukraine, world crude oil production in November was 3.3 mb/d below the level at the beginning of 2020.

Monthly world crude oil field production from January 1973 to November 2021 in thousands of barrels per day. source: EIA. A horizontal line drawn with January 2020 values.

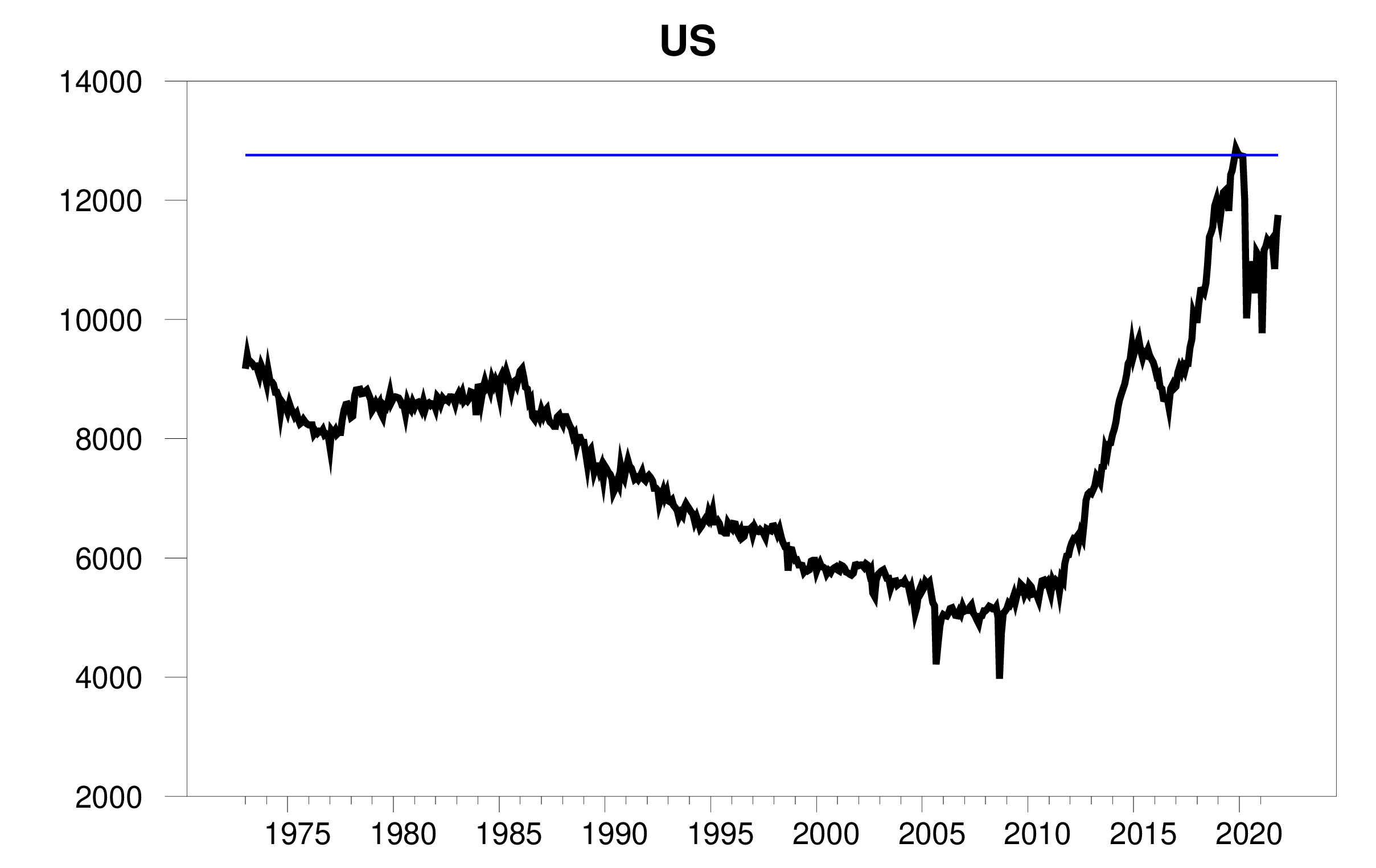

The U.S. provides one-sixth of total global pre-COVID crude oil production, but accounts for nearly one-third of the world’s deficit relative to pre-COVID today. US production remains 1 mb/d below the level at the beginning of 2020.

U.S. monthly crude oil field production, measured in thousands of barrels per day, from January 1973 to November 2021. source: EIA. A horizontal line drawn with January 2020 values.

