After surging to $130 a barrel, oil prices have retreated to levels seen before Russia’s invasion of Ukraine.Russian oil may Finding buyers despite sanctionsand American production resume. But the situation is still very uncertain, and the possibility of a major disruption in the amount of Russian oil entering the world’s refineries is very high.in my previous post, I examine the reasons for the rise in oil prices that had occurred before the invasion, and discuss the impact on U.S. inflation. Today, I’ll comment on the likely impact of further supply disruptions on real US GDP.

April 2022 crude oil futures contract prices, since barchart.com.

Russia accounts for 13% of the world’s crude oil field production and 17% of the world’s natural gas production. While natural gas is a relatively localized commodity, oil is easily transported. Although different grades of crude oil are sold at different prices, broadly speaking, this is a world oil market with a single world price. Production disruptions anywhere in the world can change prices for everyone in the world. What would happen if the US and the rest of the world suddenly had to reduce our oil consumption by 13%?

The total retail value (including taxes) of refined petroleum products sold in the United States accounts for about 4 percent of US GDP. 13% of 4% is (0.13)x(0.04) = 0.005, or half of 1%. Thus, the dollar value of a 13% reduction in the use of petroleum products is only half of 1% of GDP. By contrast, in a typical U.S. recession, real GDP is 5% below trend — 10x. Additionally, energy’s share of value in the U.S. economy has been declining over time, leading some to conclude that we are less vulnerable to supply disruptions today than we were 40 years ago.

Above: Dollar value of consumer purchases Energy Goods and Services as a percentage total consumer spending, monthly, January 1959 to January 2022.Bottom panel: 100 times the natural logarithm of the ratio West Texas Intermediate crude oil spot price to the whole consumer price index.

But the share of spending has not steadily declined. When the relative price of oil rose rapidly—such as in the 1970s, the share of spending rose. This is a result of the low price elasticity of demand for oil. If you buy the same number of gallons of gas this month as last month, despite doubling the price of gas, your share of spending on gas will double. If Russian oil production were to decrease significantly, we would see a significant increase in prices and a higher share of spending. When calculating the economic value of lost oil, which share should we use – the share before the supply disruption, or the share after?

a recent paper Baqaee and Farhi (2019) developed a method to deal with this problem, and a paper by Bachmann, Baqaee and many others Apply these insights to the current situation in Europe. They analysed the consequences of Germany’s complete cessation of oil and gas imports from Russia. They concluded that the cost to the economy would be 0.5% to 3.0% of GDP, depending on the extent to which Germany could substitute. Even the upper end of the range is manageable and less output than in a typical recession.

