Forecasters are pessimistic about April’s survey results (Figure 1). About a third forecast negative quarterly/quarterly growth in the second quarter of 2022, but the average (and median) forecast is positive growth, as shown in Figure 2 (although two consecutive quarters of negative growth are critical for determining whether the NBER BCDC declares a recession). About one-fifth of respondents forecast at least two consecutive quarters of negative growth starting later in 2022-23.

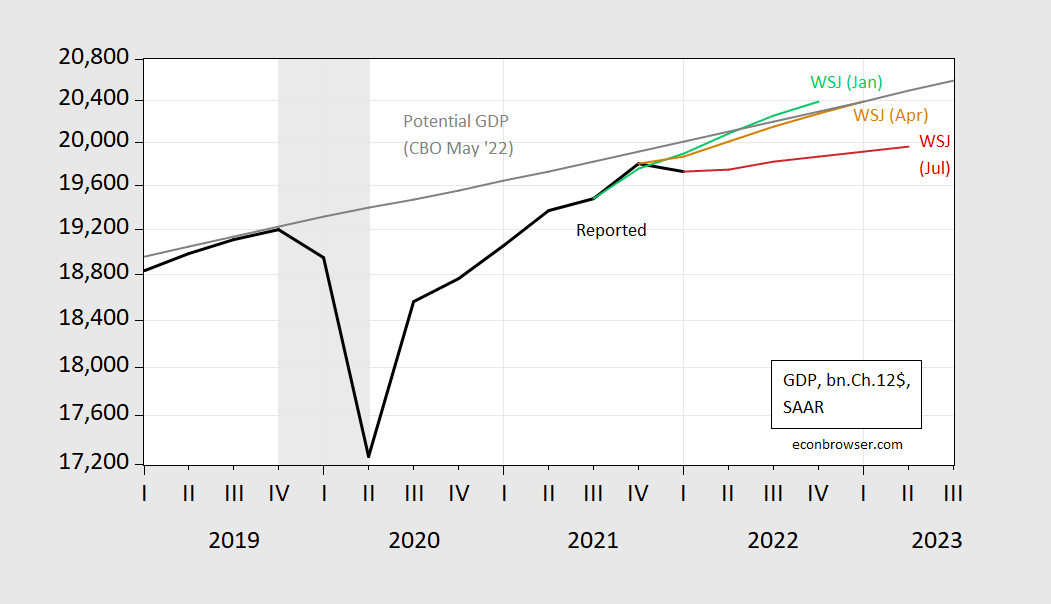

figure 1: Q1 2022 3rd edition reported GDP (black), WSJ January survey (green), April survey (tan), July survey (red), potential GDP (grey), all in billions Units Ch.2012$, SAAR, all on a logarithmic scale. NBER defines the peak and trough dates of the recession with shades of grey. Source: BEA, CBO (July 2022), Wall Street Journal investigationvarious years, NBER and author calculations.

The January survey by The Wall Street Journal showed output growth was pretty good, exceeding potential (based on CBO’s May estimates). By the time of the April survey, that trajectory had declined more than a month after Russia expanded its invasion of Ukraine and oil prices soared accordingly. As of the July survey, the average response predicted a sharp decline in that trajectory, with the implied output gap widening to -2.6% by the second quarter of 2023 (based on CBO estimates of potential, not respondents’ estimates).

