from Anders Aslund In Project Syndicate:

And on March 8, the central bank decided to stop converting the ruble into foreign currencies, which means the ruble is no longer convertible.

More specifically, from Law 360:

[T]Citizens with accounts in U.S. dollars and other convertible currencies can withdraw up to $10,000 in cash until Sept. 9, the Bank of Russia said. No matter which currency the account is in, withdrawals will be made in US dollars at the market exchange rate of the day.

“It may take several days for banks to bring the required amount of cash to a specific branch,” the central bank said. Citizens can withdraw their remaining cash in foreign currency accounts in rubles at the market exchange rate on the issue date, the Bank of Russia added.

Russians will continue to be able to hold funds in foreign currency accounts. The Central Bank of the Russian Federation has been known to say that lenders will not sell currency to citizens for the next six months, but they can exchange cash for rubles in any amount at any time.

The latest controls on capital flows come after the Bank of Russia decided on February 28 to block foreign investors from selling Russian securities and ordered the Moscow Stock Exchange to remain closed in an attempt to stem the flow of capital. money abroad.

Meanwhile, Russian President Vladimir Putin approved a special executive order requiring foreign debts to be repaid in rubles, including bonds initially issued in foreign currencies, to maintain stability in Russian markets and protect the interests of creditors.

Fears are growing that Russia will struggle to repay its hard currency debt following a series of unprecedented financial sanctions in Britain, the United States and Europe.

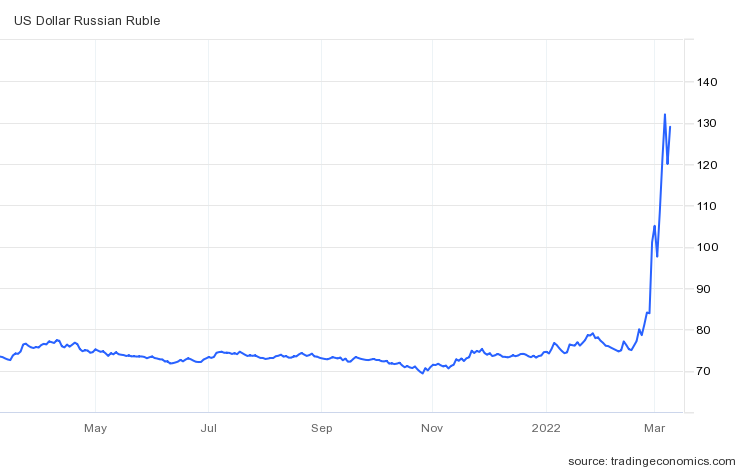

The ruble has plummeted, and despite some volatility, the value has not really recovered.

