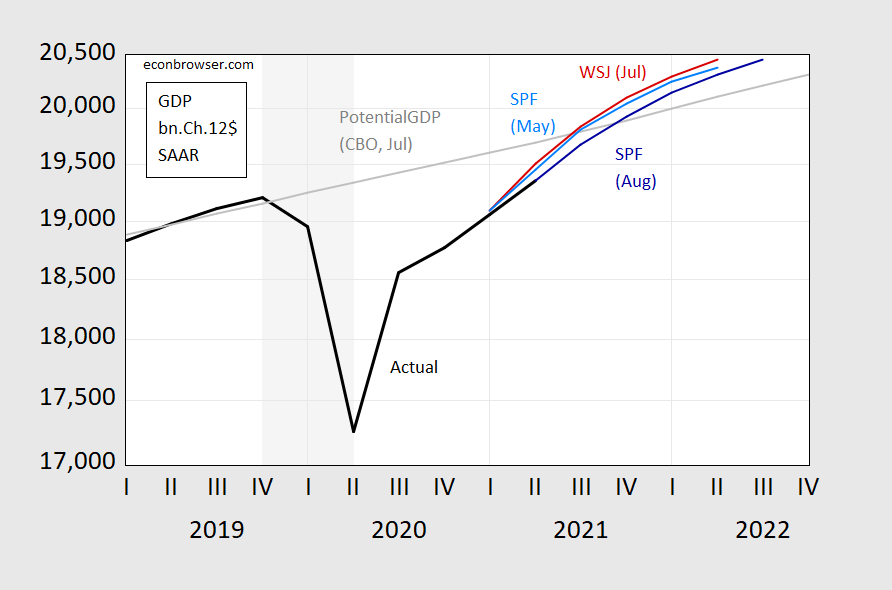

Growth prospects have slowed, while CPI levels look higher, according to Survey of professional forecasters in August.

figure 1: Reported GDP (black bold), Wall Street Journal’s July survey of forecast GDP (red), May SPF forecast GDP (light blue), August SPF forecast GDP (dark blue), all in billions Ch .2012$, SAAR. Source: BEA, early release in 2021Q2, WSJ July survey, Survey of professional forecasters by the Federal Reserve Bank of Philadelphia (Various), NBER and author’s calculations.

From May to August, the decline in forecast growth is quite large. Although we do not have an SPF forecast for July, based on my experience, the SPF and Wall Street Journal growth forecasts are similar. This in turn means that the growth prospects for the past month have dimmed.Retail sales

Interestingly, compared with the CBO’s forecast in July, the current SPF consensus is closer to the forecast locked in by the government in February. This means-if CBO’s estimate of potential GDP is accurate.

As expected, CPI inflation is temporarily higher, so the level is expected to be higher.

