Well, things got interesting in America. The Fed begins raising interest rates in April 2022, basing its decision on a theoretical framework that suggests unemployment is higher than what it considers the natural rate of interest (the rate at which inflation is stable). Thus, rate hikes are designed to slow spending and increase unemployment, and cause price makers to stop accelerating price increases. Except that the data doesn’t match theory, and inflation is falling despite the rate hikes, not because of them. This is another demonstration of how flawed dominant mainstream economics has become. Last Friday (January 3, 2022), the U.S. Bureau of Labor Statistics (BLS) released the latest labor market data—— Employment Situation Summary – January 2023 – This reveals continued and very strong job growth, rising participation and falling unemployment. These bode well for American workers. In addition, with inflation now falling, nominal wages rose moderately in most industries, and real wages rose as well—another benign sign. The latest data is certainly at odds with the Fed-type narrative. The point is that the labor market is behaving nothing like the hypothetical models deployed by the Fed.

Overview January 2022 (seasonally adjusted):

- Employment rose by 517,000 – booming.

- Labor Force Survey Total Employment Net Increase of 894K (0.56%) – Strong.

- The net increase in the labor force was 866,000 (0.52%).

- The participation rate rose 0.1 percentage point to 62.4%.

- The measure of total unemployed fell by 28,000 to 5.694 million.

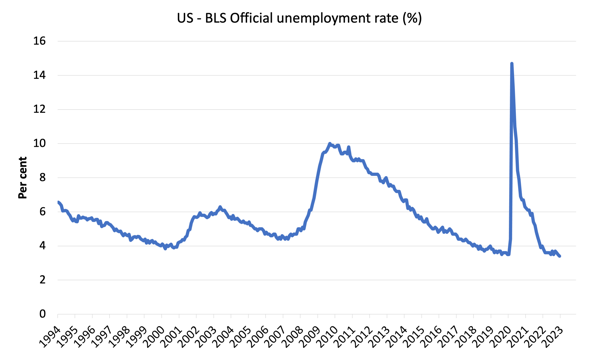

- The official unemployment rate fell 0.1 percentage point to 3.4%.

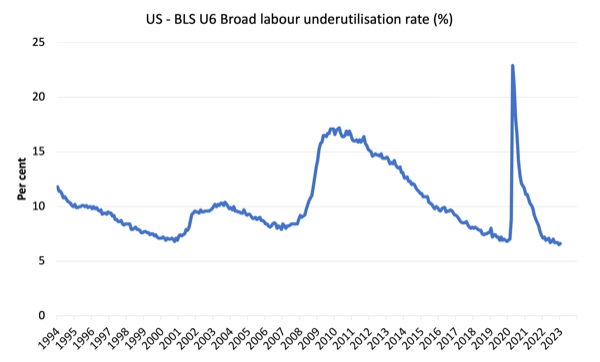

- The broad measure of labor underutilization (U6) rose 0.1 percentage point to 6.6%.

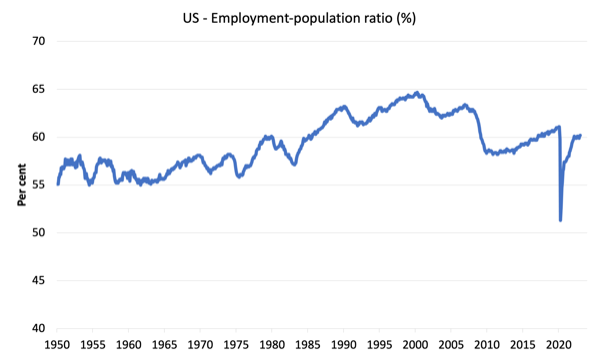

- The employment-to-population ratio rose 0.1 percentage point to 60.2% (still well below the May 2020 peak of 61.2).

For those confused about the difference between wage (institutional) data and household survey data, you should read this blog post – The U.S. labor market is in bad shape – I explain the differences in detail here.

Some months have very small differences, while others have large differences.

This month, the difference is a bit big.

Salary Employment Trends

The U.S. Bureau of Labor Statistics states:

Total nonfarm payrolls rose by 517,000 in January, compared with the 401,000 monthly average for 2022. Job gains were broad-based in January, led by gains in leisure and hospitality, professional and business services, and health care…

The leisure and hospitality industry added 128,000 jobs in January and will add an average of 89,000 jobs per month in 2022…still 495,000, or 2.9%, below its pre-pandemic level in February 2020.

