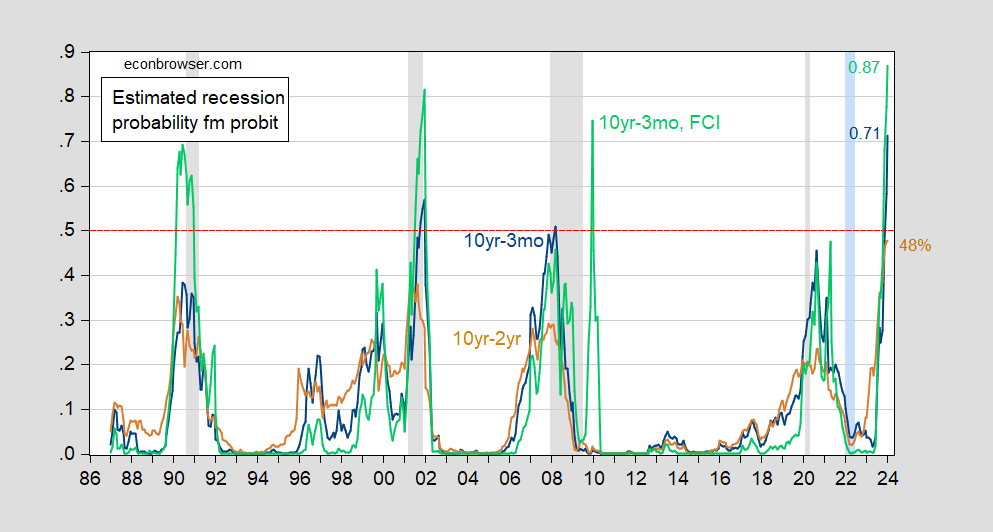

Ordinary probability models suggest a high probability of a recession, especially using the 10yr-3mo spread:

figure 1: Recession probabilities projected by 10-year to 3-month spread (blue), 10-year to 2-year spread (tan), FCI widened 10- to 3-month spread (green). All models estimated to be over 1986M01-2023M01. Dates of peak-to-trough recessions as defined by NBER are shaded in gray. A dashed red line with a probability of 50%. Source: Author’s calculations, National Bureau of Economic Research.

The 10yr-3mo spread implies a recession probability crossing the 50% threshold; while the 10yr-2yr does not, it is very close. Adding the financial condition index pushes the probability up to 87%, but this specification also produces false positives in 2009-10.

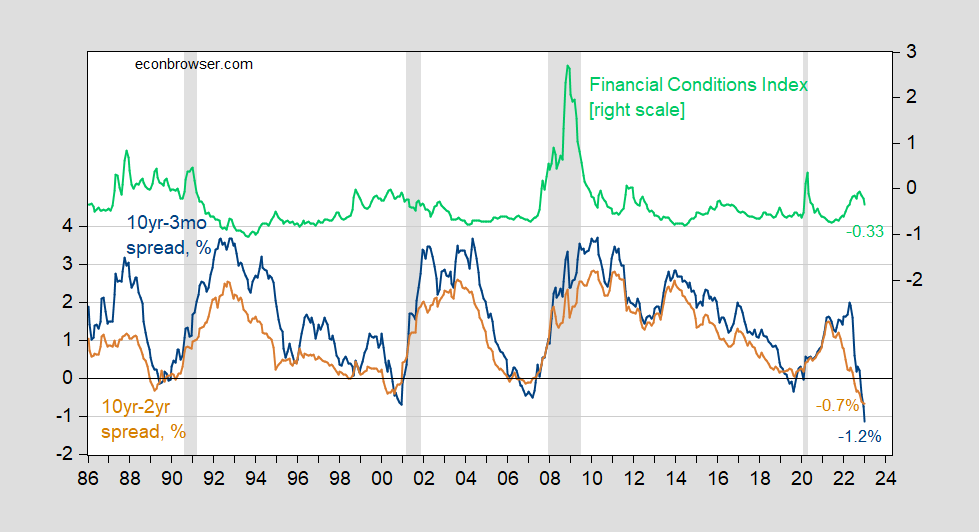

These are spreads as of today (January data as of January 30).

figure 2: U.S. Treasury 10- to 3-month term spread (blue, left scale), 10- to 2-year (tan, left scale), both in %, and Chicago Fed National Financial Conditions Index (green, right scale ). Spread to 1/30 in January 2023; FCI through 1/20. Dates of peak-to-trough recessions as defined by NBER are shaded in gray. Sources: Treasury Department, Federal Reserve Bank of Chicago, via FRED, NBER, and author’s calculations.

Interestingly, one of the main early proponents of the term spread as an indicator, Campbell Harvey thinks this time is different:

Although the curve is inverting for the ninth time since 1968, Harvey said it may not be a harbinger of recession.

…

“Dodge Bullets”

Harvey, whose model correlates to inflation-adjusted yields, said the fact that inflation expectations have inverted — meaning traders see price pressures easing over time — also reduces the likelihood of a future recession sex.“When you put all of this together, it shows that we can dodge a bullet,” Harvey said. “Avoid a hard landing — a recession — and achieve slow or slightly negative growth. If a recession comes, it will be mild.”

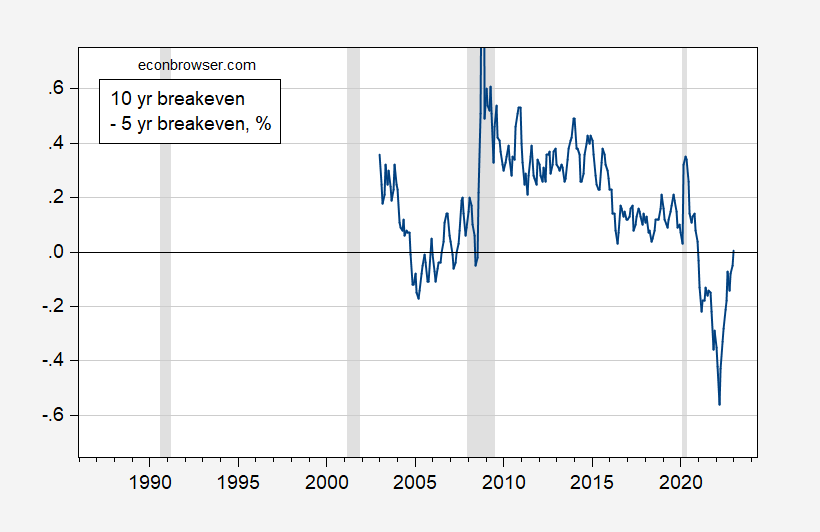

In fact, the term structure of inflation expectations has also (or was) inverted, contrary to what happened in 2007-09 and before the 2020 recession.

image 3: 10-year inflation breakeven minus 5-year inflation breakeven, calculated using Treasury-TIPS spread, % (blue). Dates of peak-to-trough recessions as defined by NBER are shaded in gray. Source: Treasury Department calculations based on FRED, NBER, and authors.

The Philadelphia Fed’s estimated term structure of inflation expectations suggests that longer-term expected inflation is lower than it was a year ago or even a month ago (see Philadelphia Fed Estimates). He reiterated this a few hours ago [video].

So, we’ll see if this time is actually different…

[I don’t have ready access to the foreign term spread for January, so I can’t estimate the Ahmed-Chinn specification.]

{kind=link}

{kind=link}