follow up first part, the second partand the third part.

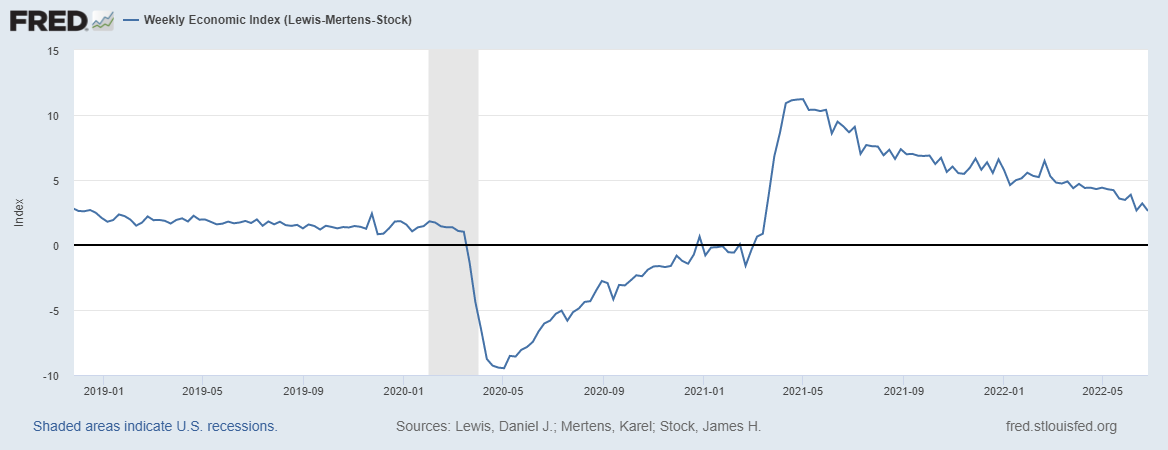

Using data as of June 25, the Lewis-Mertens-Stock Weekly Index remains in positive territory.

resource: Fredaccessed July 3, 2022.

The same goes for the OECD Weekly Tracker, using data as of June 25:

![]()

resource: OECDaccessed July 3, 2022.

