A sort of reader observe:

You’re wrong because you haven’t considered statistics more holistically. This is where your students learn. If your dial is telling you different things, cross check your indicators. If employment is growing faster and faster, then GDP should also be rising. If jobs are growing rapidly, so should mobility and gasoline consumption, because so many people in this country drive to work. Finally, if productivity is collapsing while jobs are being added, you really need to pause and put together some narrative about why this is happening. It indicates an anomaly in the data that needs to be examined more closely.

So, without further ado, we provide a series of headline economic snapshots, focusing first on the indicators, then the NBER BCDC, then some alternative indicators, including Mr Kopits’ favorite, and finally the labor market indicator that we have.

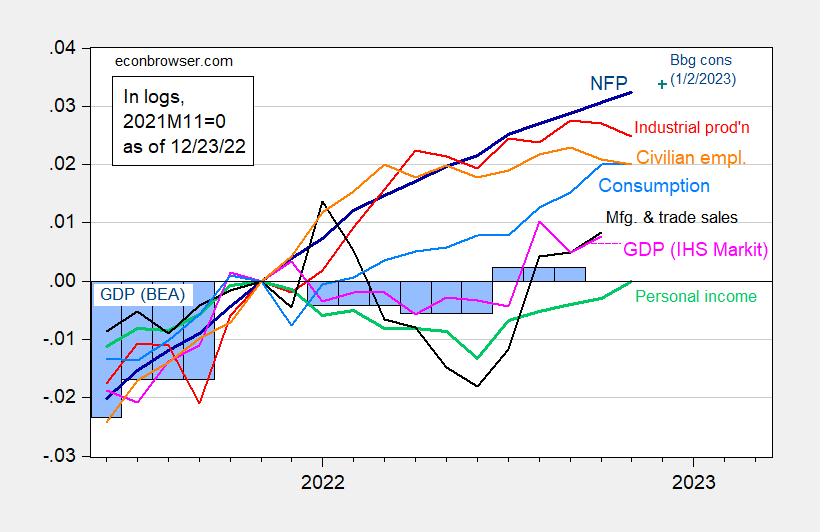

figure 1: 2012 Nonfarm Payrolls, NFP (Dark Blue), Bloomberg Consensus (Blue+), Private Employment (Orange), Industrial Production (Red), Personal Income Excluding Transfers (Green), 2012 Manufacturing and Trade Sales $ (black), Consumption $ for Ch.2012 (light blue) and Monthly GDP $ for Ch.2012 (pink), GDP (blue bars), all log normalized to 2021M11=0. Q3 Source: BLS, Fed, BEA, from FRED, IHS Markit (nee Macroeconomic Advisers) (published 12/1/2022), and authors’ calculations.

Note that official measures of nonfarm payrolls are rising through the first half of 2022, as are industrial production and consumption. Civilian employment rose but eventually flattened out, while GDP (quarterly and monthly) and personal income excluding transfers fell (before recovery). However, as mentioned several times, GDP will be revised again and again over time.

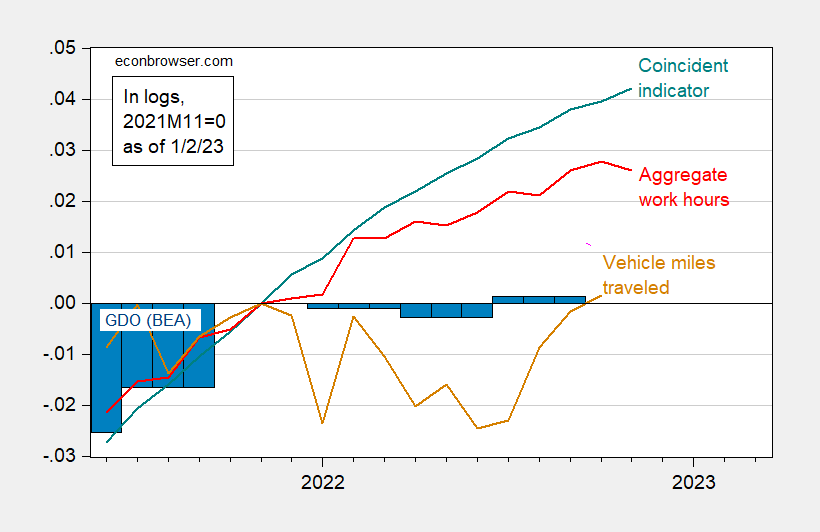

What about alternative indicators?this Federal Reserve Bank of Philadelphia A simultaneous indicator is provided for the country. I plotted this, along with total hours worked, Mr Kopits’ preferred measure, vehicle miles driven, again normalized to 2022M11.

