Calculated risk (h/t pgl) Note the fall in futures timber prices. Joseph Some people think that this will not necessarily be reflected in the actual price paid by consumers for a period of time. I don’t have a retail price, but I removed the BLS measurement standard from consumers by one step, which is the PPI of wood.

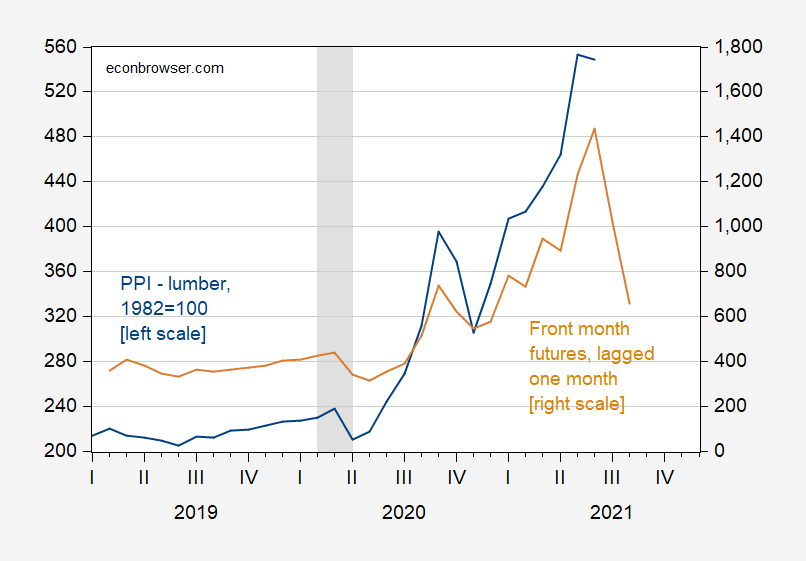

figure 1: The PPI of lumber and cork (blue, left scale) and the PPI of near-month futures lag one month (brown, right scale). The NBER decline date is shaded in gray. Source: BLS through FRED, Macro Trend Network, NBER and the author’s calculation.

The correlation between the two variables seems obvious, but to illustrate the tightness of the fit, here is a scatter plot.

figure 2: Compared with the near-month softwood futures price, the softwood PPI is one month behind, and both are calculated by logs. Futures data is the monthly average of daily data.

In my June post, I pointed out that a 1% futures basis (approximately logarithmic futures minus logarithmic current spot) does not necessarily mean a 1% decline in timber prices, which would be implied in a risk-neutral efficient market environment. Mehrotla and Carter (2017) It is found that between 1995 and 2013, within a two-month range, a basis of 1 percentage point means a decrease of 0.55 percentage points. This means that the PPI fell by 7% in June. Facts have proved that the actual change was 7.3%.

Here I adopt another method. In view of the evidence that both PPI and futures are non-stationary during this sample period, I use the following equation in the logarithmic first difference to make predictions:

Δppi_lumberTon = 0.01 + Δ0.67Timber_Futuret-1

Adjustment-R2 = 0.64, SER = 0.054, DW = 2.27, Nobs = 28. bold Indicates the significance of using the HAC robust standard error at the 1% level.

This regression produces the following predictions:

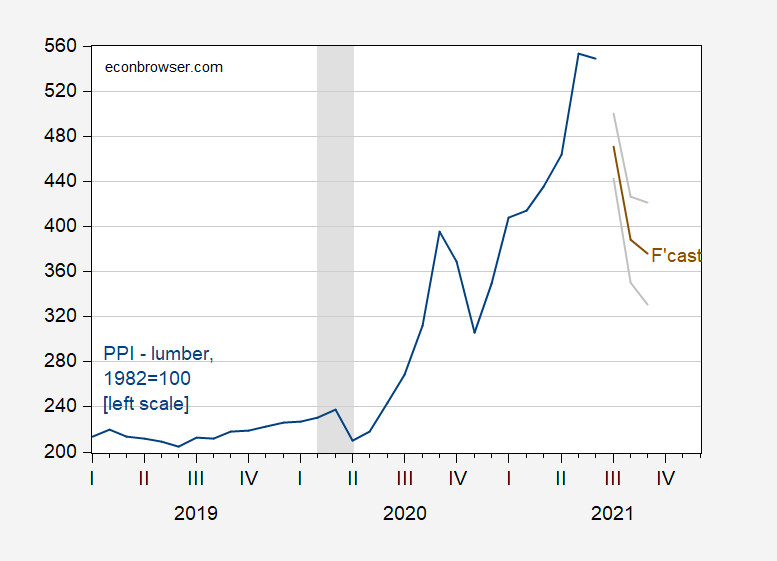

image 3: PPI (blue, left scale) and forecast (see text) (dark brown) for wood and cork, and +/- 1 standard error (grey). The NBER decline date is shaded in gray. Source: BLS calculated by FRED, NBER and the author.

The model predicts 15.3%, 19.3% and 3.2% in July, August and September respectively (all calculated by logarithmic difference). This forecast brings the September PPI to the average level of December 2020/January 2021.

{kind=link}

{kind=link}