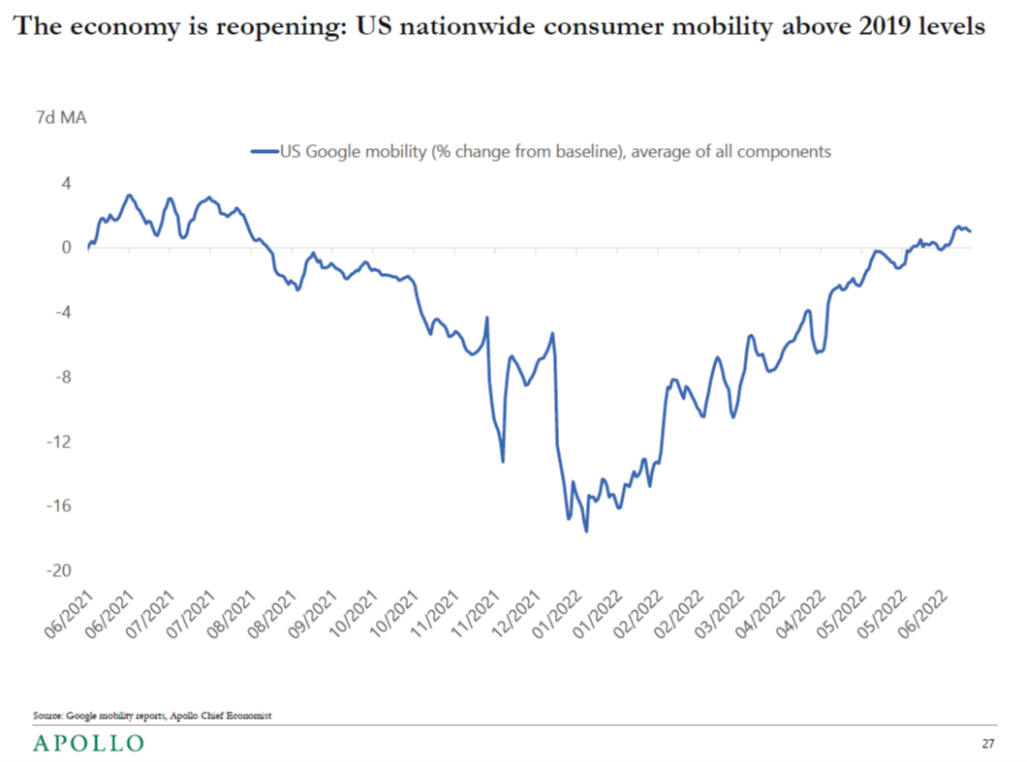

The Google Mobile Index is above 2019 levels.

resource: Torsten Slok, “Slowdown Watch,” Apollo, 2 July 2022.

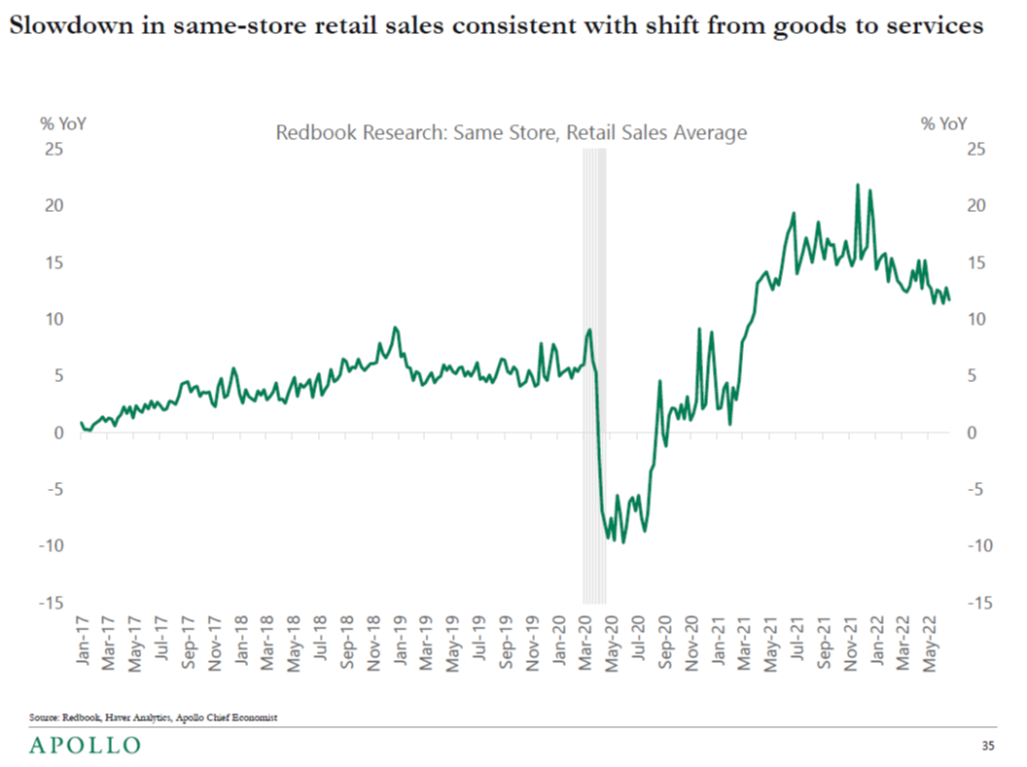

Same-store retail sales are down, but still higher than in 2019 (and higher than 2019 trends, as far as I can tell):

resource: Torsten Slok, “Slowdown Watch,” Apollo, 2 July 2022.