figure 2: Concurrent Index (teal), Private Nonfarm Employees’ Total Weekly Hours Index (red), Vehicle Miles Traveled (tan), and GDO$ (blue bars) from Ch.2012 for the U.S., all seasonally adjusted Adjusted, Nov 2021 log = 0. resource: Federal Reserve Bank of PhiladelphiaBLS, FHA via FRED release), BEA, and author’s calculations.

Indeed, vehicle miles traveled declined in the first half. I don’t think it’s a big mystery.

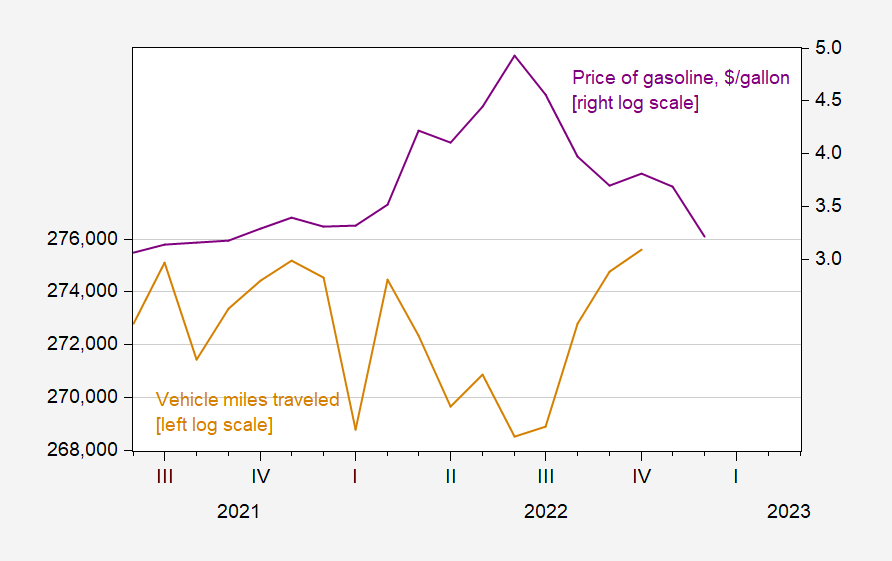

image 3: Vehicle miles driven, sa (millions/month) (tan, left log scale) and gasoline price ($/gallon) (purple, right log scale), nsa Source: FHA, EIA all from FRED.

I’d guess that the H1 drop was more due to higher gasoline prices (remember that in basic microeconomic analysis, demand usually has income and price motivations), and the January drop was due to the surge in omicron variants. So, I think VMT is an unreliable indicator (anyway, Works poorly as a coincident indicator of a recession as defined by the NBERusing a probabilistic framework).

