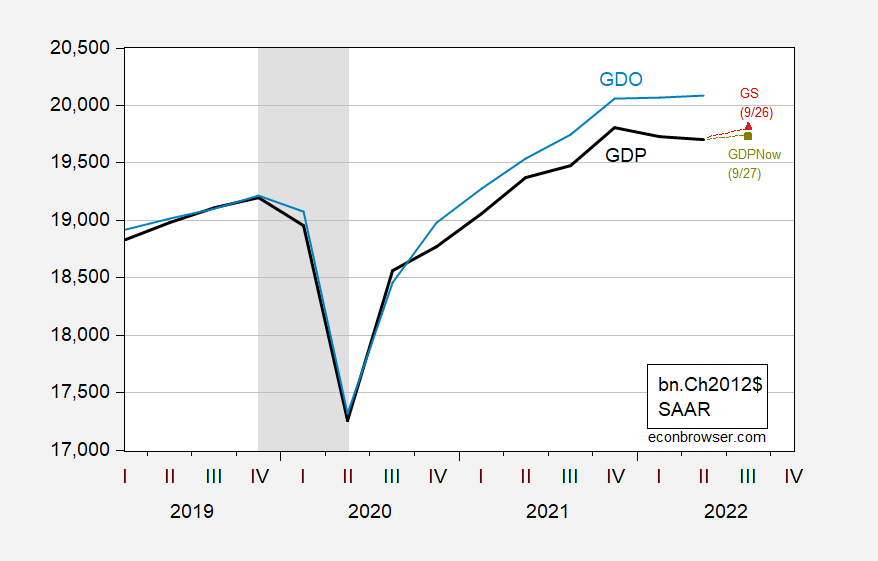

The Atlanta Fed (0.3% SAAR) forecast sluggish third-quarter growth, while Goldman Sachs (1.2%) was slightly faster. It is important to remember that the impact on the implied level of GDP may be dwarfed by the annual benchmark revision. And for the first time, the annual benchmark revision will come on September 29 instead of the end of July.

figure 1: GDP (black), GDO (blue), GDPNow nowcast (yellow-green square), Goldman Sachs nowcast (red triangle), all in billions Ch.2012$ SAAR. The NBER uses shades of grey to define the peak and trough dates of the recession. Source: BEA Q2 second release, Atlanta Fed (9/27), Goldman Sachs (9/26), NBER and author’s calculations.

We don’t know what effect the revision will have on GDP’s trajectory, but we do know that, overall, GDO is a better predictor of what revised GDP will ultimately look like than reported GDP. The first annual benchmark revisions sometimes lead to noticeable changes. For example, the 2018 annual benchmark implied first-quarter GDP was 0.4 percentage points higher than initially reported.

This article discusses revisions in detail East Asian Articles.

{kind=link}

{kind=link}