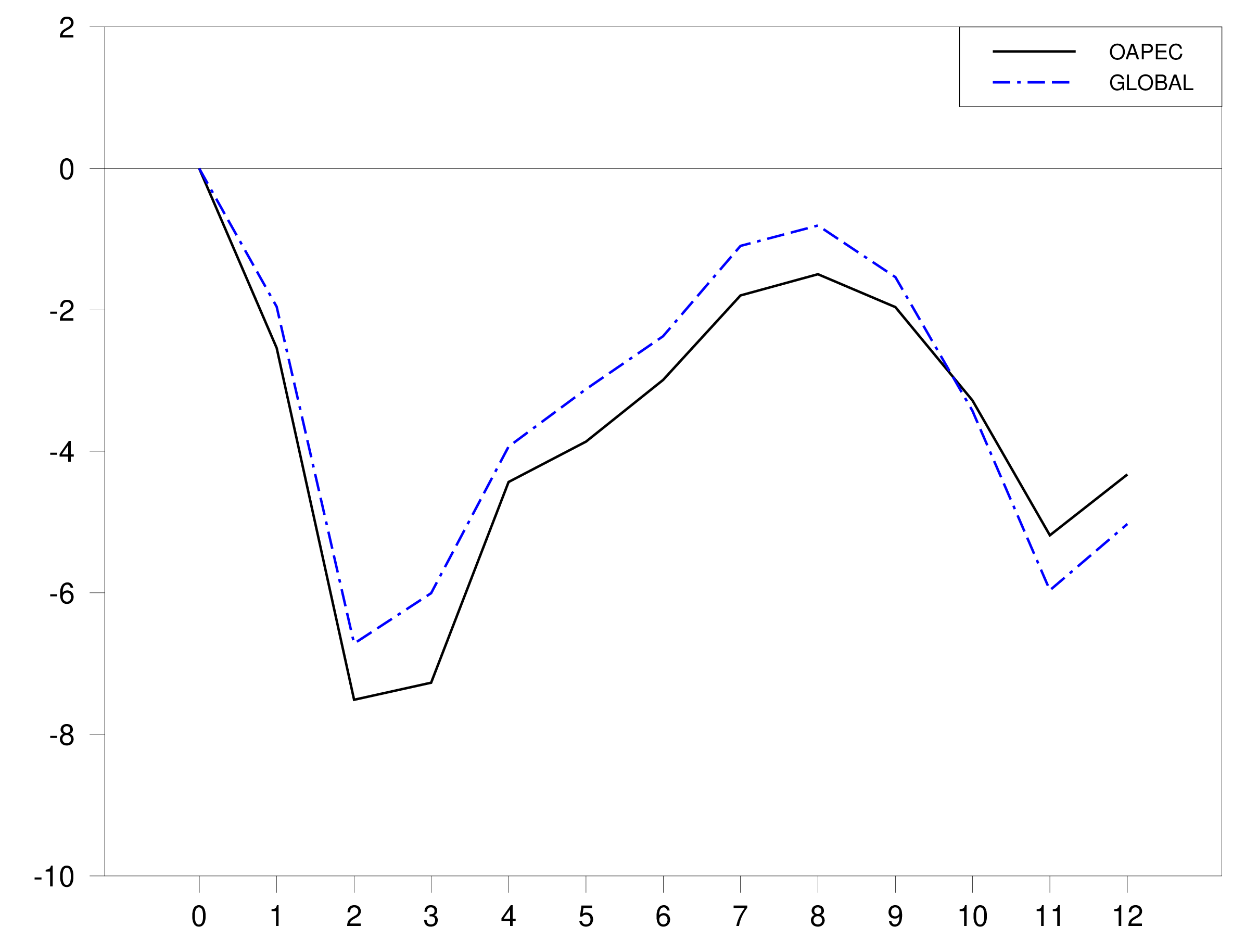

Another way we might try to answer this question is to look for historical precedent. In October 1973, OPEC’s Arab members announced a ban on oil sales to the United States and other countries deemed pro-Israel. The black line in the graph below depicts the reduction in oil production by OPEC Arab members as a percentage of total world production. The largest shortfall amounts to 7% of world production. Production in other countries increased at that time, but not by much. The total decline in global production for all countries is shown in blue.

Oil production after the 1973 Arab-Israeli war. Blue dotted line: change in global monthly crude oil production since September 1973 as a percentage of September 1973 levels. Solid black line: The change in monthly oil production by OPEC Arab members since September 1973 as a percentage of the September 1973 global level. Horizontal axis: Number of months since September 1973. source: Hamilton (2013).