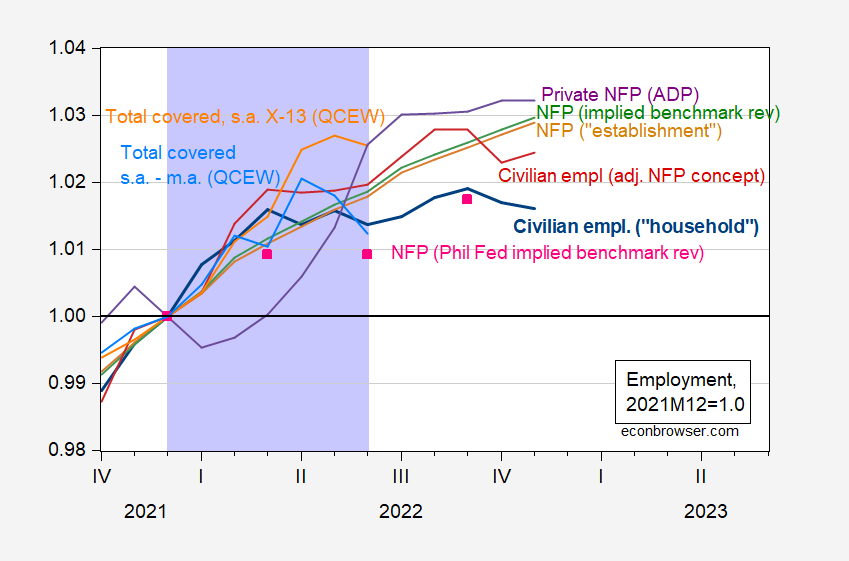

How about looking at labor market developments “holistically”, as Mr Kopits suggests? In Figure 3 I have plotted a set of indicators that have been cited, including the Philadelphia Fed’s implied benchmark revisions.

Figure 4: Civilian employment over age 16, FRED series CE16OV (bold blue), civilian employment adjusted for nonfarm employment concept (red), nonfarm employment, FRED series PAYEMS (tan), adjusted to reflect authors’ preliminary baseline revisions Nonfarm Payrolls series (green) ), Philadelphia Fed adjusted nonfarm payrolls to reflect preliminary benchmark revisions (pink squares), Quarterly Census of Employment and Wages (QCEW) total employment, X-13 Census adjustments by authors (orange), QCEW adjusted by geometric moving average (sky blue), both expressed relative to 2021M12 values, both seasonally adjusted. The lavender shading represents (by Mr. Steven Kopits) a hypothetical peak-to-trough recession in 2022H1.Source: CE16OV from BLS via FRED’s PAYEMS, Preliminary Benchmark Series constructed by the author Using data from the BLS, Federal Reserve Bank of Philadelphiacivilian employment adjusted according to the BLS’s NFP concept, the BLS’s QCEW, and the authors’ calculations.

Mr Kopits relies heavily on Federal Reserve Bank of Philadelphia to support the argument that job creation growth was small from March to June. As the Philadelphia Fed authors point out, their adjustments are less detailed than those made by the BLS, but generally more timely (BLS revisions are made annually in March).What’s interesting to me is that as briefings and Longer articles are the basis of the newsletter, with a focus on achieving higher accuracy in state-level estimates. In addition, in order to fit the latest data, the Philadelphia Fed adjusted the seasonal adjustment method.

To reduce the potential impact of extreme employment changes during the pandemic on our seasonal adjustment process, we only include data through December 2019, switch from a multiplicative to an additive seasonal adjustment process, and forecast 2020 to 2022 seasonal factors of the year.

This suggests that I am somewhat sensitive to the seasonal adjustment method, which is consistent with my differing estimates of QCEW covered employment (compare the orange line in Figure 4 with the sky blue line, the former using Census X-13 throughout and the latter always using a geometric moving average).

I’m also a little surprised that the implied March 2022 benchmark revision leaves non-farm payrolls far from the Philly Fed’s estimate for June. I don’t have a definitive answer here.

I would note that taking the civilian employment series and adjusting it to the NFP concept (dark red) shows a similar increase in the institutional series (tan). ADP’s private NFP – based on a different data set and methodology – shows an acceleration in employment in the second quarter.

So in this overall assessment, I think the question of whether employment actually grew in the second quarter (which was noticeably higher in all accounts in the first half) is an open question. On the other hand, given the evolution of macro variables – and discounting the usefulness of VMT as a recession signal as defined by NBER – I think the case for a recession in the first half of 2022 is extremely weak. (On the other hand, considering industrial production trajectories, total hours and High frequency (weekly) indicators.

Beside: Mr Kopits wrote:

Finally, if productivity is collapsing while jobs are being added, you really need to pause and put together some narrative about why this is happening. It indicates an anomaly in the data that needs to be examined more closely.

Well, mechanically speaking, 2022H1 employment increases and output (GDO) growth stagnates, exactly meaning negative productivity growth. Literally, the (real) output of the nonfarm business sector (NFB) per hour is the (real) output of the NFB sector divided by NFB employment. Man, you can’t make up for this stupidity. There is an interesting question, why does productivity drop? But that’s not the question that confuses Mr. Kopitts.

{kind=link}

{kind=link}