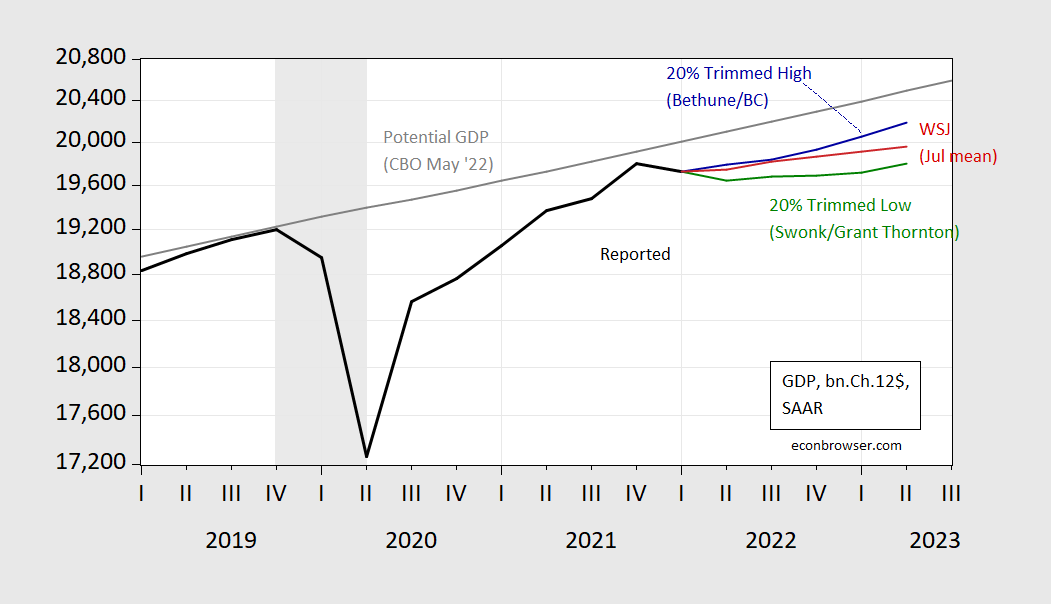

There are some notable differences in forecasts. This is hinted at in Figure 2, which shows 20% trimmed top and bottom observations (ranked based on Q4/Q4 2022 growth).

figure 2: Q1 2022 3rd edition reported GDP (black), Diane Swonk/Grant-Thornton (green), Brian Bethune/Boston College (blue), July survey average (red), potential GDP (grey), All in billions of Ch.2012$, SAAR, all on a logarithmic scale. The NBER uses shades of grey to define the peak and trough dates of the recession. Source: BEA, CBO (July 2022), Wall Street Journal investigationNBER, the authors’ calculations.

The average response implies positive growth in the second quarter. The 2022 median (not shown) looks similar, (although median respondents also see two quarters of negative growth starting in the first quarter of 2023).

Brian Bethune of Boston College tops the 20% trim sample and 2% in Q4/Q4 2022). Grant Thornton’s Diane Swonk forecasts a negative Q2 growth (-1.7% SAAR) and anemic growth thereafter, so Q4/Q4 2022 growth is only -0.5%.

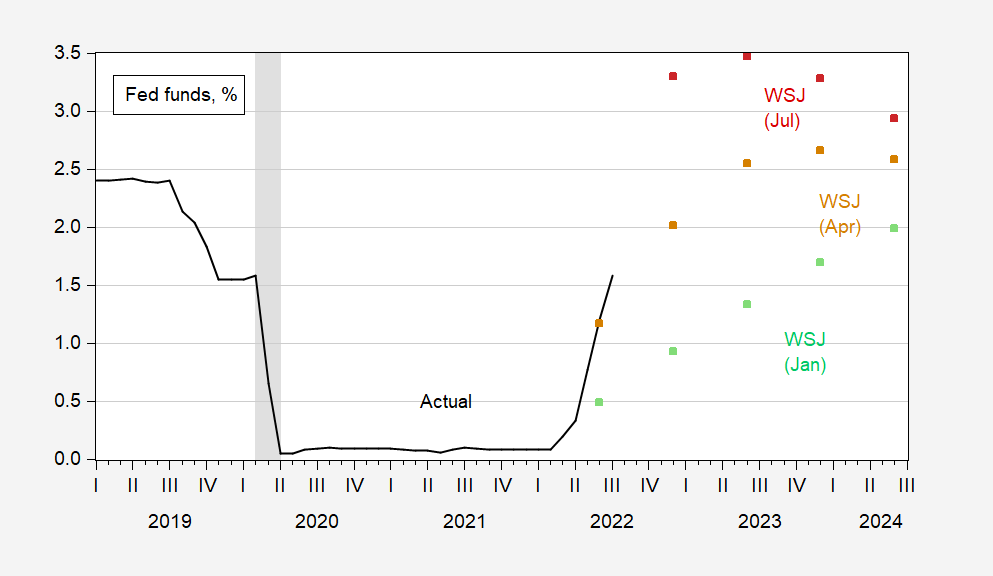

The downgrade in the growth outlook is not surprising; the narrative about raising the federal funds rate to reduce perceived inflationary pressures is shown in the rate forecast:

image 3: effective federal funds rate (black), WSJ January survey (green squares), April surveys (tan squares), July surveys (red squares), all in %. The NBER uses shades of grey to define the peak and trough dates of the recession. Source: Federal Reserve via FRED, Wall Street Journal investigationvarious years, NBER.

{kind=link}

{kind=link}