Employment in professional and business services rose by 82,000 in January…on average 63,000 per month through 2022.

Government payrolls rose by 74,000 in January. Employment in the state education sector rose by 35,000, reflecting the return of university staff following the strike.

Health Care Added 58,000 Jobs In January…The health care industry will add an average of 47,000 jobs per month through 2022.

Retail payrolls rose by 30,000 in January, following negligible net gains in 2022 (+7,000 per month on average)…

The construction industry added 25,000 jobs in January…an average of 22,000 per month through 2022.

Transportation and warehousing added 23,000 jobs in January, the same as the industry’s average monthly gain in 2022…

Employment on social assistance increased by 21,000 in January, not far from the 19,000 average gain per month in 2022.

Manufacturing employment continued its upward trend in January (+19,000). Manufacturing will add an average of 33,000 jobs per month in 2022.

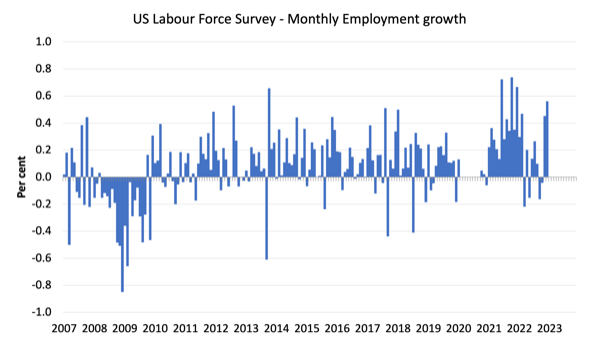

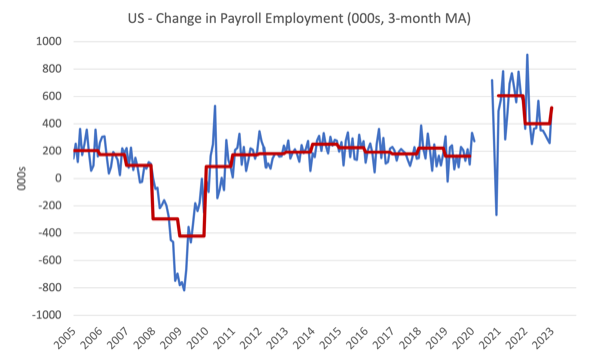

The first graph shows the monthly change in employment (in thousands, expressed as a 3-month moving average to remove monthly noise). The red line is the annual average. Observations between January 2020 and January 2020 were excluded as outliers.

The labor market boomed in January with no signs of collapsing or slowing down significantly.

However, some industries have still not regained the jobs lost in 2020-21.

The graph below shows the same data in a different way — in this case, the graph shows the average monthly net change in wage employment (real) for the calendar year 2005 through 2023.

The red marks on the columns are the results for the current month.

Average monthly change – 2019-2023 (000s)

| Year | Average Monthly Employment Change (000s) |

| 2019 | 164 |

| 2020 | -774 |

| 2021 | 606 |

| 2022 | 401 |

| 2023 (present) | 517 |

Labor Force Survey Data – Employment Rise, More Working-Age People Finding Jobs

Seasonally adjusted data for January 2022 shows:

1. Labor Force Survey Total Employment Net Increase of 894,000 (0.56%) – Strong.

2. Labor force net increase of 866,000 (0.52%) – strong.

3. The participation rate increased by 0.1 percentage points to 62.4%.

4. As a result (in accounting terms), the total number of unemployed fell by 28,000 to 5.694 million and the official unemployment rate fell by 0.1 percentage points to 3.4%.

These figures suggest that the labor market is quantitatively very strong.

The chart below shows monthly job growth since January 2008 and excludes extreme observations (outliers) between May and January 2020 that distort the current period relative to the pre-pandemic period.

The employment-to-population ratio is a good indicator of the strength of the labor market because the denominator, population, is not particularly cycle-sensitive (unlike the labor force), so movements are relatively clear.

The graph below shows the US employed population from January 1950 to January 2023.

In January 2023, the rate increased by 0.1 percentage point to 60.2%.

The pre-pandemic peak level was 61.1% in May 2020.

But it was the highest level since February 2019.