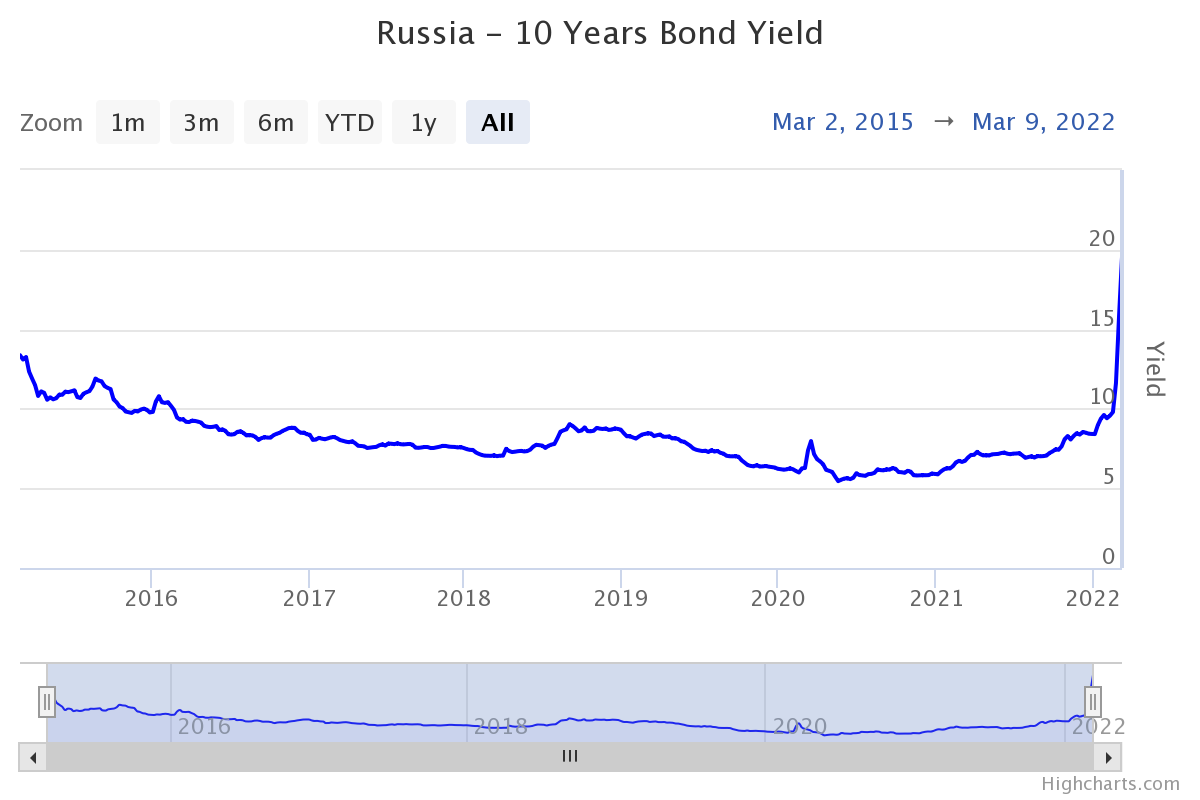

A longer-term perspective highlights the truly catastrophic nature of the collapse.

(Note: Time-averaged data in this long-span graph).

The policy rate was held at 20%, while sovereign yields soared. Again, look at the longest span available.

5-year bond CDS on March 3,412 (records dating back to 2015), assuming a 40% recovery rate and an implied PD of 6.87% (world government bonds).However, a Financial Times March 5 The article notes that implied PDs inferred from CDS can be misleading:

Russia’s five-year CDS is trading at around 45 percent upfront, a level that means investors can expect gains of more than 50 cents on Russia’s foreign debt restructuring at 50 cents. However, the bond itself is priced at around 20 cents, suggesting a much larger negative outcome for holders.

The problem could come to a head if Russia fails to pay the next interest payment on its dollar debt on March 16, which investors see as a growing possibility. Moscow this week paid interest on its ruble-denominated debt — which is not covered by the CDS — but said the money would not reach foreign holders, citing a central bank ban on repatriation of foreign currency abroad.

Some traders even fear the swaps may end up paying nothing at all, mirroring previous CDS mishaps such as car rental company Europcar in 2021 and Dutch lender SNS Realal in 2013.

Analysts at JPMorgan said the smaller size of some of the debt could mean the bonds would be out of scope for CDS if a default occurs. Six of Russia’s $15 bonds include a “backup mechanism” that allows Moscow to repay in rubles rather than dollars or euros.

The other three bonds need to be settled in Russia, which means they are effectively no longer tradable because Russian authorities have blocked offshore settlement at Euroclear.

