Given the recent debate over whether we’re back to the 1970s, where the only superficial resemblance is that inflation has accelerated over the past year or so, I dug into my data archives to remind myself of something. One of the problems with dealing with official data is that it is revised from time to time and the time series becomes discontinuous. Consequently, labor market data for Australia tends to start from February 1978, when the Australian Bureau of Statistics switched to monthly labor force surveys. Researchers who want to study historical data must have been there for a while and saved their earlier data collection (like me). But it’s often impossible to match them with newer publicly available data. You’ll see how that turns out below. But I’m also interested in going back in time today, after the latest news from the ABS — Industrial Disputes, Australia – Data (released March 9, 2023) showing controversies remain at historically low levels. So in what follows I’ll show you that the current situation is so far from what happened in the 1970s that it turns the narrative of us central bankers into a pack of lies.

History of Labor Disputes

One can analyze the manifestations of class struggle in many ways—the number of disputes, the number of workdays lost, and the number of employees involved.

The ABS current industrial disputes data series begins in the March 1985 quarter and provides data for all three measures through the December 2022 quarter.

The first graph shows three series from that period, and while there is a lot of noise in the data, the trend is clear.

The reduction in industrial disputes is enormous and is the result of public policy that deliberately weakens unions and makes it easier for bosses to sue unions engaged in industrial action.

This decline marked the beginning of the period when the government was transformed from a mediator in the struggle between labor and capital to an agent of capital.

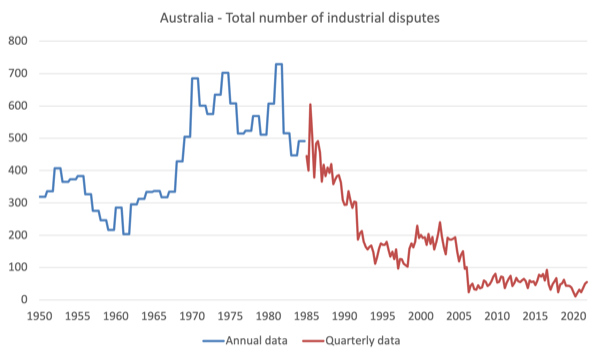

But by piecing together older annual data from 1950 to 1984 with the current quarterly data shown in the chart above, we can get a better idea of how the field of industrial relations has changed.

The chart below shows the number of labor disputes from 1950 to the December quarter of 2022 (data are annual data up to 1985, then quarterly data).

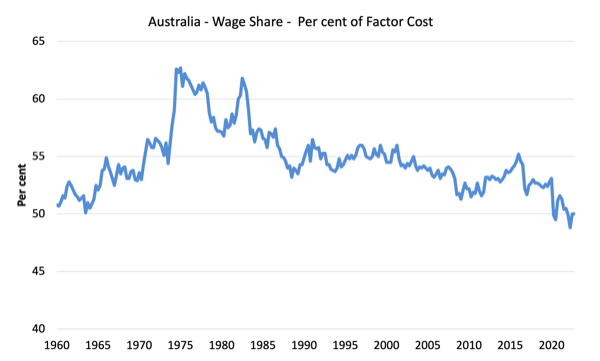

Additionally, we have consistent wage share data from the September 1959 quarter through the December 2022 quarter, as shown in the chart below.

The distribution of national income in terms of wage share began the period (March to 1985) at 56.6% (after a peak of 62.7% in the March quarter of 1975).

The wage share has been reduced to 50% by the December 2022 quarter.

It is easy to see that wage shares are higher when unions are able to effectively represent the interests of their members.

The problem is that union membership has declined dramatically since the mid-1970s.

history- Trade Union Statistics, Australia, December 1975 – Indicating an upward trend in union membership for the year:

Total membership increased by 52,100 (1.9%) • Total membership increased by 52,100 (1.9%) from 1974 to 2,814,000… Between 1970 and 1975, male membership increased by 12% and female membership increased by 12% , female members increased by SO%.

Measured by workforce size, we learn that:

At the end of 1975, trade union membership accounted for 58 percent of employed wage and salary earners. 58% of employed wage earners. The percentage of men is 63%, and that of women is 48%.

Really exciting.

Get a quick overview of current and latest ABS related releases – union membership – Tell a bleak story for workers:

– 12.5% of employees (1.4 million) are union members.

– Since 1992, trade union membership has fallen from 41% to 12.5%.

So in 1975, the coverage was 58%.

By 1992, this proportion had dropped to 41%.

This drops to 12.5% by August 2022.

We left the 1970s a long time ago!

Phillips Curve Analysis

To map these labor force trends (controversy and union membership) onto the inflation narrative, we need to construct some Phillips curves that relate the unemployment rate (as a proxy for the strength of labor market demand) to price or wage inflation.

The Phillips curve, first revealed in 1958, is about the relationship between wage inflation and unemployment.

