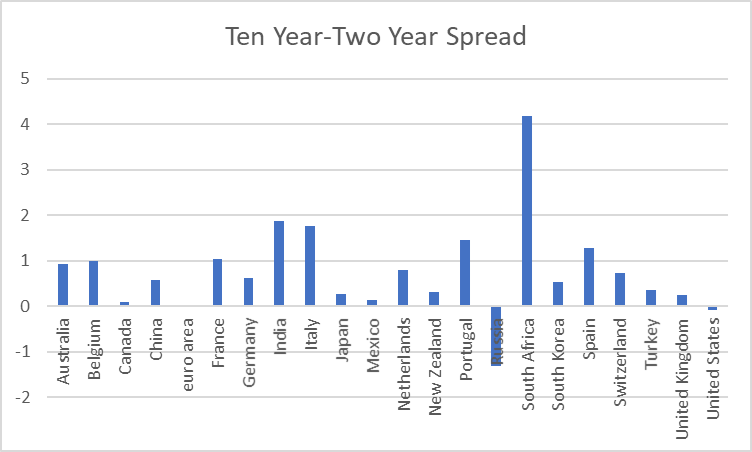

There has been a lot of talk about an inverted U.S. yield curve, especially negative 10- to 2-year spreads. The chart below depicts the 10- to 2-year spread (2s10s) for several economies.

figure 1: 10 years to April 1, 2022 minus 2-year spread, %. Source: WorldGovernmentBonds.com, accessed 2 April 2022.

Note that there are few cross-country studies on the predictive power of such spreads for recessions. Chin & Cook (2015) Analysis 10yr-3mo, Flour (2014) Investigate 5yr-3mo in emerging markets. Haubrich (2021) [ungated 2020 wp version] Some recent cross-country evidence is reviewed.

