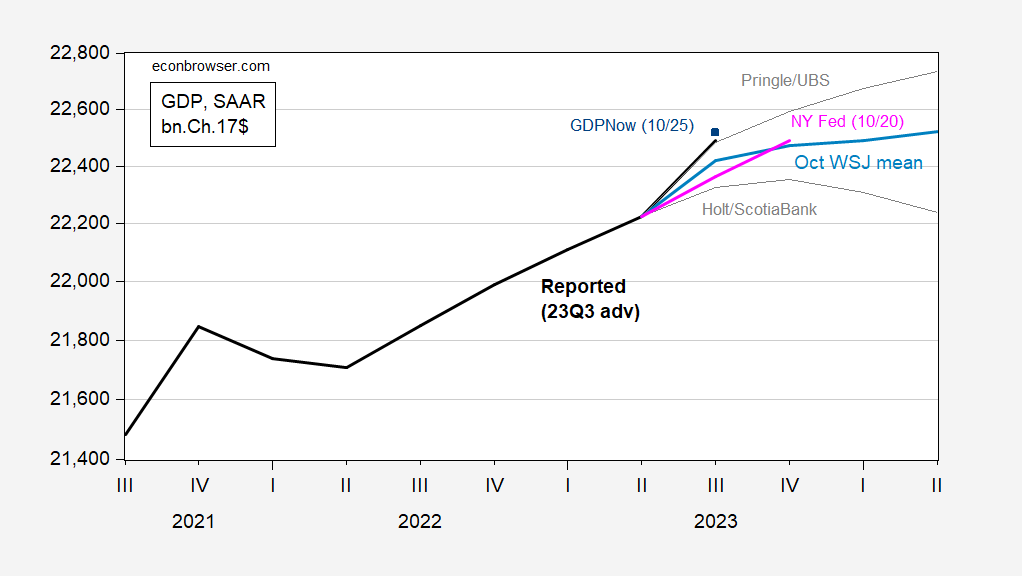

GDP surged to 4.9%, compared with Bloomberg’s forecast of 4.3% and the Atlanta Fed’s GDPNow of 5.4% (about a percentage point lower than 2017 GDP) GDPNow two months ago seemed too optimistic (8/24)). Jim’s post yesterday Implications for recession calls and macrostability (inflation falling to target) are discussed. The chart below shows advance estimates of GDP relative to instant forecasts and forecasts.

figure 1: Q3 2023 GDP estimates from report (black), Wall Street Journal October survey average (blue), 20% adjustment range (grey line), GDPNow (blue square), New York Fed Instant forecast (pink line), all in billions. 2017 Quarterly Annual Growth Rate $SAAR. Source: BEA, Wall Street Journal, Federal Reserve Bank of Atlanta, Federal Reserve Bank of New York, and author’s calculations.

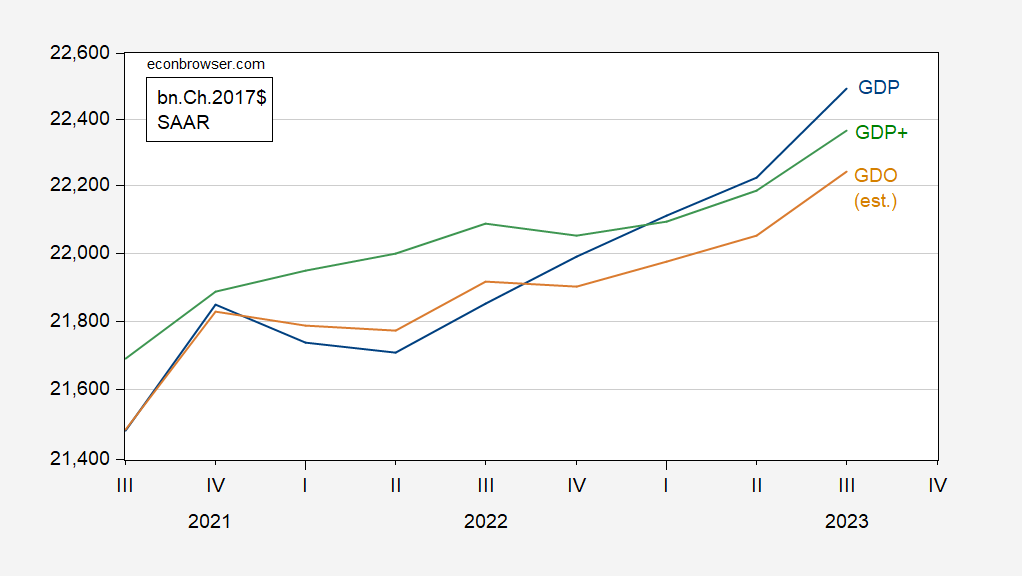

GDP is a measure of output in terms of expenditures.According to records Economic Commission for Europe (2015) and Nalervik and Braun (BPEA, 2011)GDO (the arithmetic mean of GDP and GDI) is a more accurate measure of final GDP, and hGDP regresses GDO better than other methods.

figure 2: GDP (blue), GDO (tan) and GDP+ (green), all in 2017 billion USD seasonally adjusted (SAAR) units. GDO assumes a $100 billion decline in third-quarter corporate revenue (seasonally adjusted earnings). GDP+ assumes that GDP+ in the fourth quarter of 2019 is equal to GDP. Source: BEA 2023Q3 advance estimates, Philadelphia Fed (Viewed October 26, 2023) and the author’s calculations.

review as In July 2001, preliminary readings of second-quarter GDP growth were positive (at that time, the NBER set the peak of the business cycle as the first quarter of 2001)., it is important to remember that GDP can undergo significant revisions (which is why the NBER BCDC does rely heavily on this indicator). The average absolute revision (from pre-qualification to final) is 1.2 ppts (SAAR) and the standard deviation of revisions (from pre-qualification to final) is 1 ppt. (The average revision is 0 percentage points, so advance estimates of growth are, on average, unbiased.) A negative reading for third-quarter GDP in the final year seems unlikely, given a reading of 4.9 percentage points and a MAR of 1.2 percentage points. .

this Philadelphia Fed GDP+Contains revised information showing that third-quarter GDP was 1.5 percentage points below the GDP indicator (SAAR). Nonetheless, given that the previous growth reading was above GDP, GDP+ rescaled to GDP+ = GDP for the fourth quarter of 2019 showed output was 0.6% lower than the official reading.

Incidentally, the current GDP+ years show no negative GDP growth in the first half of 2022, so even if one wanted to use GDP-like indicators to define a recession, a recession in that period seems taboo.

{kind=link}

{kind=link}