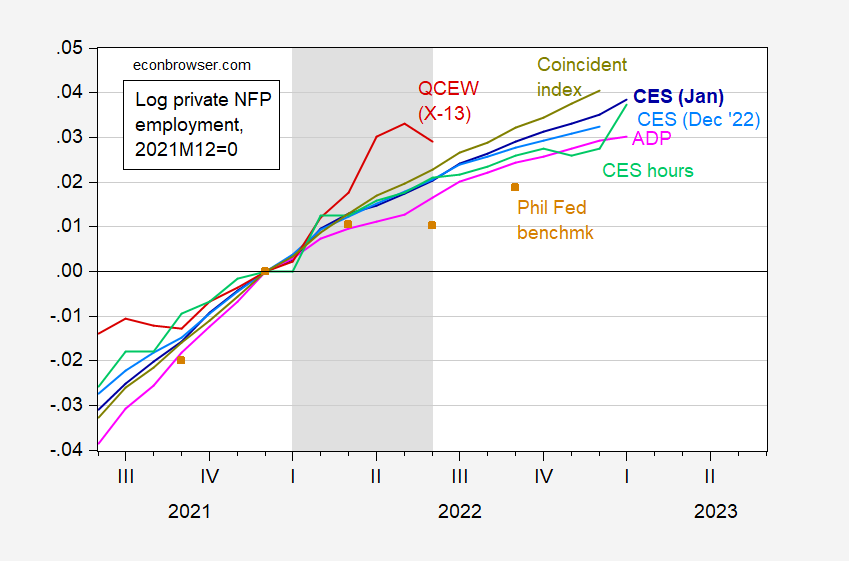

After sorting out a bunch of labor market data, we have the following graph of private non-agricultural labor force, which seems to be related to Last made the argument for a recession in the first half of 2022 a month ago.

figure 1: From the January 2023 CES private nonfarm payrolls inclusion benchmark revision (blue), from the December 2022 CES (sky blue), ADP (pink), CES weekly totals for production and non-supervisory workers Hours worked (light green), QCEW privately covered workers, using log-transformed Census X-13 (red), Philadelphia Fed preliminary benchmark minus reported government employment (tan squares), Philadelphia Fed coincident index (yellow-green) Seasonally adjusted, all seasonally adjusted, log 2022M12=0. A hypothetical recession is shaded in light gray. Sources: BLS (various) via FRED, BLS QCEW, Philadelphia Fed via FRED, and authors’ calculations.

Note: Data was baseline revised for January 2023 CES private NFP March 2023 QCEW data and a new seasonality factor. The QCEW is a nearly complete census reported through June 2022 (but subject to revision), but must be seasonally adjusted to make it comparable to other series.The total weekly hour variable is no Estimates from other independent sources based on CES survey data – in principle it would equal hours employed times average weekly hours worked. The ADP series is based on completely different data than the BLS series. The Philadelphia Fed has a benchmarking program that accesses some, but not all, of the BLS data in order to make more timely estimates. Finally, the Philadelphia Fed Coincidence Index uses the Stock-Watson dynamic factor approach primarily applied to labor market data (including wage and salary expenditures) to infer levels of economic activity.

{kind=link}

{kind=link}