William Luther of AIER asked “Is inflation just catching up?“:

… The observed inflation is only what is needed to catch up, which is simply not true. Today’s price levels are higher than expected in the absence of a pandemic, and higher than the Fed’s hint that it will give it a 2% inflation target. The price level has exceeded expectations. The question now is whether it will continue to grow so rapidly, stay high, or fade away.

In other words, his answer to the question raised in the title is “no”. Whether it will have a harmful effect depends on how sustained inflation is relative to expectations.

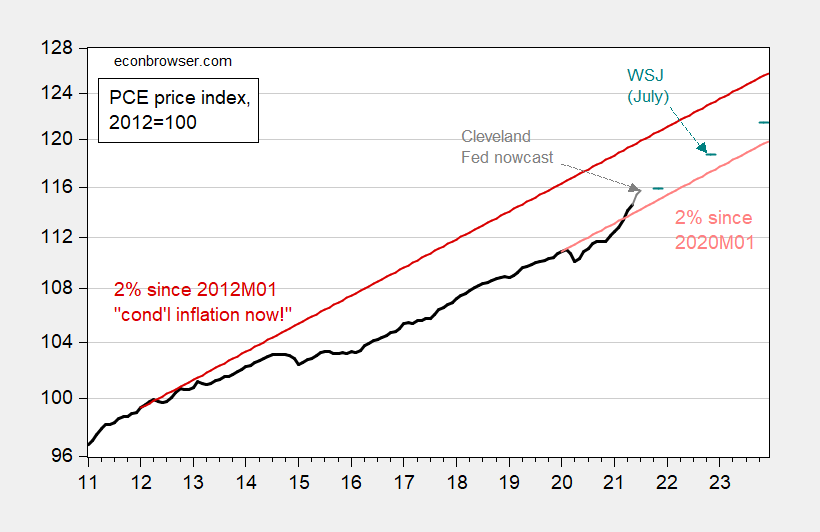

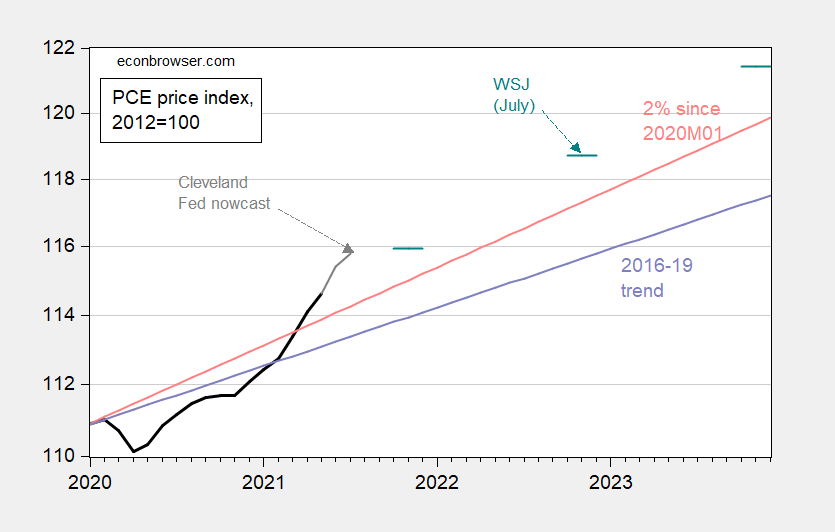

I have drawn the PCE price index, the Cleveland Federal Reserve’s real-time forecast data as of July 26, and the comparison of the WSJ July forecast with the 2015M01-2021M01 trend cited by Dr. Luther and the 2% trend.

figure 1: Personal Consumption Expenditure (PCE) Price Deflator (black), Cleveland Federal Reserve Nowcast (grey line), Wall Street Journal survey mean (cyan line), 2015M01-20M01 trend (light blue), 2020M01 2% trend (pink) ), all 2012=100, on a logarithmic scale. Source: BEA, Cleveland Federal Reserve (visited 7/26), WSJ July survey and author’s calculations.

Using Dr. Luther’s trend, if the Cleveland Fed’s nowcasting is accepted, then the PCE price index appears to have exceeded the standard as of today. As the inflation rate continues to exceed 2% (as shown by the Wall Street Journal’s July economist survey), the price level continues to deviate from the trend.

As of July, the price level will be 1.3% above the trend; by November 2023, it will be 1.5% (in logarithms). Compared to the facts in April and May 2020, it is useful that the index is 1.2% below the trend.

already In January 2012, Jeffry Frieden and I are now calling for conditional inflation! Stay at 4%-6% in a few years. The call (if 2%) means the following:

figure 2: Personal Consumption Expenditure (PCE) Price Deflator (black), Cleveland Federal Reserve Nowcast (grey line), Wall Street Journal survey mean (cyan line), 2% trend for 2020M01 (pink), 2% trend for 2012M01 (red) , All 2012=100, on a logarithmic scale. Source: Bank of East Asia, Cleveland Federal Reserve (accessed on July 26), Wall Street Journal July survey and author’s calculations.

From this perspective, we still have a lot to do. As of July, the price level will be 3.4% below the trend; by November 2023, it will be 3.3%.

Which is the correct comparison? Luther was right to interpret the shock as a pandemic in early 2020. In addition, the flexible average inflation target (FAIT) dates back to January 2020 to take effect, so this is another reason for comparison. On the other hand, if we have been thinking about trying to correct too slow price inflation in the past decade after the Great Recession, then the calculations in Figure 2 are more appropriate in a sense.

{kind=link}

{kind=link}