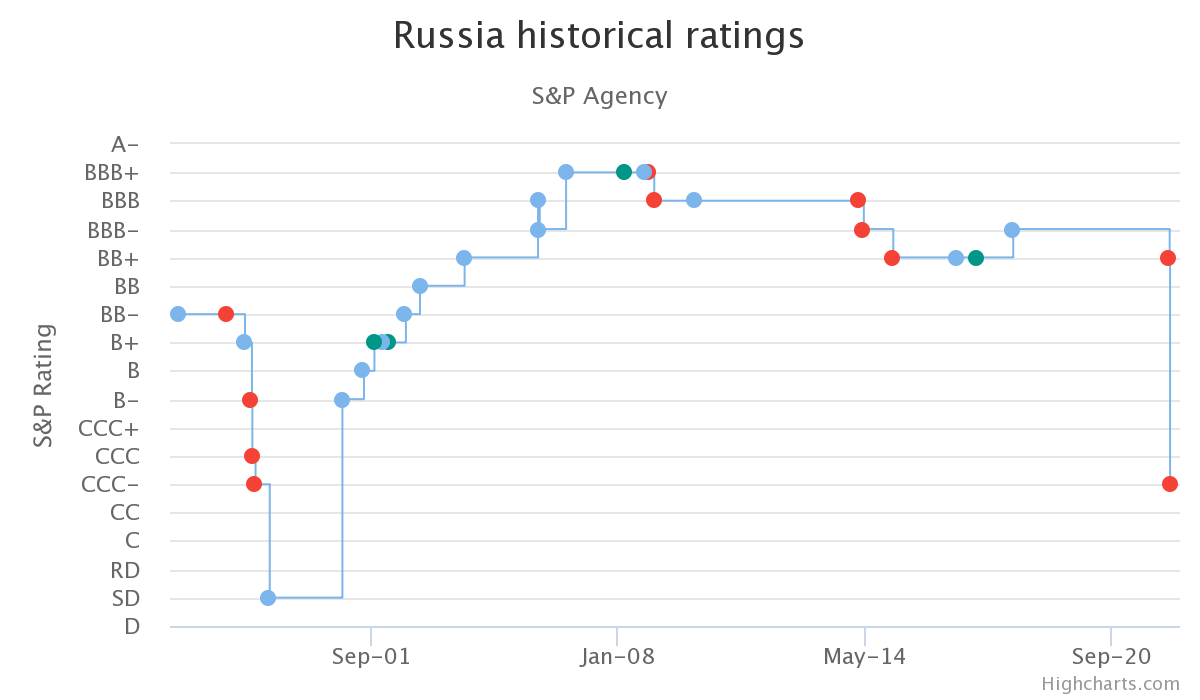

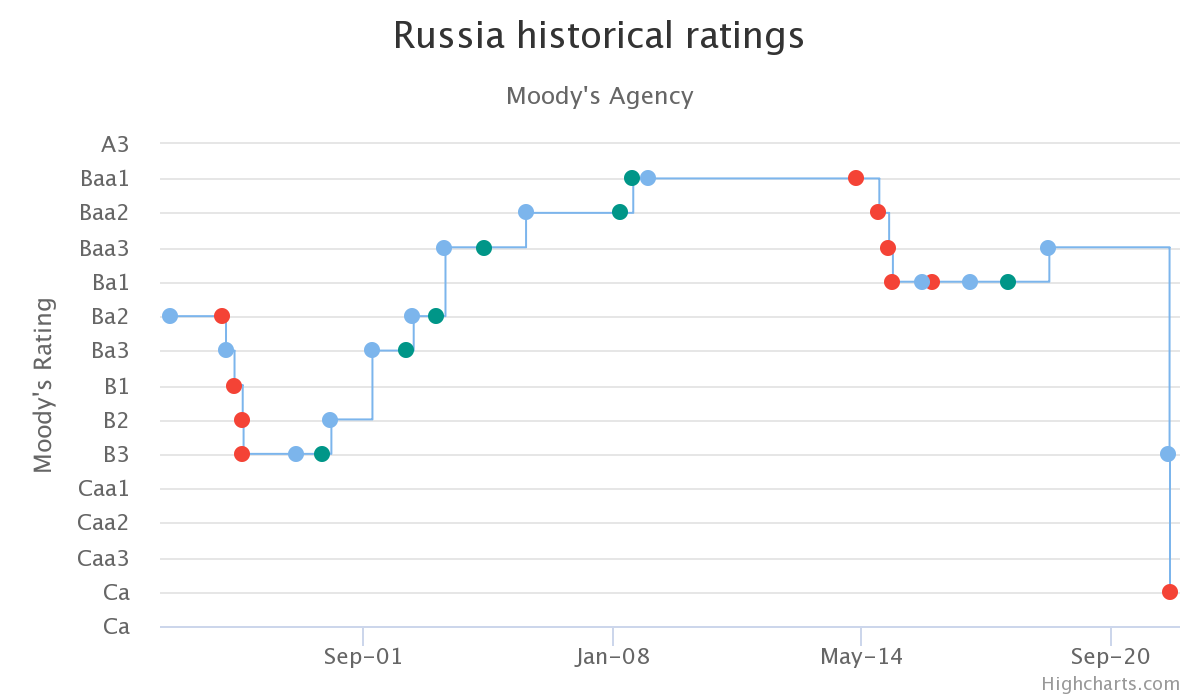

This is a time series of Russian sovereign debt credit ratings from S&P and Moody’s.