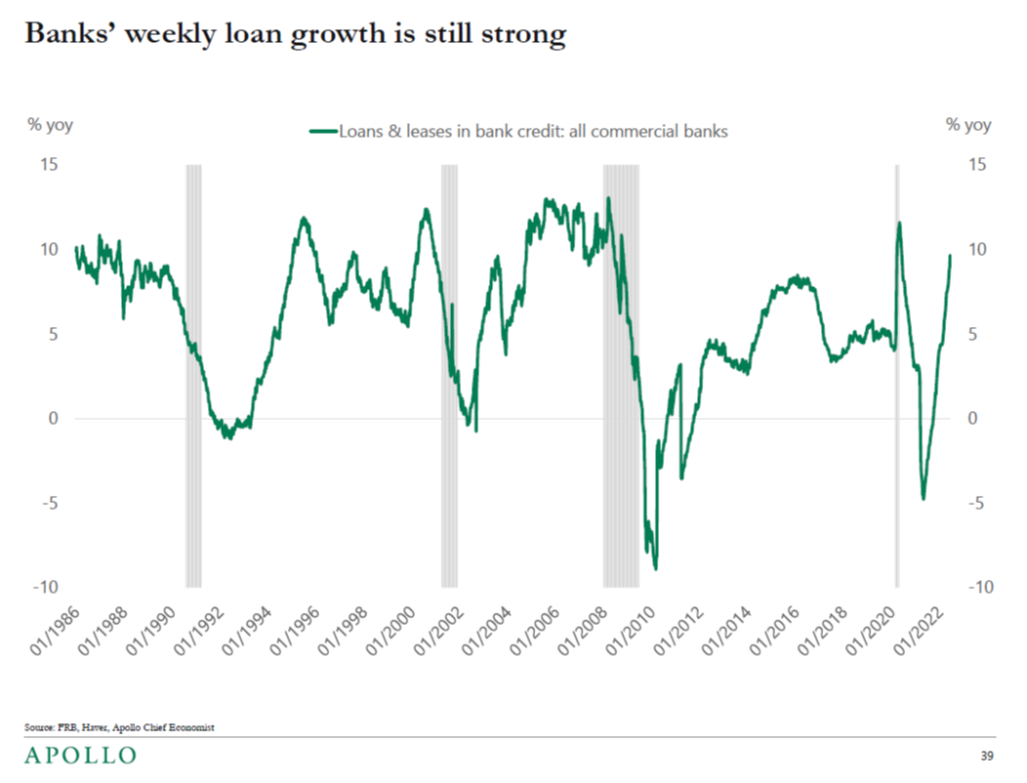

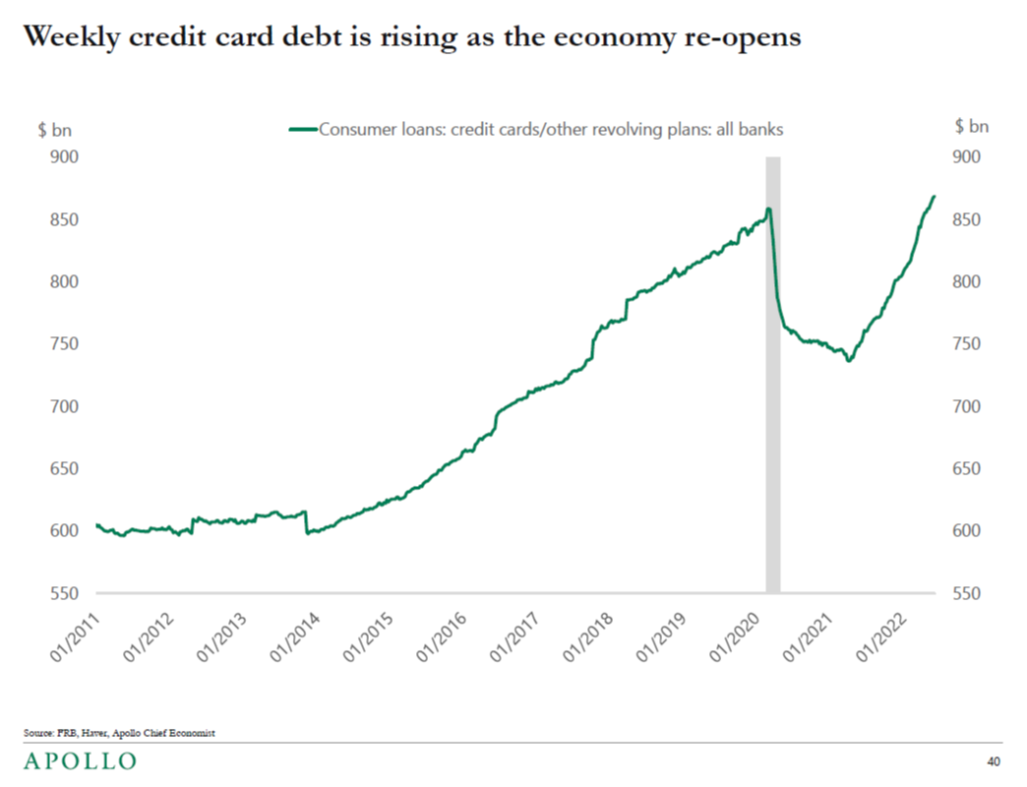

Credit metrics are on the rise, from growth in bank loans to outstanding credit card debt. Both indicate optimism about the near-term situation.

resource: Torsten Slok, “Slowdown Watch,” Apollo, 2 July 2022.

resource: Torsten Slok, “Slowdown Watch,” Apollo, 2 July 2022.

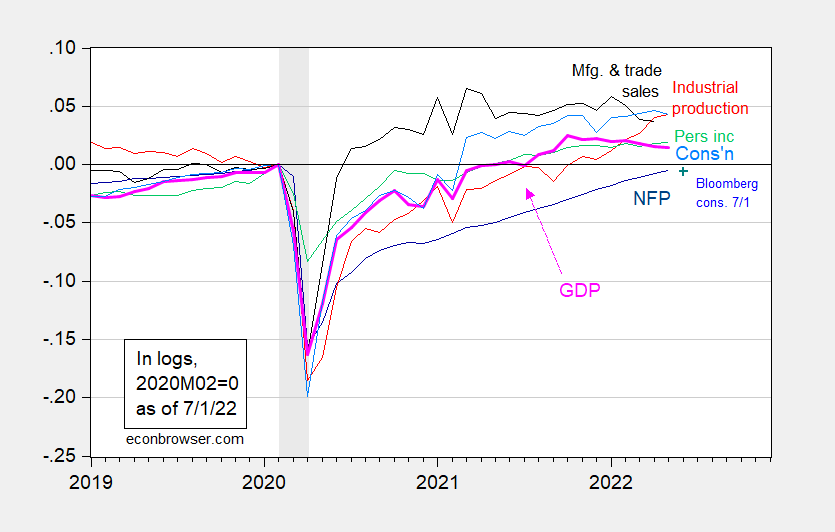

The truth is that some broad measures of activity have declined over the past few months (i.e. monthly GDP, last month’s consumption). But before employment and income. Current transfers continued to increase. As discussed in this article, monthly GDP is sometimes subject to sharp revisions.

figure 1: Nonfarm payrolls (dark blue), Bloomberg consensus on NFP (blue+), industrial production (red), 2012 personal income excluding transfers (green), 2012 manufacturing and trade sales (black), Consumption in Ch.2012$ (light blue) and monthly GDP in Ch.2012$ (pink) are normalized to 2020M02=0. NBER defines the decay date, peak to trough, shades of gray. Sources: BLS, Federal Reserve, BEA, via FRED, IHS Markit (nee Macroeconomic Advisers) (published July 1, 2022), NBER, and author’s calculations.

None of the above comments should be taken to mean that we won’t be in a recession anytime soon or by the end of 2023.Indeed, a June IGM-FT poll That shows 70% of economists surveyed believe there will be a recession next year. (More info on polls this post.)

{kind=link}

{kind=link}