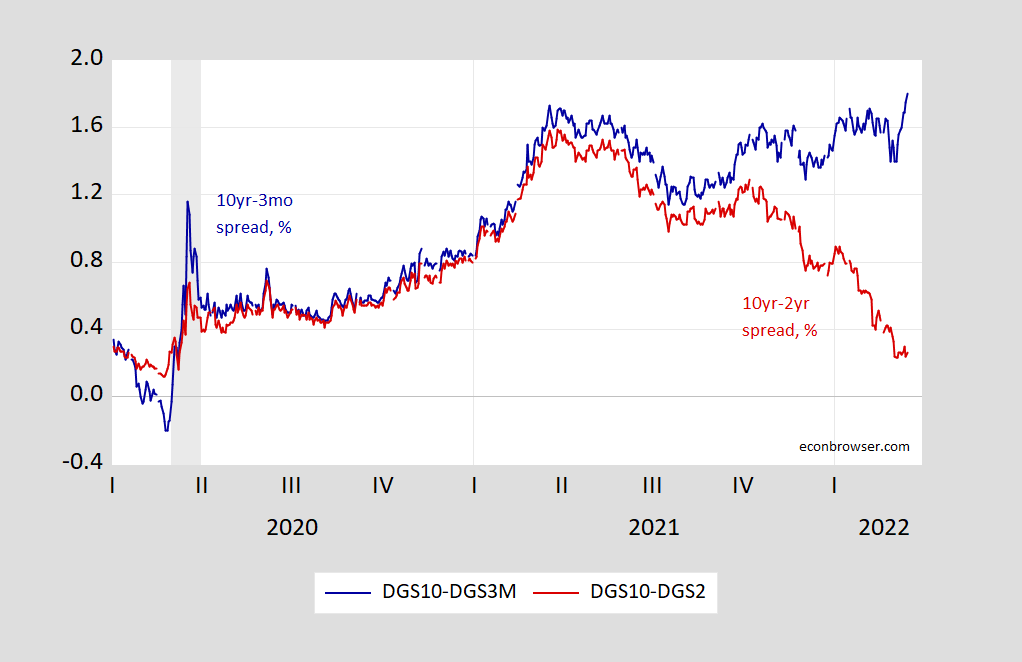

The economy is still likely to grow based on a spread of at least 10 years to 3 months. Less clear indicators of 10 to 2 years. Expected inflation has stopped rising, thus also implying future rates in the next 2-3 months; in fact, they have all fallen in recent days. (For what analysis, not the market, considers inflation, see Jim’s Monday Post; for recession, see Jim Wednesday’s post.

figure 1: The 10-month-three-month Treasury spread (blue) and the 10-year-two-year Treasury spread (red), expressed as a percentage. Recession dates as defined by NBER are shaded in gray. Source: Treasury via FRED, NBER and author’s calculations.