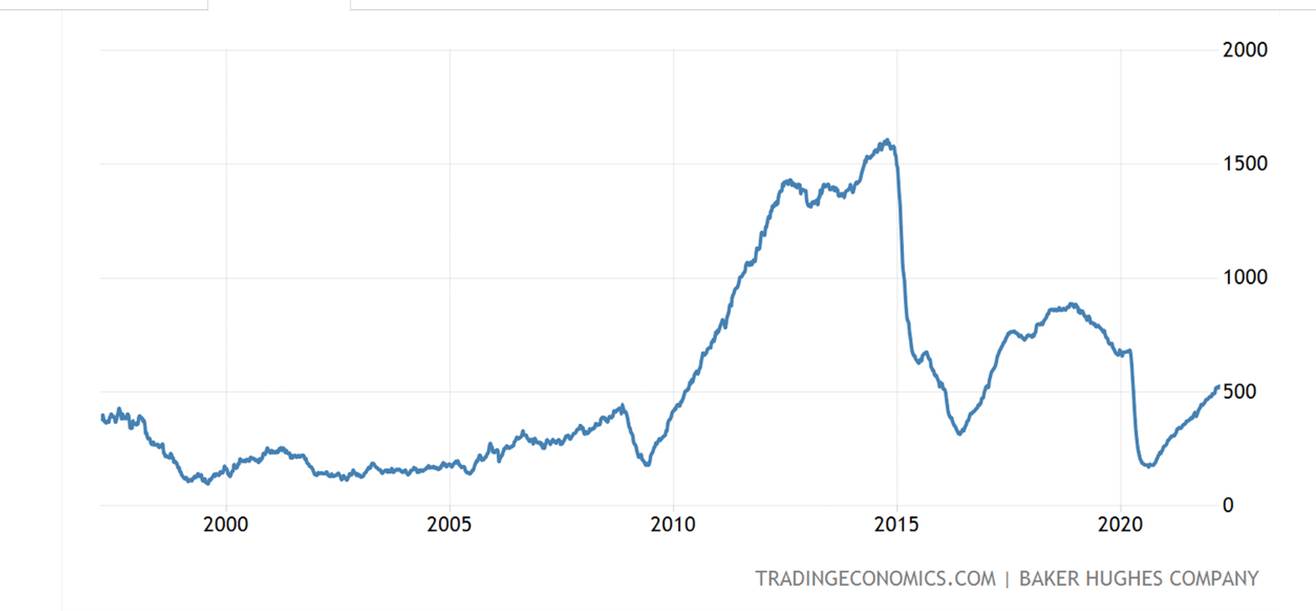

A big part of the story is that it’s easier to take something apart than to put it back together.This negative oil prices April 2020 marked the end of some enthusiasm for U.S. shale oil production, followed by a collapse in lending and drilling. Higher oil prices have been gradually but steadily restoring resources. This process will continue even if recent prices do not exceed a hundred dollars a barrel, but it will take time. Perhaps by the end of summer, U.S. production will return to levels seen in early 2020.

Baker-Hughes counts the number of active rigs in the United States on a weekly basis. resource: trade economics.

Demand is growing faster than supply, which has led to higher oil prices. That doesn’t necessarily mean more inflation, some economists argue. We don’t need to see inflation in the overall price level if the rise in the price of petrodollars is matched by the fall in the dollar price of other goods or services. But in practice, it often takes unusual events to cause the prices of many goods and services to actually drop. If oil prices rise and other prices don’t fall, it means overall inflation. For this reason, if the dollar price of oil rises but the dollar price of all other commodities does not change, it is sometimes useful to consider a counterfactual to calculate the inflation rate as a summary of the direct contribution of oil prices. inflation.

In 2019, the market value of U.S. crude oil production and imports was equivalent to about 2% of GDP. This suggests a quick and dirty rule for obtaining approximate answers to the hypothetical questions above. If we multiply the percent change in crude oil prices by 0.02, this should give us a rough idea of what inflation would be if changes in crude oil prices were the only source of inflation.This is the same as rough rule of thumb Federal Reserve Chairman Jerome Powell has said that a $10 increase in oil prices (about 10% at current prices) would lead to a 0.2% increase in inflation.

