In the old literature on sanctions, the costs imposed on the economy had to be considerable to bring about change (Hoffbauer Point out that the average impact of sanctions on GDP is about 2%, but not large; sanctions against Iraq are about 5%). Those announced so far for Russia won’t have that much of an impact in the short term (maybe different in the long run). However, Sever Russia’s ties with SWIFT — In addition to other restrictions on financial transactions – may be closer. Sanctions on the Central Bank of Russia, apparently under considerationmay be closer.

from Bloomberg:

The move would be “devastating” for Russia, said Tim Ash, a strategist at Bluebay Asset Management in London. “We will see the ruble collapse.”

While the decision is unprecedented for an economy the size of Russia, the U.S. has previously sanctioned rival central banks. In 2019, the U.S. Treasury Department blacklisted the monetary authorities of Iran and Venezuela for pooling funds to support destabilizing activities in their respective regions. The Central Bank of North Korea has also been blacklisted.

Some discussion on sanctioning central banks (generally) here.

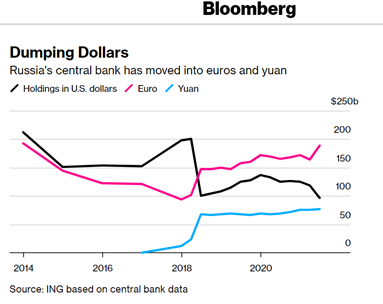

The article notes that central banks have reduced their holdings of U.S. dollars – which accounted for 16.4% of foreign exchange as of June 2021.

It is not clear to me whether the impact of US sanctions on the Russian central bank is proportional to dollar holdings.

{kind=link}

{kind=link}