With yesterday’s employment release (discussed here postal), we have employment data by industry, and corresponding average hourly earnings. We don’t have the CPI for that month, but using nowcasting, we can guess how real wages might change.

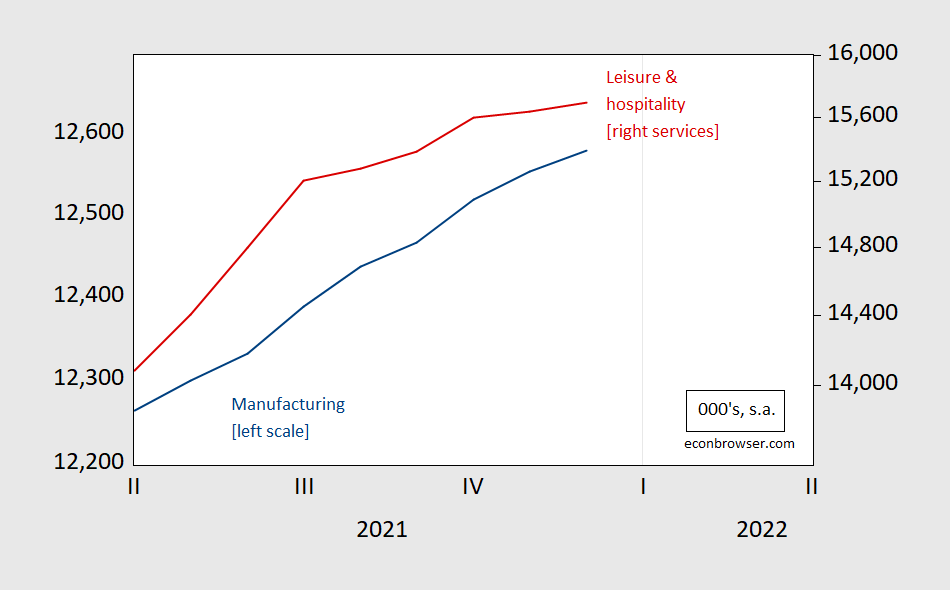

figure 1: Manufacturing employment (blue, left log scale) and leisure and hospitality services (red, right log scale), both in the 000s, sa Source: US Bureau of Labor Statistics.

Employment in the leisure and hospitality sector was flattening even before the impact of omicron was felt. Having said that, preliminary estimates for employment in the sector have been revised (relatively) sharply: 0.38 percentage points compared to 0.06 percentage points for manufacturing and 0.09 percentage points for all nonfarm payrolls.

Average hourly earnings rose rapidly in December.evolution inflation Adjusted hourly wages vary by industry. as shown in picture 2.

figure 2: Average hourly earnings for all private nonfarm payrolls (blue), manufacturing (red) and leisure and hospitality services (turquoise), production and non-managerial workers, in 2020 dollars, using December CPI from the Cleveland Fed Instant forecast value. NBER-defined recession date peaks and valleys gray shading Source: BLS, Cleveland Fed (Access 1/8) and the authors’ calculations.

Gross nonfarm payrolls and real wages in hotels and leisure rose, while manufacturing was flat.

Torsten Slok observes:

[W]Age growth at the industry level [leads to] The conclusion is that wage inflation is particularly high in contact-intensive occupations, suggesting that the virus and labor shortages for in-person businesses are key reasons why wage growth has been so strong.

…

Ultimately, the virus continues to hamper labor supply in contact-intensive industries, a key reason why upward pressure on wages is so intense. There is little the Fed can do about it, other than to cool aggregate demand quickly to avoid runaway inflation. The question for investors is whether the Fed is moving fast enough.

However, the series shown in Figure 2 does not use composition-adjusted wages. Goldman said their (nominal) “composition-corrected wage tracker was +4.1% in Q4 (+4.0% in Q3).” This compares to the implied +6.9% (and Q3 +6.7%) for the BLS overall nonfarm payrolls series (AHETPI via FRED). Inflation-adjusted component-adjusted wages will fall given the evolution of the CPI. This is not good news for labor returns. On the other hand, it breaks away from the wage-price spiral narrative.

{kind=link}

{kind=link}