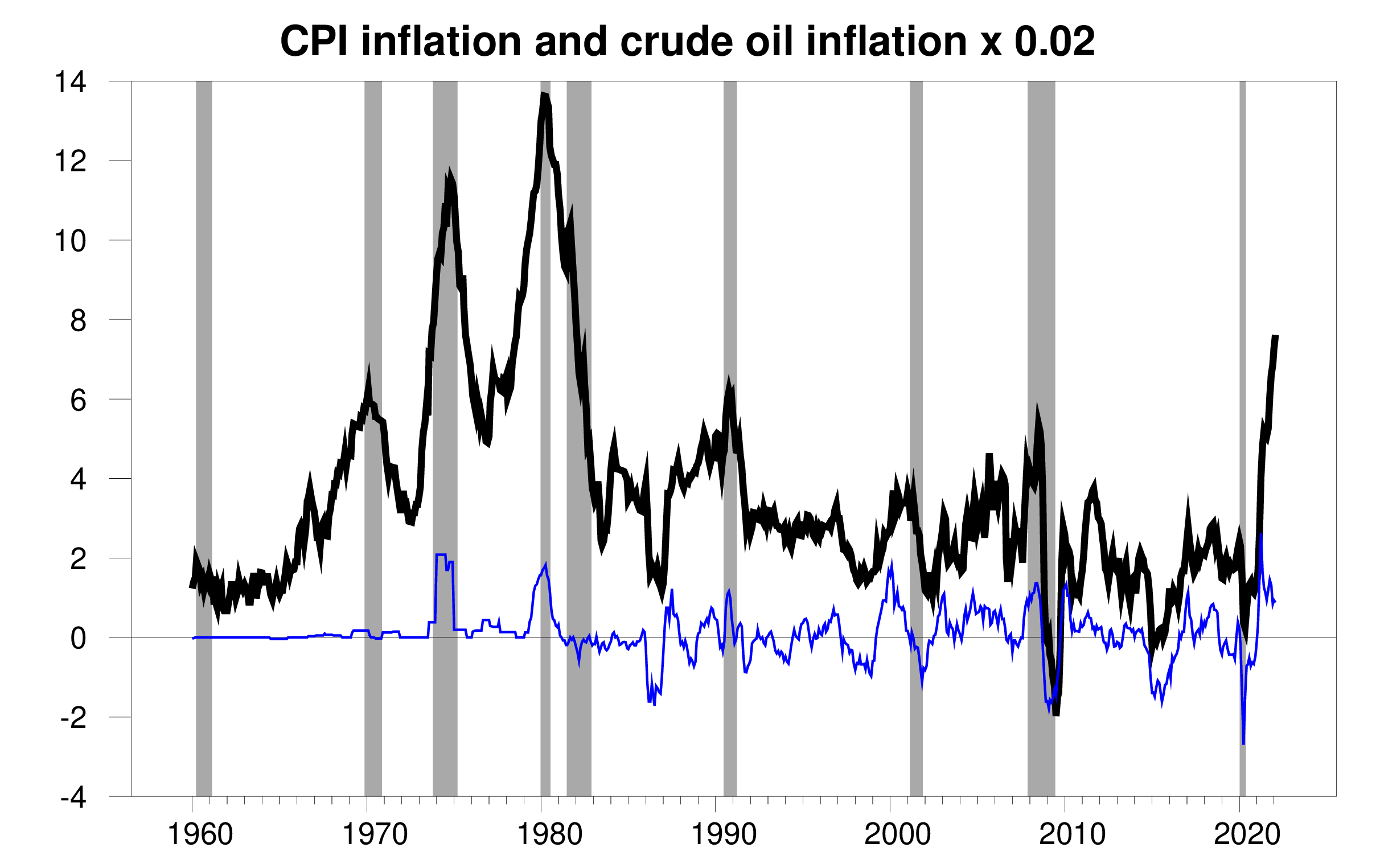

I use the approximation in the graph below to calculate the direct contribution of oil prices to US inflation each month since 1960. This quick calculation shows that oil contributed about two percentage points to the inflation surge in 1974 (after the OAPEC oil embargo) and 1980 (after the Iranian revolution). Oil contributed 2.6 percentage points to U.S. inflation in the 12 months to April 2021.

100 times the natural logarithmic year-over-year change in U.S. CPI (black), and 2 times the year-over-year change in the U.S. dollar price of WTI crude oil (blue), monthly, from January 1960 to February 2022 moon.

In the 1970s, blue oil’s contribution was a step-up and step-down function – it rose when oil prices rose and zeroed when prices stopped rising. But Black’s actual inflation path doesn’t follow a buck-boost function. Instead, inflation appears to rise to new higher levels with each spike in oil prices. Monetary policy in the 1970s essentially sanctioned a temporary spike in inflation, turning it into a persistent trend. The chart below shows two indicators of monetary policy error that led to this. The graph above plots real interest rates, calculated as the difference between the nominal federal funds rate set by the Federal Reserve and the year-over-year inflation rate as measured by the CPI. According to policy provisions such as the rules proposed by John Taylor, the real interest rate indicator plotted here should increase when inflation rises to bring inflation back to the lower target value. For much of the 1970s, huge negative real interest rates were an indicator of Fed overstimulation. The bottom panel provides a second indicator that plots the growth rate of the money supply as measured by M2. The surge in currency growth coincided with the two oil price surges of the 1970s and helped these fluctuations spread into more general and persistent inflation.

Above: Nominal federal funds rate for the given month minus 100 times the log change in CPI over the past 12 months.Bottom panel: 100x log year-over-year change M2.

Both indicators also sent a very clear signal that the Fed also went too far last year.

The Fed’s view is that last year’s price surge was the result of a temporary supply issue, as the developments I’ve described in the oil market are an example. They (like me) hope that we will see significant progress on these supply challenges in the coming months. That sentiment has prompted the Fed to plan to gradually ease the gas as the year unfolds.

But given the tragic turn of events in Europe, supply problems could get worse before they get better. This will make the Fed’s job more difficult.

{kind=link}

{kind=link}