this is a title Bloomberg Article yesterday. Every few years there is talk of concerted action to weaken the dollar, same as 2015. There are good reasons to expect the dollar to weaken at different times – a strong dollar and high interest rates have put pressure on the external balance of emerging markets. But does such action matter? Here are dollars and some covariates.

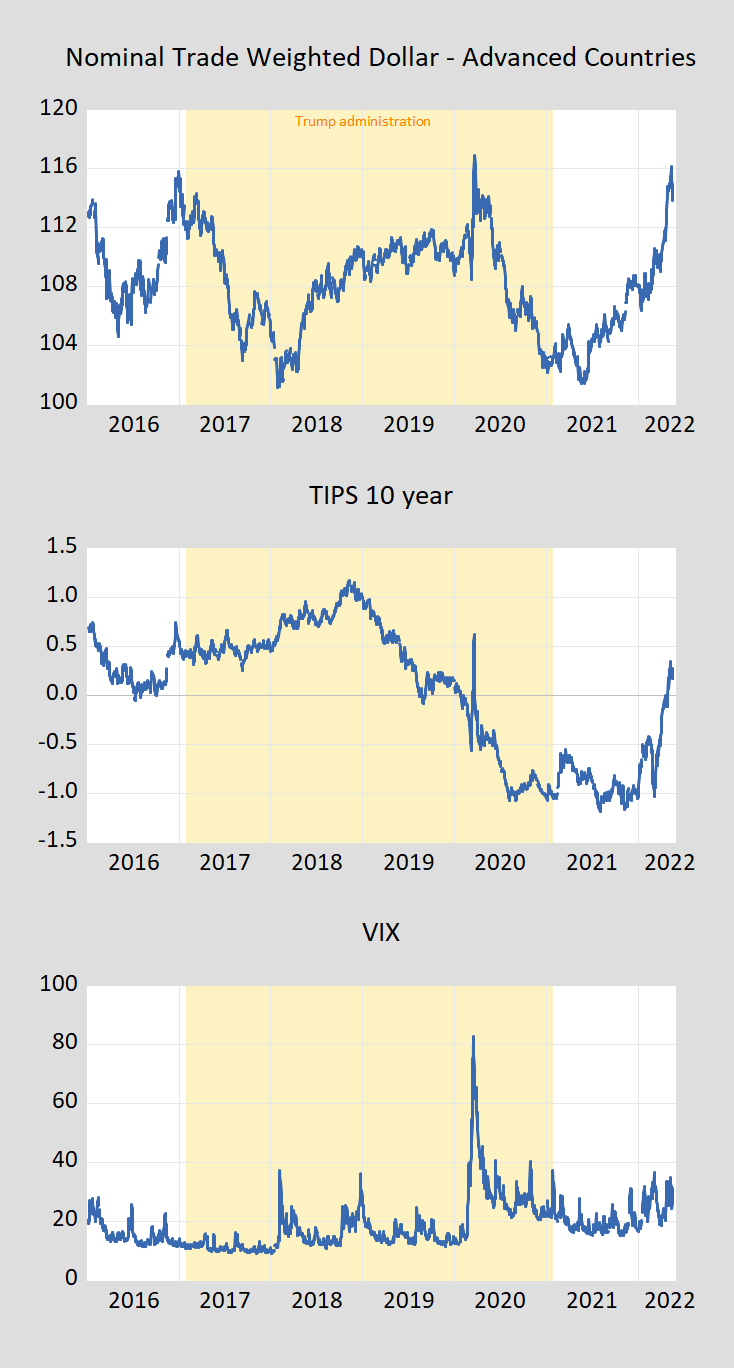

figure 1, top: Nominal trade-weighted USD (relative to advanced economies); middle panel, TIPS 10-year yield, %; bottom panel, VIX. Shades of light orange indicate the Trump administration. Source: Federal Reserve, Treasury, CBOE (via FRED).