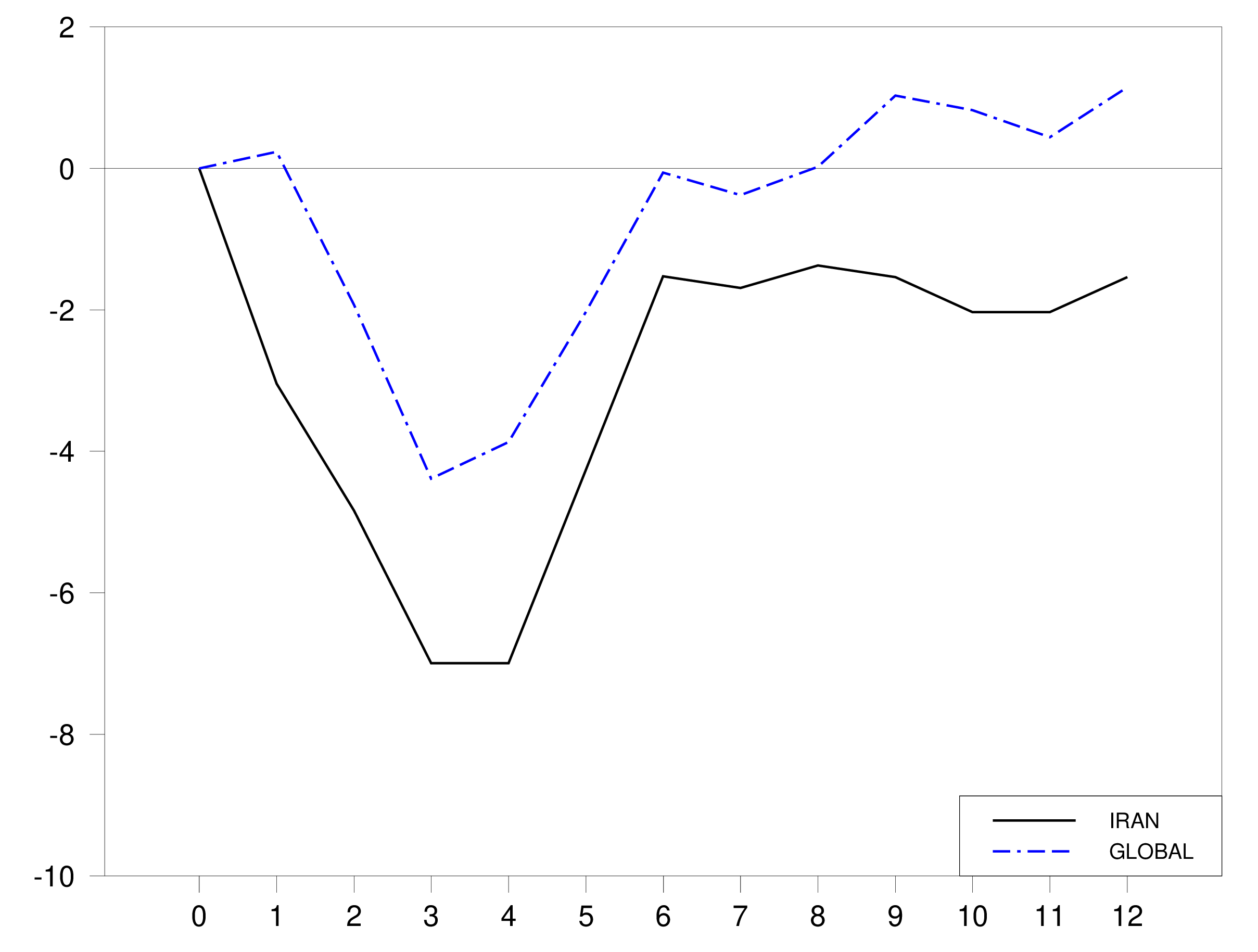

Another example comes from the 1978 Iranian Revolution. It also destroyed about 7% of the world’s oil production. But in this case, production increases in other countries would limit the global shortfall to around 4%.

Oil production after the 1978 Iranian Revolution. Blue dotted line: Change in global crude oil monthly production since October 1978 as a percentage of October 1978 levels. Black solid line: change in monthly oil production in Iran since October 1978 as a percentage of October 1978 global level. Horizontal axis: Number of months since October 1978. source: Hamilton (2013).