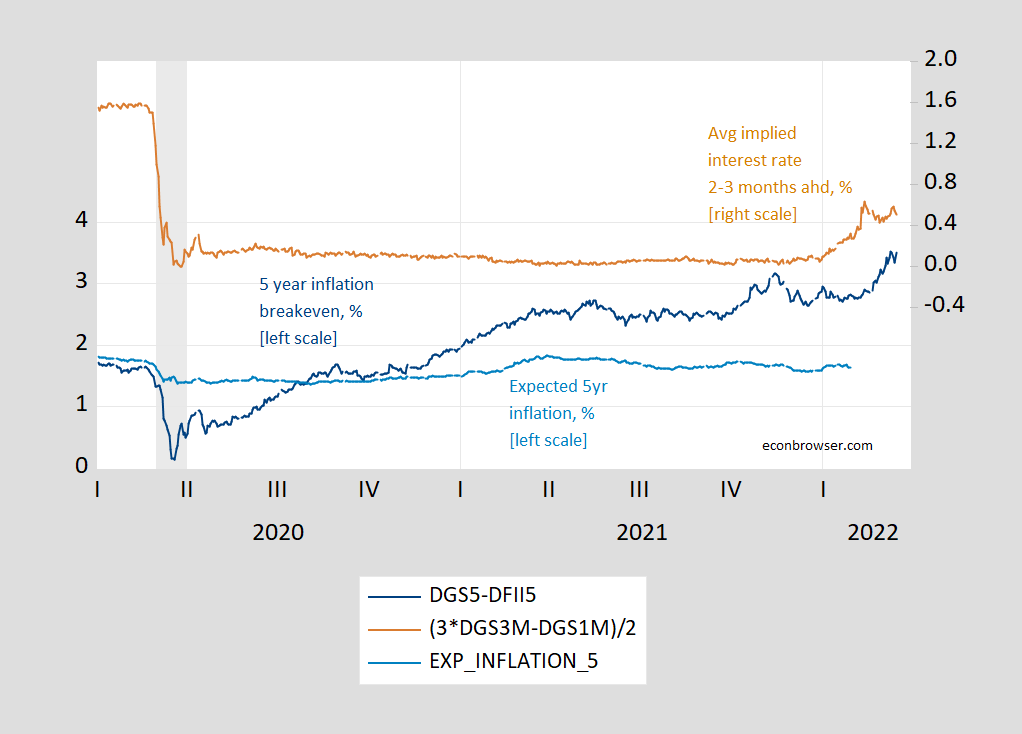

What does expected inflation look like and how do interest rates respond?

figure 2: Five-year inflation breakeven calculated as five-year Treasury yield minus five-year TIPS yield (dark blue, left scale), five-year breakeven adjusted for inflation risk premium and liquidity premium per DKW (light blue, left scale) , 2-3 month forward rate (brown, right scale), all in %. Recession dates as defined by NBER are shaded in gray. Source: FRB via FRED, Treasury, Kim, Walsh & Wei (2019) Following NBER’s D’amico, Kim and Wei (DKW).

It’s hard to see how the 5-year inflation breakeven has evolved, but it has stopped rising as oil prices retreated.

image 3: Five-year inflation breakeven is calculated as five-year Treasury yield minus five-year TIPS yield, % (blue, left scale) and oil price, WTI, $/bbl (black, right log scale). Source: Treasury and EIA, via FRED.

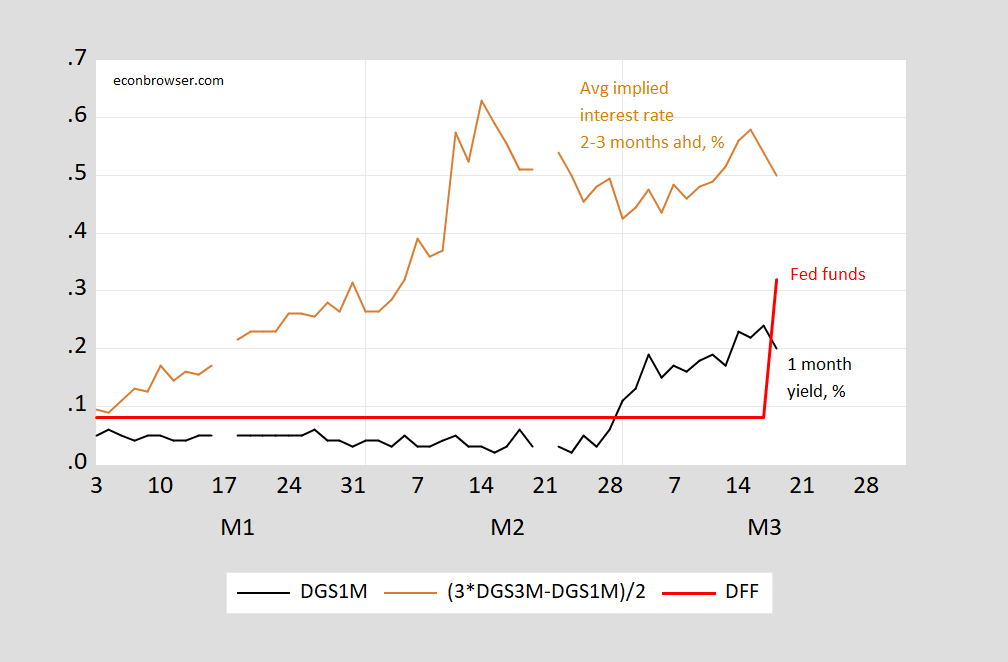

Interestingly, 2-3 month forward rates fell as the fed funds rate increased (although this may have been due to lower oil prices).

Figure 4: Fed funds rate (red), 1-month Treasury yield (black), 2-3 month forward rate (brown), all in %. Source: FRB via FRED, Treasury, Kim, Walsh & Wei (2019) Following D’amico, Kim and Wei (DKW).

Jim presents his overview ‘Sanctions, energy prices and the world economy’ in video.

{kind=link}

{kind=link}