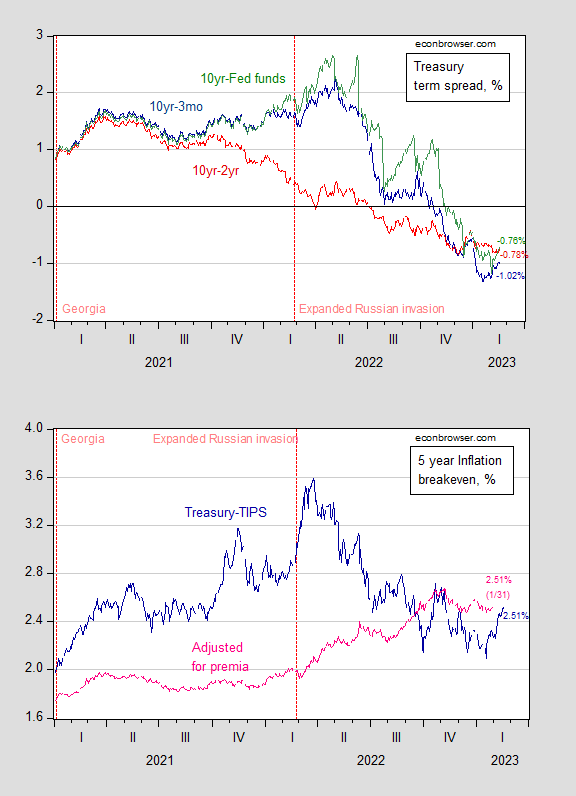

Quite frankly, term spreads have turned inverted and inflation expectations adjusted for premiums have risen. The VIX has been rising since February 2022, with geopolitical risk rising in the period following the invasion. Growth that had been accelerating then decelerated, according to weekly indicators. In other words, “Thank you, Putin”.

Figure 1: Top panel: 10Y-3M Treasury Spread (blue), 10Y-2Y Spread (red), 10Y-Fed Funds Spread (green), all expressed as percentages. Bottom panel: 5-Year Treasury – TIPS Spread (dark blue) and 5-Year Expected Inflation (pink), both in %.Source: Treasury via FRED, and kilowatt After D’amico, Kim and Wei (DKW) visit 2/18,

Note that while TIPS spreads widened immediately after the invasion and then fell, inflation expectations, as measured after accounting for risk and term premiums, have continued to rise since the invasion.

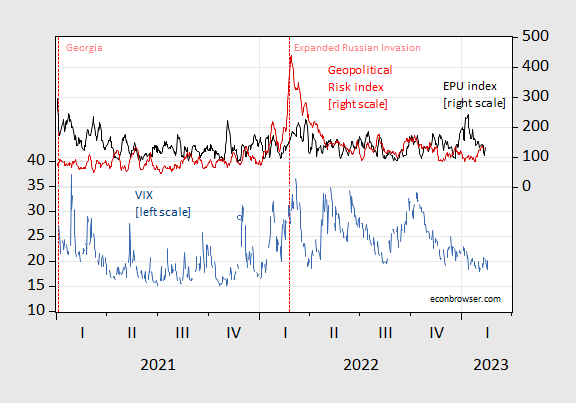

figure 2: VIX (blue, left scale) and Economic Policy Uncertainty Index, centered on 7-day moving average (black, right scale), Geopolitical Risk Index, centered on 7-day moving average (red, right scale) . Source: CBOE via FRED, policyuncertainty.com via FRED, Caldara/Iakovielloand the authors’ calculations.

The VIX has been rising since the invasion — and so has the geopolitical risk index.

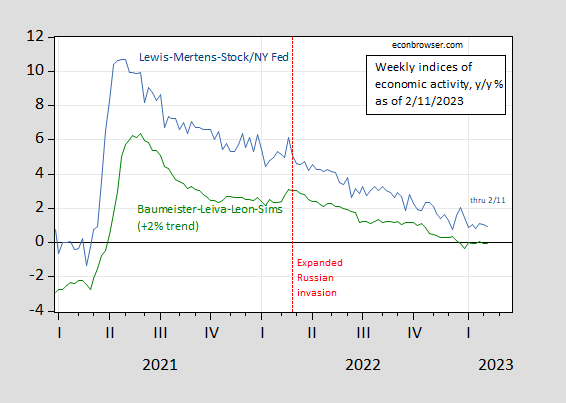

Given these observations, it is not surprising that high-frequency indicators of economic activity resumed declining with the invasion.

image 3: Lewis-Mertens-Stock weekly economic index (blue), Baumeister-Leiva-Leon-Sims US weekly economic conditions index plus 2% trend (green).Source: New York Fed via fred, WECIand the authors’ calculations.

{kind=link}

{kind=link}