The table below summarizes these events and two other historical examples of significant oil supply disruptions. In all of these events, we have seen about a 5% reduction in world supply. A 50% reduction in the amount of Russian oil entering the market would represent a shock as big as any of the four examples. Russia halted production altogether, along with shutting down natural gas, in what would be the largest energy supply disruption in history.

| date | |||||

|---|---|---|---|---|---|

| 11/73 | |||||

| November 78 | |||||

| October 80 | |||||

| Aug 90 |

After each of the aforementioned oil supply disruptions, the U.S. had a recession. If the above quick calculation of the economic value of lost oil is correct, we would conclude that the fact that a recession followed these events must be a coincidence, and that the main cause of the recession will be found elsewhere.

A defining feature of recessions is that factors of production are underutilized. In recessions, we see unemployment soar as people who have been working lose their jobs and can’t find new ones. Busy factories operate at less than full capacity. If the underutilized resource is one of the consequences of oil supply disruption, then the economic cost will be far greater than the simple calculation above assuming that the only thing we lose can be measured by the market value of oil itself.

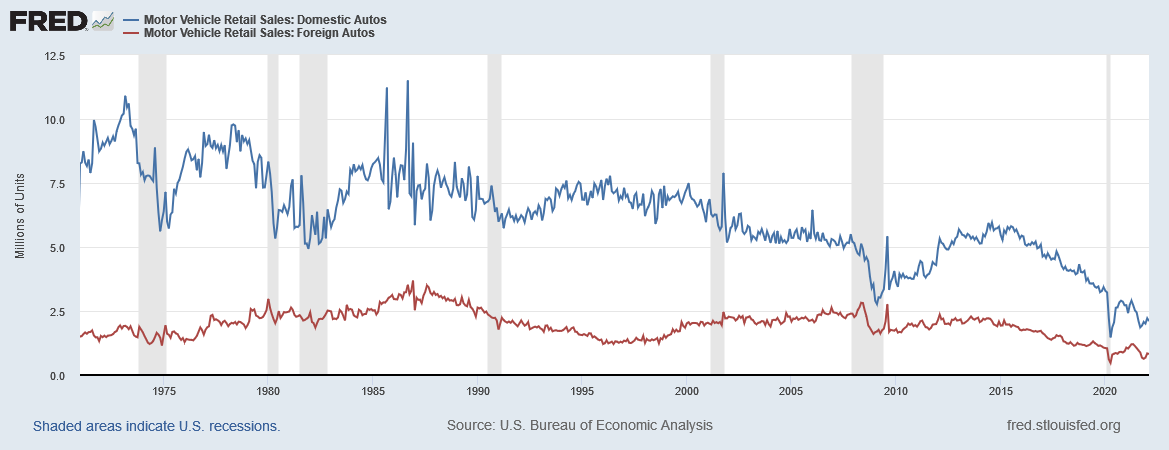

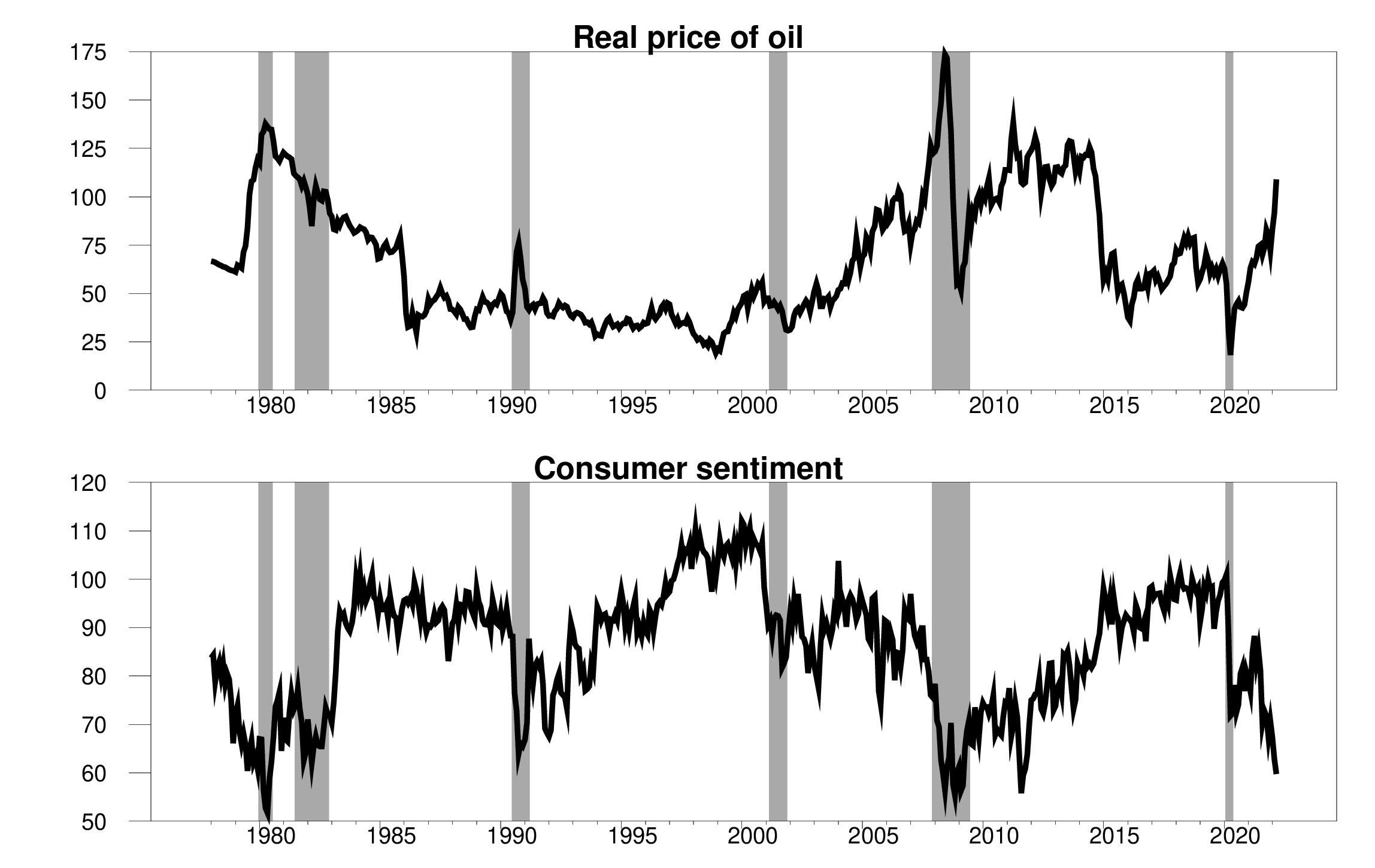