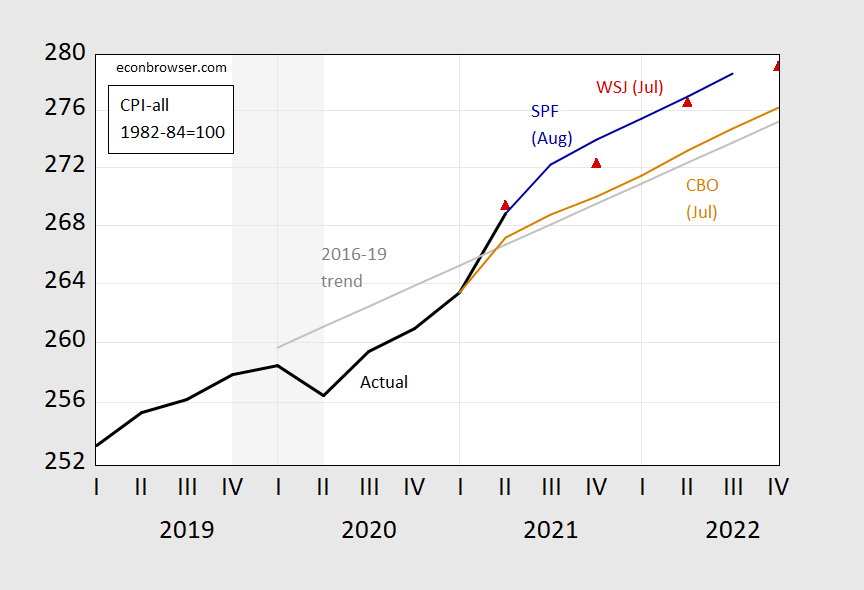

figure 2: CPI (black bold), CBO forecasted CPI (brown), WSJ July survey forecast (red triangle), SPF forecast (blue), 2016-19 random trend (grey), all 1982-84=100. The decline date defined by NBER is shaded in gray. source: The Wall Street Journal’s July investigation, Survey of professional forecasters by the Federal Reserve Bank of Philadelphia, NBER and the author’s calculation.

The fact that the path of the price forecast is roughly parallel to the CBO’s July forecast indicates that the increase in inflation is considered temporary-the current quarterly inflation forecast has been revised up from an annualized 2.6% to 5.2%.

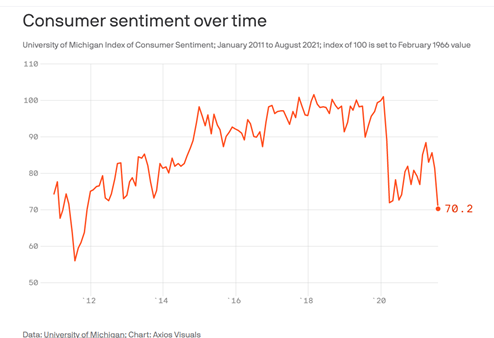

According to the University of Michigan survey, the decline in growth expectations is consistent with the decline in consumer confidence.

source: Luo, Aksios, August 16, 2021.

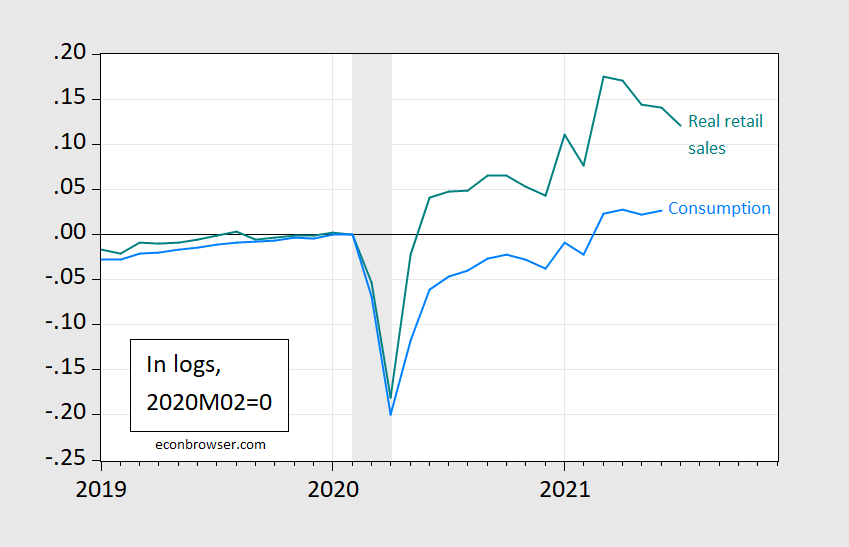

Today’s retail sales data is lower than expected, indicating that economic activity has actually cooled down.

image 3: The actual retail sales of 84 US dollars in 1982 (green) and 2012 (light blue), excluding food services, are both in the logarithm of 2020M02=0. The NBER decline date is shaded in gray. Source: Census, BLS, BEA, NBER, and author’s calculations.

The data for the first few months has been revised upwards, so IHS MarkIt nowcast, for example, has raised its estimate of the growth in the second quarter. GS has not yet released (at least I haven’t seen it) an updated nowcast that reflects retail sales for the third quarter. For me, it’s worth noting that the actual (reduced by CPI) food service sales (calculated by subtracting retail sales from retail sales and food services) for the past two months have been basically flat.

{kind=link}

{kind=link}