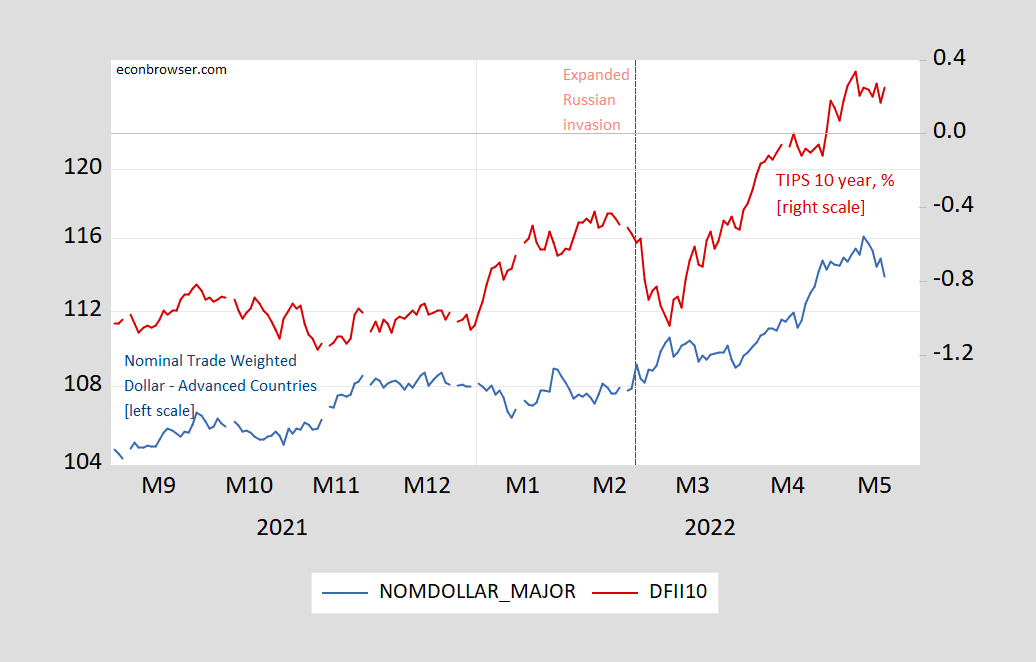

Note that the current surge in the value of the U.S. dollar is not closely related to risk appetite as measured by the VIX, but more closely related to real interest rates, suggesting that risk aversion is not the main driver of the dollar’s strength. Figure 2 shows the details of the graph.

figure 2, nominal trade-weighted U.S. dollars (blue, left log scale), TIPS 10-year yield, % (red, right scale). Last four days exchange rate extrapolated using DXY. Sources: Federal Reserve, Treasury via FRED, tradingeconomics.com and author’s calculations.

There has been a long-running debate over whether sterilized foreign exchange interventions — the buying and selling of foreign currencies by central banks while keeping the monetary base unchanged — affect exchange rates.In the early days (such as before 1990), the traditional answer was “no” (see description here). years ago, my point of view Relatively small interventions won’t have much of an impact. From a theoretical and empirical standpoint, recent assessments are more nuanced.A recent comprehensive survey of the foreign exchange intervention literature is Popper (2022).

The practice of central bank intervention was at one point ahead of convincing theoretical explanations for its use or convincing empirical evidence for its effectiveness. Research accelerated when the emerging economic crises of the 1990s and early 2000s brought new data in the form of emergency interventions and related policy experiments, and the 2008 financial crisis prompted a serious treatment of financial frictions as intervention models.

Current intervention models combine financial frictions with related externalities: aggregate demand and money externalities that now inform macroeconomic models more broadly, and trade-related externalities that are particularly relevant to developing and emerging economies. Learn about externalities. Features of these models allow for normative assessment of the use of interventions, although most (but not all) are from a single economic perspective.

Advances in experience reflect the advantages of more variation in the use of interventions, better data, and new approaches to address simultaneity. Intervention is now widely believed to affect exchange rates at least to some extent; sustained unilateral intervention and its corresponding accumulation of reserves appear to have played a role in moderating exchange rate volatility and reducing the likelihood and damaging consequences of financial crises.

Key avenues for future research include identifying the most important frictions and externalities, and where interventions – and perhaps international collaborations – are suitable (if any) and may appropriately address externalities policy mix.

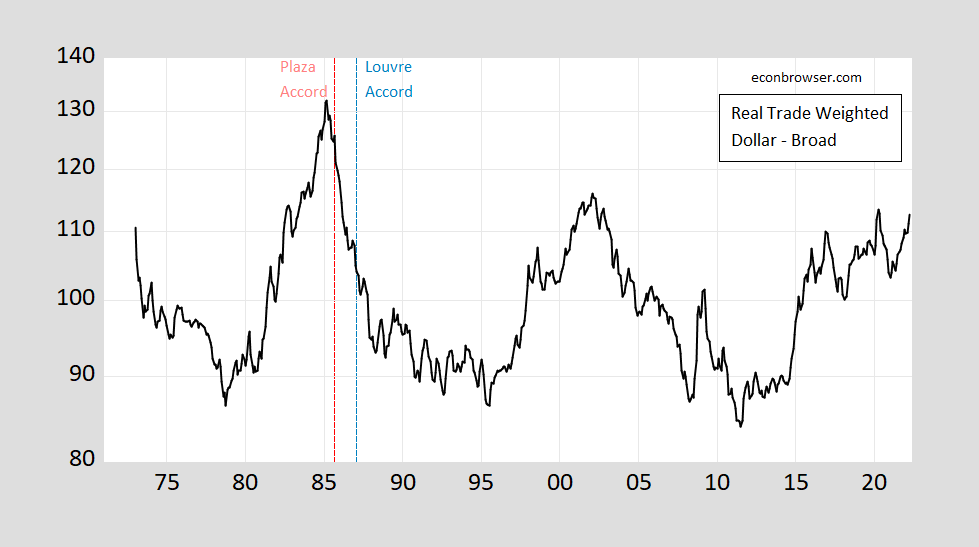

I’m ignoring the question of whether the dollar is overvalued (see this post for a discussion of what that means). The truth is that the dollar is strong based on price—though not as strong as it was in 2002, and certainly not as strong as it was in 1985.

{kind=link}

{kind=link}