Car production is undoubtedly a part of that. The above-mentioned four phases of automobile sales and production all saw a sharp decline, while other short-term oil prices rose sharply, both car sales and production fell sharply. Auto workers were laid off, and factories were producing far fewer vehicles than before. Perhaps the hit to cars comes from factors other than gas prices. But we usually see car sales start to drop when oil prices start to soar, which is usually a few months before a recession starts. Gasoline prices, for example, rose sharply in 1973, and car sales fell before the embargo and before the recession officially began. The price hikes and falling car sales associated with the Iranian revolution also started long before the recession. Additionally, we often see sales of gas-guzzling cars go down while sales of more fuel-efficient cars go up. It seems hard to argue that gasoline prices have not played a role in these developments.

While gas spending is a relatively small percentage of average consumer spending, it can vary widely depending on the individual circumstances you’re focusing on. Kuhn, Kerig and Zibat (2021) It was found that 10% of US consumers spend no money on gasoline at all, while another 10% spend more than 10% of their budget on gasoline. The median U.S. household spending is 4%. When prices doubled, many of those households tried to keep buying the same number of gallons, which meant they had to spend less elsewhere. We see a strong correlation in the data between gasoline prices and consumer confidence. The dramatic change in gasoline prices seems likely to lead to drastic cuts in spending in other categories. The lower demand for these products has again led to worker unemployment and underutilization of capital in these industries.