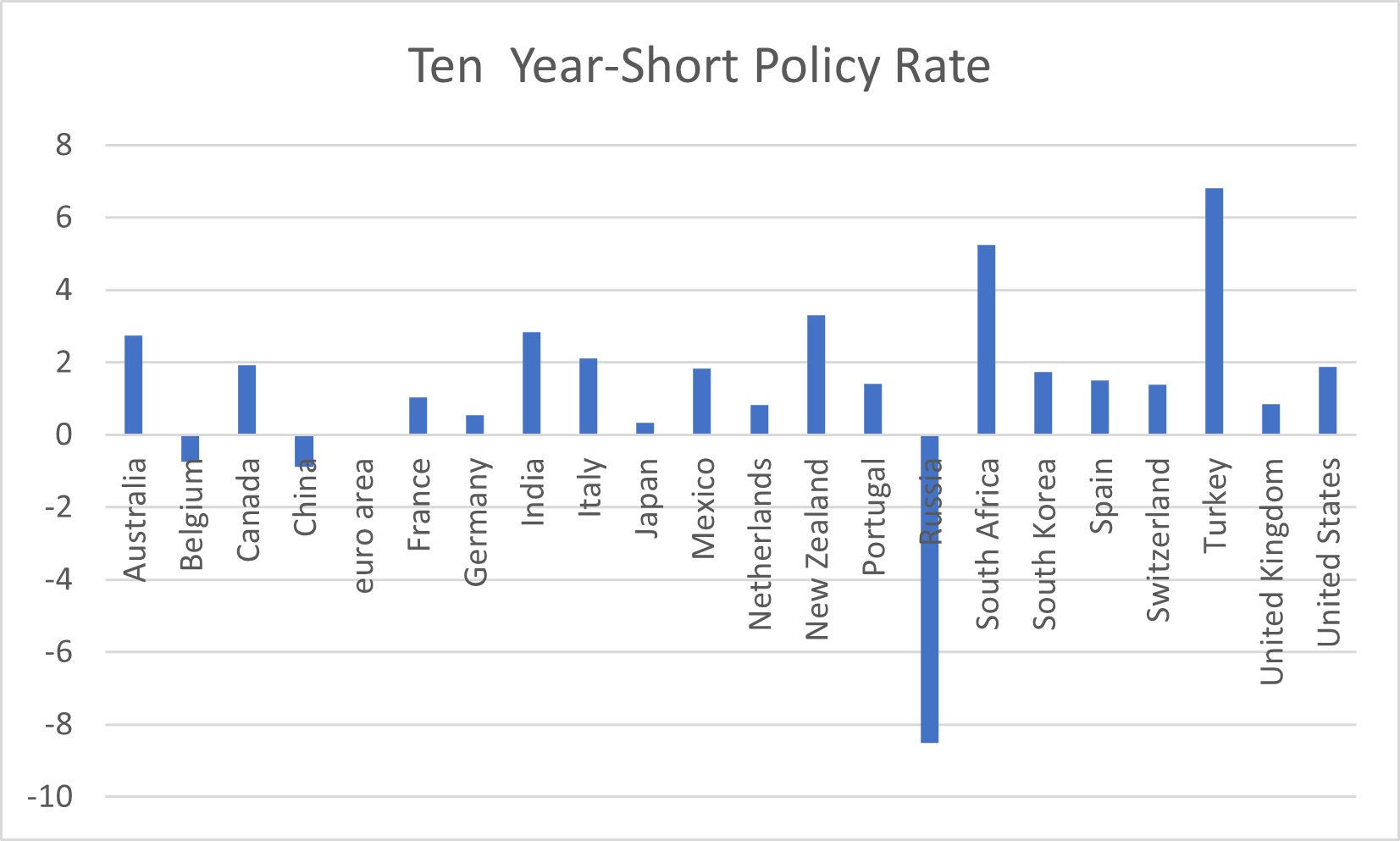

The Economist used to report 10-year and 3-month rates in simple form, but it stopped a while ago. TradingEconomics.com reports 10-year rates and policy rates. This is a graph comparable to Figure 1.

figure 2: 10 years to April 1, 2022 less policy spreads, %. Source: TradingEconomics.com, accessed April 2, 2022, and author’s calculations.

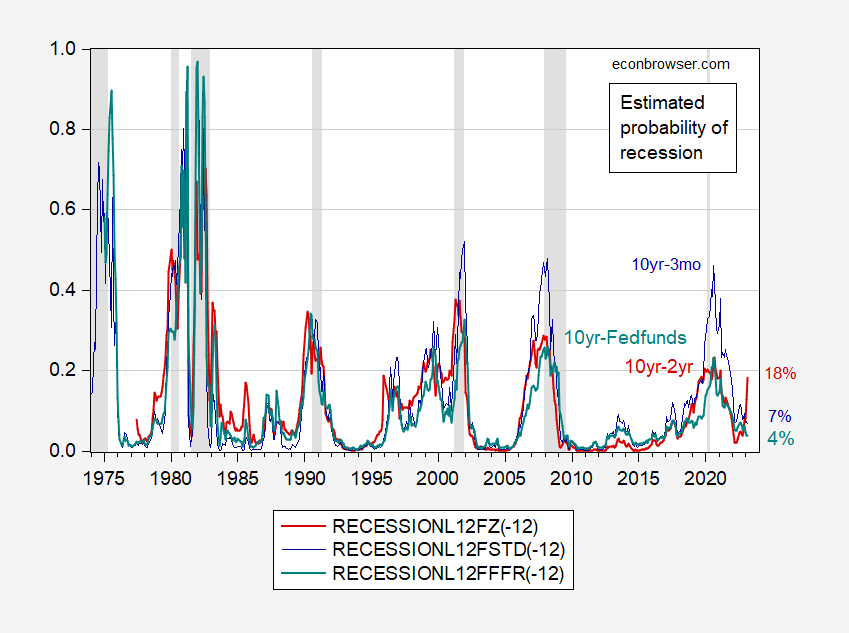

how to view these developments. Recession probability charts for US 10-year to 2-year and 10-year federal funds (blue, turquoise, respectively) and comparing 10-year to 3-month (red). Implying that we probably don’t want to focus too much on 2s10s (even if this reversal happens before all the recessions we have the data for).

image 3: Use the 10-year to 3-month Treasury spread (blue), the 10-year to 2-year spread (red), and the 10-year federal funds (actual) to estimate the recession probability 12 months ahead. Recession dates as defined by NBER are shaded from peak to trough in gray. Source: Treasury via FRED, NBER and author’s calculations.

{kind=link}

{kind=link}