Does it matter if spreads reverse because short-term yields fall or long-term yields rise? mackenzie and mccormick (Bloomberg) says yes. As long-term yields rise…

If, at first glance, the shift in the yield curve is a decidedly positive sign – suggesting that the economy is now less at risk of a recession than before – then that may not be the case. Granted, this suggests traders don’t expect the Fed to shift into firefighting mode anytime soon. Even so, it will almost certainly depress the economy further as it affects mortgages, credit cards and business loans. This would further tighten financial conditions, which could be a welcome development for the Fed. But the risk is that it slams on the brakes so hard that the economy comes to a complete standstill.

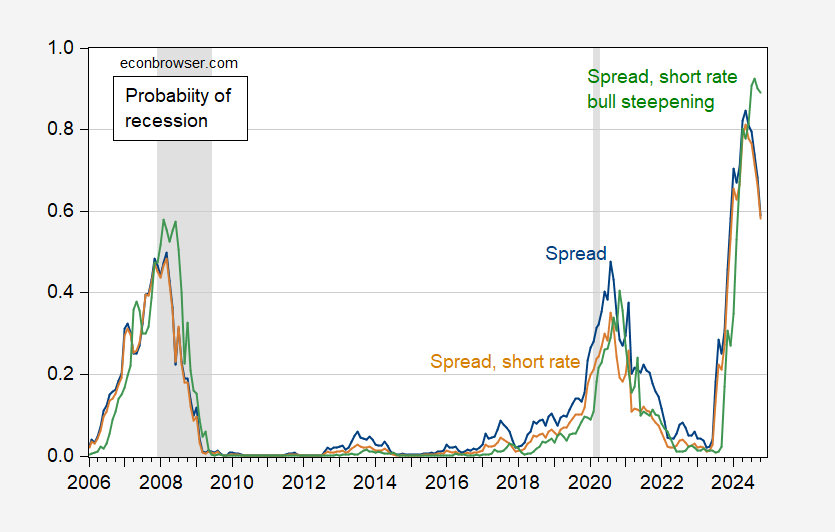

Can a Bull Market Steep Prevent a Recession? Figure 1 covers “large robustness”, which favors this assumption to some extent, at least intuitively. H

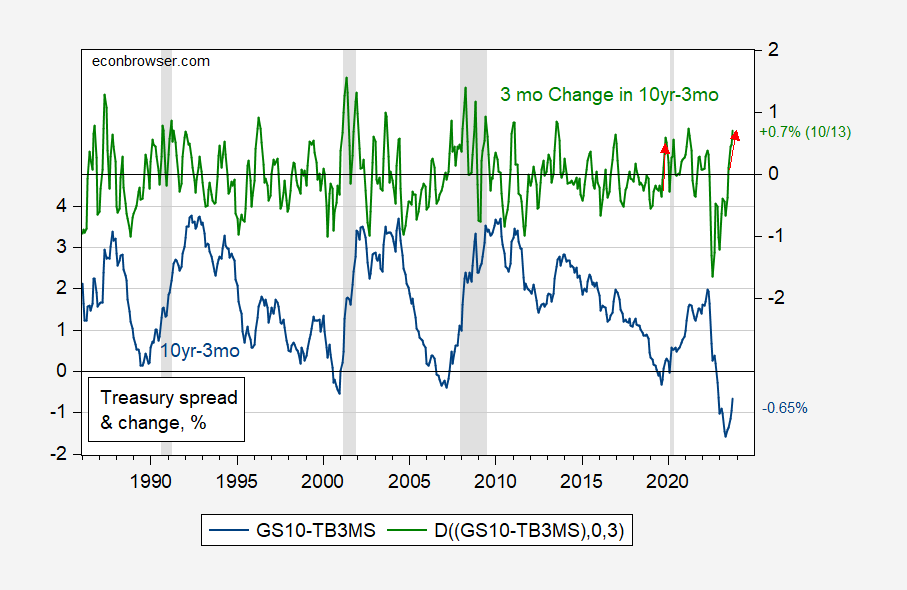

figure 1: The 10-year to 3-month Treasury spread, % (blue, left axis), and the 3-month change in the 10-year to 3-month Treasury spread, ppt (green, right axis). The observation data for October is as of October 13. NBER-defined recession peak-to-trough dates appear gray. The red arrow indicates that the 3-month change was positive during the period when the reversal occurred. Source: Treasury Department through FRED, NBER, and author’s calculations.

The evidence supporting the bear market steepening hypothesis is stronger when the proposition is formally evaluated. I estimate probabilistic models for (i) spreads only, (ii) spreads and short-term rates, and (iii) spreads, short-term rates, and changes in 3-month spreads. The 3-month spread change is statistically significant and increases the pseudo-R2.

(ii)Pr(economic recession=1)t+12 = 0.813 – 76.11spreadt + 9.80Itshort

pseudo-R2 = 0.28, Nobs = 241, bold Indicates significance at 5% MSL.

(3)Pr(economic recession=1)t+12 = 0.736 – 98.37spreadt + 11.99Itshort + 98.28D3spreadt

pseudo-R2 = 0.34, Nobs = 241, bold Indicates significance at 5% MSL.

The odds of a recession are as follows.

figure 2: Estimates of the probability of recession over the next 12 months for spreads (blue), spreads and short-term rates (tan) and changes in spreads, short-term rates and 3-month spreads (green) for the period 1986-2023M10. NBER-defined recession peak-to-trough dates appear gray. Source: NBER and author’s calculations.

The bear steepness specification implies a 90% chance of a recession in September 2024, while using spreads + short rates it is only 66.4% (the specification’s peak probability is May 2024). Does this make me more pessimistic about avoiding a recession?Not really; this Ahmed Chin The normative probability of foreign term spreads (but no steepening measures) in September 2024 is approximately 90.8%.

{kind=link}

{kind=link}