The conventional wisdom that a sudden change in spending patterns could lead to a decline in real GDP emphasizes that nominal prices fail to adjust quickly enough to respond to falling demand. If this were the mechanism, we could counter some of the effects of the oil shock with monetary and fiscal stimulus to try to keep aggregate demand high.

My point is that changes in demand lead to underutilization of resources because technological barriers prevent rapid changes in production. Factories can’t immediately switch from making big cars that people no longer want to making the small cars they want now. Fiscal or monetary stimulus will not solve this problem.I’m here recent papers.

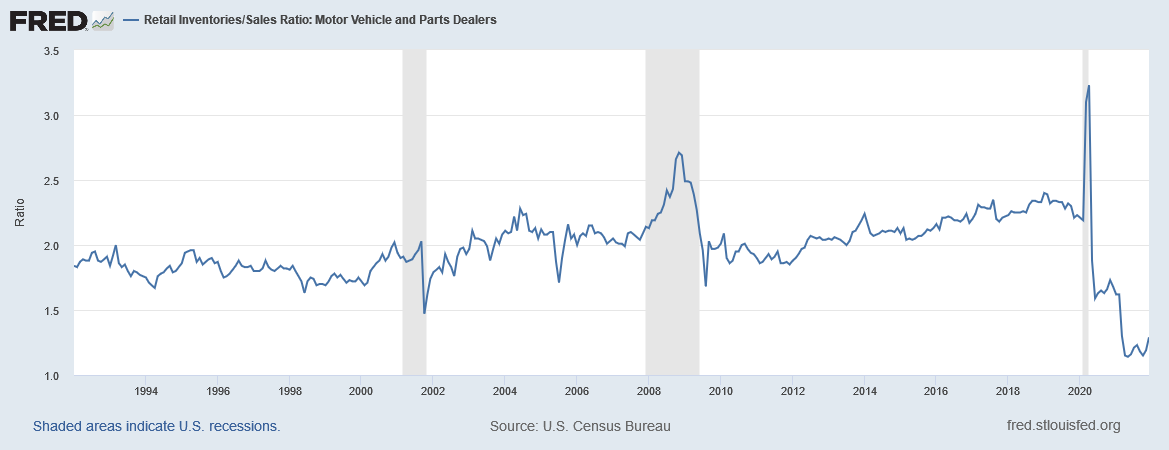

How is the situation now? The chart above shows that consumer sentiment is declining during the current event, as it has been during previous oil price spikes. However, the situation in the auto industry today is very different from what it was before. The downturn in car production is not because of lack of demand, but because of supply issues, for example, Problems getting computer chips. By the way, this is another example of the broader argument I made. Just looking at the dollar value of chips is no way to judge the scale of the damage caused by chip shortages. If modern cars couldn’t be built without them, the lost resources would be far beyond the dollar value of the chips themselves. But the fact that supply, not demand, has been a key limiting factor, means that a drop in car demand won’t have the same overall impact as it would in a normal market environment. I’ve been expecting a big jump in GDP as auto dealers replenish depleted inventories. That’s not going to happen to the same extent now, which lowers my growth forecast for 2022. But that won’t keep car sales below 2021 levels.

Based on what has happened so far, I don’t think the US is heading for a recession right now. But if we do see a big drop in Russian oil and gas shipments, I’m much more pessimistic than some other economists. Given the localized market for natural gas, I think Europe will face some real challenges if supplies come to a sudden stop.

Let me end with a final comment. I am here to discuss only the economic consequences of the tragic events currently taking place in Europe. But the situation in Ukraine is more dire and scary than any concern I’ve been talking about. My personal view is that we should push for tougher sanctions to take away the revenue that Putin uses to fund continued suffering and bloodshed.

We shouldn’t have any illusions about the cost of doing this for everyone. But if Russia succeeds, it will cost us all a lot more.

{kind=link}

{kind=link}