Unemployment and Underutilization Trends

The U.S. Bureau of Labor Statistics states:

The unemployment rate was 3.4% in January, with 5.7 million people unemployed, little changed. Little net change in the unemployment rate since early 2022…

The number of people unemployed for less than five weeks fell to 1.9 million in January. The number of long-term unemployed (27 weeks or more unemployed) was little changed at 1.1 million. The long-term unemployed accounted for 19.4% of the total unemployed in January…

The number of people not in the labor force currently wanting to work was 5.3 million in January, little changed from the previous month…

The unemployment rate fell slightly in January as employment growth was stronger than labor force growth (given the rising participation rate).

As a result, the demand side of the labor market just outstripped growth in the supply side, while other aggregates were largely unchanged.

The first graph shows the official unemployment rate since January 1994.

The official unemployment rate is narrow Measures of labor waste, which imply strict comparisons with the 1960s, for example, in terms of tightness in the labor market, must take into account broader measures of labor underutilization.

The figure below shows the BLS metric U6, which is defined as:

Total unemployment, plus all marginalized workers plus total number of people working part-time for economic reasons, as a percentage of all civilian labor force plus all marginalized workers.

As such, it is the broadest quantitative measure of labor underutilization published by the BLS.

Pre-COVID, U6 was 6.8% (January 2019).

In January 2022, the U6 indicator was 6.6%, up 0.1 percentage point, mainly due to a slight increase in the number of underemployed.

What does a salary do in the US?

Therefore, the jobs data does not suggest that rate hikes have hurt U.S. job creation.

What about wage growth?

The U.S. Bureau of Labor Statistics reports:

Average hourly earnings for all private nonfarm employees rose 10 cents, or 0.3%, to $33.03 in January. Average hourly earnings have increased 4.4% over the past 12 months. Average hourly earnings for private-sector production and nonsupervisory employees rose 7 cents, or 0.2%, to $28.26 in January.

These are modest increases.

However, the latest- Summary of BLS Actual Benefits (Published 12 Jan 2023) – Tell us:

Real average hourly earnings for all workers rose 0.4 percent from November to December, seasonally adjusted. …

Average hourly earnings rose 0.3%, while the consumer price index for all urban consumers (CPI-U) fell 0.1%.From December 2021 to December 2022, seasonally adjusted real average hourly earnings fell 1.7%.

Overall, wage growth failed to catch up and real wages fell during the 12-month period of rising inflationary pressures. But as inflation started to fall, modest wage growth led to modest increases in real wages.

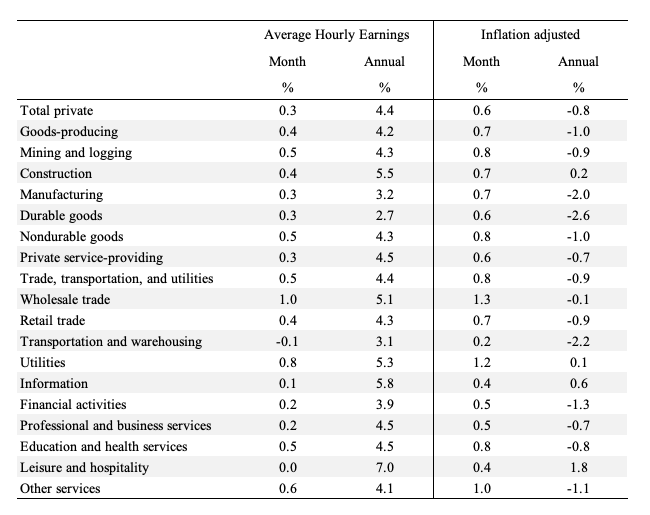

The table below shows the change in nominal Average Hourly Earnings (AHE) by industry and inflation-adjusted AHE by industry in January 2023 (note that we are using December’s CPI for adjustments – this is the latest data).

There is considerable variation across sectors, with most sectors now seeing improvements in real wage outcomes (except transport and warehousing).

