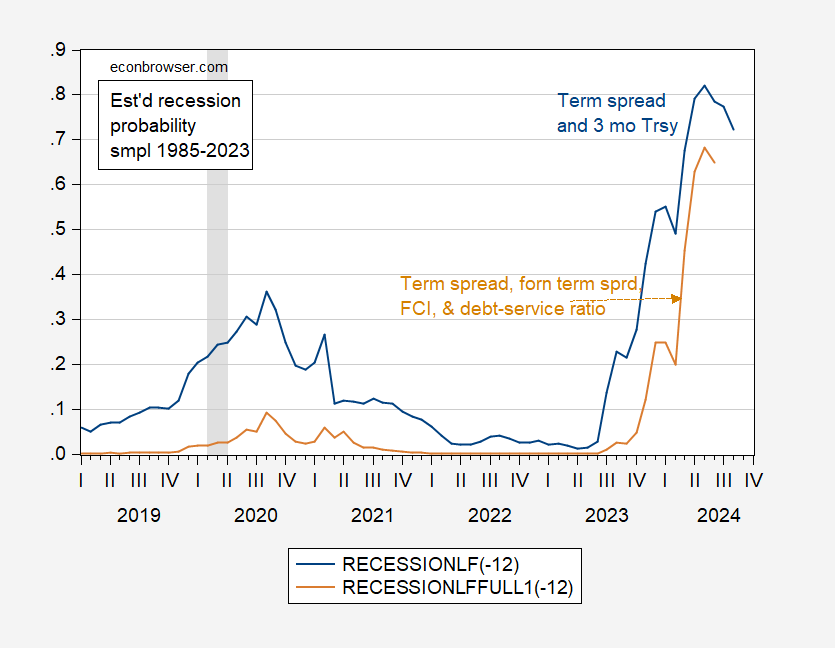

in the previous one postal, I propose recession forecasts based on a probabilistic model using term spreads plus short rates, term spreads plus short rates, foreign term spreads, and debt service ratios. The latter only lasts until March 2024, as the Bank for International Settlements only publishes debt service ratio data as of March. I extrapolated this ratio to June to get the forecast below.

figure 1: Recession probability based on the 10-year to 3-month maturity spread plus the 3-month rate (blue) as well as interest rate spreads, foreign spreads, the country’s financial conditions index and the debt service ratio (tan). The model estimates 1985 to 2023 (assuming no recession in August 2023). Source: Treasury via FRED, Federal Reserve Bank of DallasDGEIFederal Reserve Bank of Chicago through FRED, Bank for International Settlementsand the author’s calculations.

The complete model has a pseudo-R2 is 0.52, while the term spread model is 0.28. The full model has no false negatives or false negatives for the period 1989 to 2022.

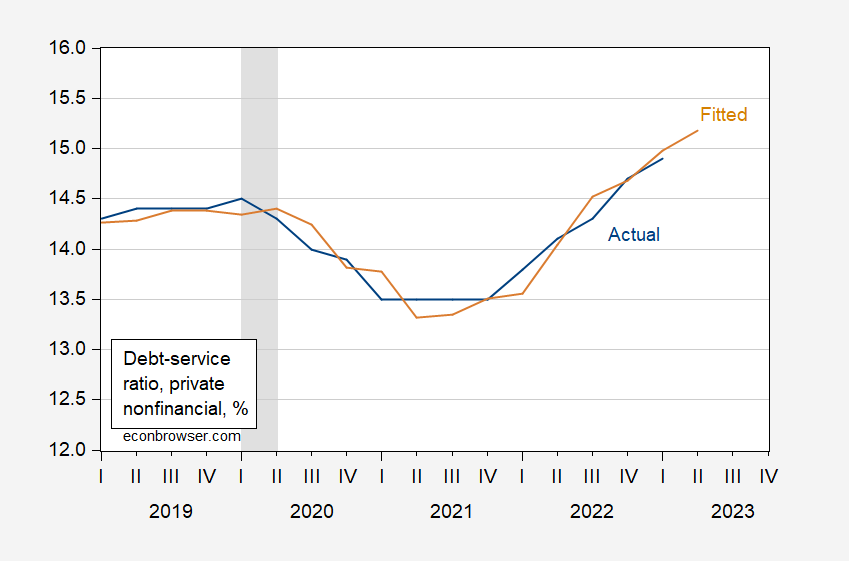

To extrapolate the debt service ratio into the second quarter of 2023, I forecast the debt service ratio using corporate AAA rates, three-month Treasury yields, and two lags of the debt service ratio (all using first differences). adjective-R2 is 0.69. The fitting situation (2019-23) is shown in Figure 2.

figure 2: Debt service ratio (blue) and fitted values (tan), both expressed as percentages. First-difference model estimated for 1985-2023. source: Bank for International Settlementsand the author’s calculations.

The debt service ratio (estimated) rose from 14.9 to 15.2, pushing up the probability of a recession from 45% to 65% (term spread model probability from 68% to 79%).

{kind=link}

{kind=link}