So we are heading towards a (very) possible sovereign default.

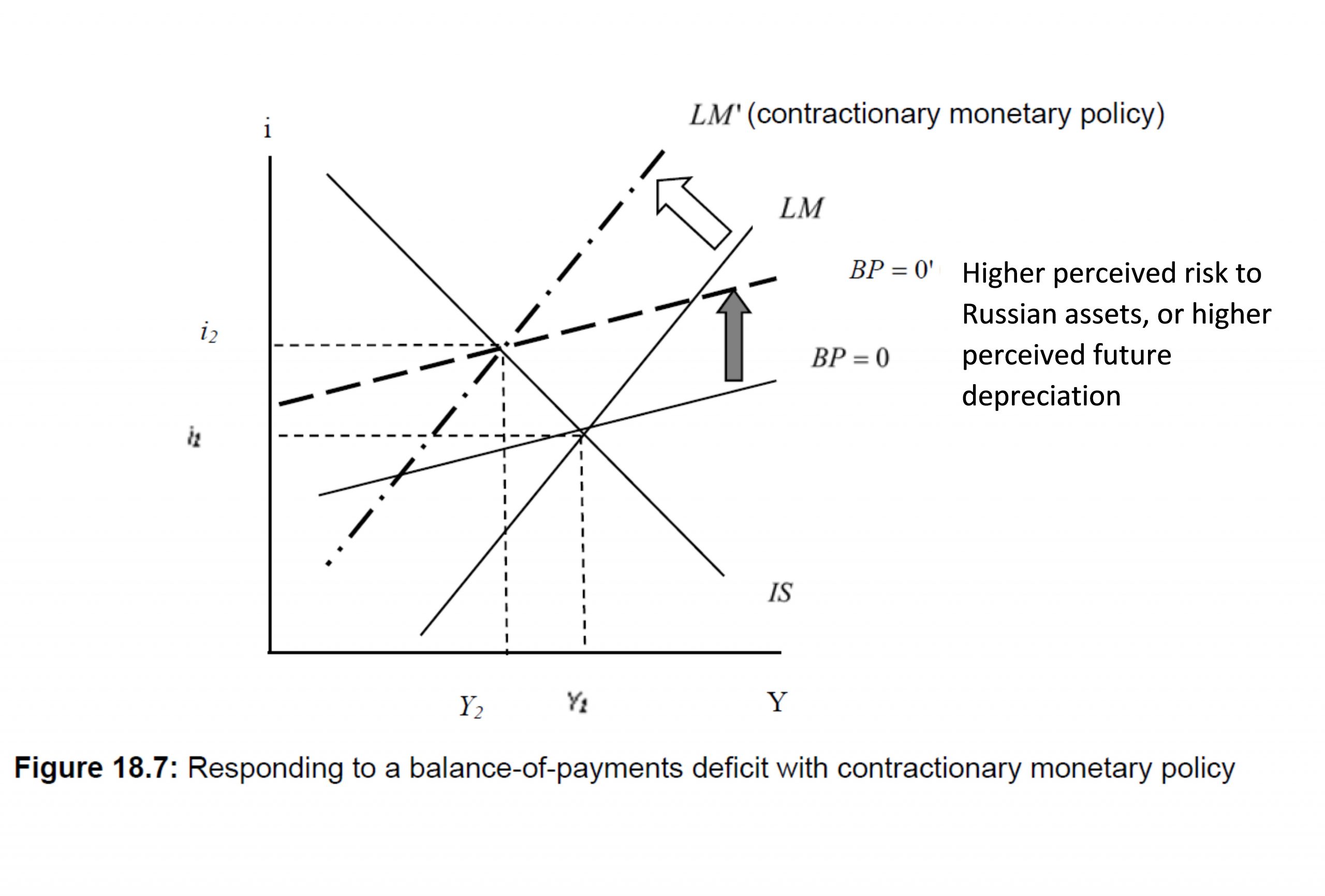

two weeks agoI interpret the external macro situation like this:

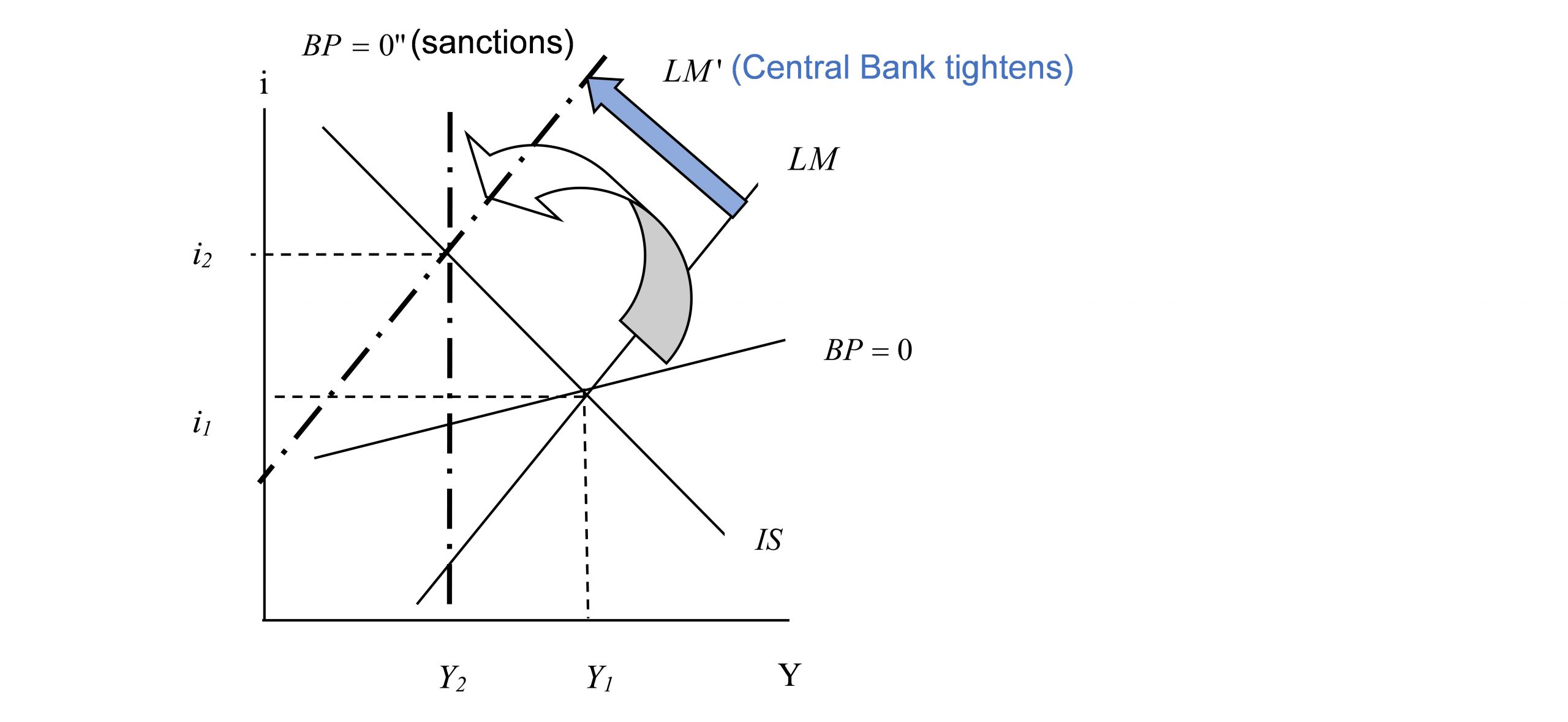

This description is no longer relevant. The closest description would be a “sudden stop” combined with depletion of reserves. Between the imposition of sanctions and the end of currency convertibility, the situation is more like the following, with the BP=0 line spinning counterclockwise.

Figure 18-6 (modified) is from the Chinn-Irwin textbook.

at income level Y1interest rate i1, reserves are accumulating. As reserves flow out, the money supply will decrease (unless those flows are sterilized); but the central bank has raised interest rates – which I describe here as high enough to stop outflows (at i2). I’m not sure if that’s the case.If not, then usable Reserves (unfrozen) will be exhausted.

{kind=link}

{kind=link}