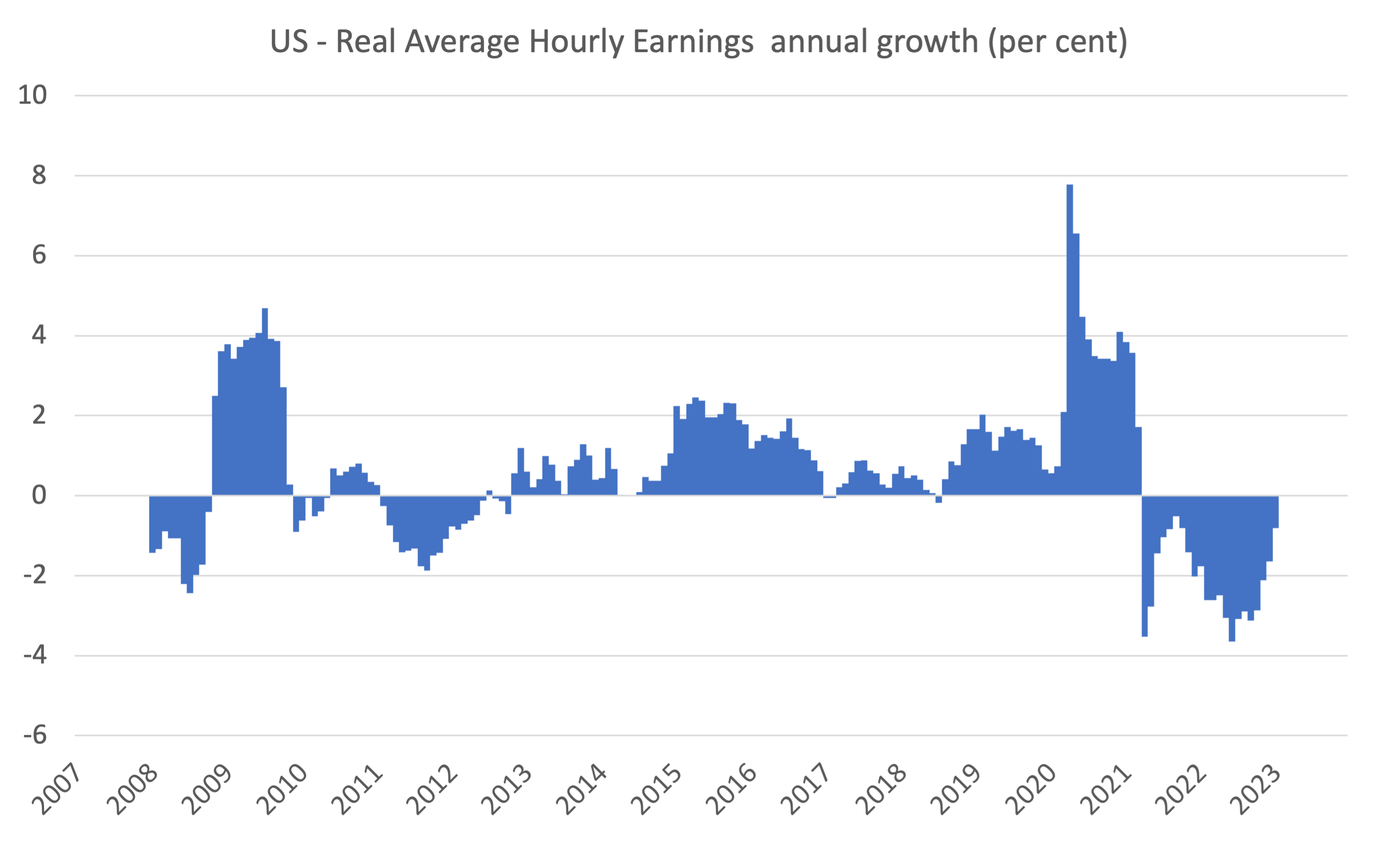

The graph below shows the annual growth rate in real average hourly earnings from 2008 to January 2023.

Another indicator that tells us whether the labor market is shifting in favor of workers is the turnover rate.

The latest BLS data — Job Openings and Labor Turnover Summary (Published January 4, 2023) – states:

On the last working day of December, the number of job openings increased to 11 million… Throughout the month, hiring and total departures were little changed at 6.2 million and 5.9 million, respectively. Little changed in departures, layoffs (4.1 million) and layoffs and layoffs (1.5 million)…

The number of quitters was little changed in December at 4.1 million, an unchanged rate of 2.7%.

If there is a recession in the U.S. labor market, the resignation rate will fall. It has been stable for a while.

in conclusion

For January 2023, the latest U.S. labor market data show strong job growth, rising participation rates and falling unemployment.

These bode well for American workers.

In addition, with inflation now falling, nominal wages rose moderately in most industries, and real wages rose as well—another benign sign.

The latest data is certainly at odds with the Fed-type narrative.

Enough for today!

(c) Copyright 2023 William Mitchell. all rights reserved.

{kind=link}

{kind=link}