In my doctoral dissertation I showed that, in fact, the origin of this relationship was much earlier, but it was the work of AW Phillips that attracted attention.

In 1960, Paul Samuelson and Robert Solow transformed the “wage Phillips curve” into a price-inflation curve, arguing that nominal wage pressures drive up unit costs, which are then passed on through markups to the final price of goods and services.

Comparable wage data are hard to come by in time because statisticians change definitions etc., creating some discontinuities.

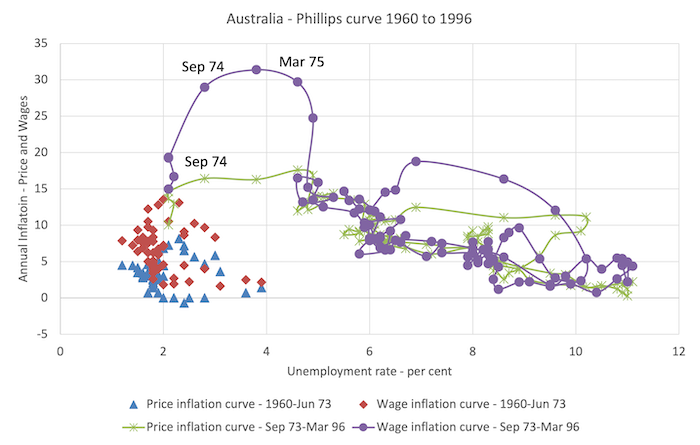

So I dug into my files and built this chart from the September 1960 quarter to the March 1996 quarter.

Importantly, the data covers the tumultuous period of the 1970s, when the OPEC oil cartel pushed up oil prices dramatically, and the resulting imported oil prices sparked a distributive struggle between workers and capital over who got the actual loss of income as lost income . The result of rising import prices.

I constructed a Phillips curve for prices and wages (annual growth rates on the vertical axis) and the official unemployment rate on the horizontal axis.

Two different “inflation” measures vary by the shape and color of the marker.

I split the data into two subsamples:

1. March quarter 1960 to June quarter 1973.

2. September 1973 quarter to March 1996 quarter.

Splits in the sample are when the industrial chaos really begins.

The lines between the observations in the second subsample can help you understand the trajectories of the wage and price inflation measures when split.

In 1974, demand for nominal wages was strong as workers defended their real wages.

Wage growth was also boosted in 1974 by a massive adjustment to public sector wages by the then Labor government.

The point is that real wage headwinds push up real unit costs (measured by the wage share) significantly, and firms then use their market pricing power to defend their margins.

Thus, the initial supply shock from rising imported oil prices quickly morphed into pervasive structural inflation in the domestic economy fueled by a distributional struggle between wages and profits.

The shift to the right in 1974 was described by monetarists as evidence of a rise in the natural rate of unemployment.

The reality is that it did mark the beginning of the deficit obsession, when the government abandoned its post-World War II commitment to full employment in favor of austerity aimed at keeping unemployment high while purging unions. Ability to increase wages for their members.

Fast track to the current period.

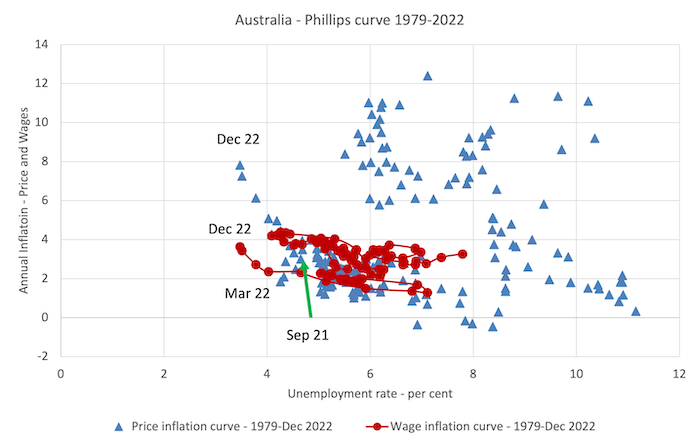

The graph below shows data from the March quarter of 1979 through the December quarter of 2022.

The difference between the episodes – the 1970s and the present – is stark.

Wage growth has been very sluggish over the past few years, and the current rate of inflation is accelerating well above it, leading to systematic and significant cuts in real wages.

The scale of these cuts is getting bigger and bigger.

The data showed there was no wage-price spiral and wage growth was little changed as inflation accelerated due to supply factors.

There is also strong evidence that firms are jacking up profits “because they can” – by using the smokescreen of rising costs, except that price acceleration far outpaces cost acceleration.

Last week I canceled a relationship with a construction industry company and I wanted some work done for me as they brought in an amended contract where the quoted price was increased by about 150% “due to rising costs”. There is no cost increase that much. They were led to the door.

Video – Current Inflation – Causes and Remedies

As part of the ongoing MMTed edX MOOC we are running, which provides free education to those who want to learn Modern Monetary Theory (MMT), I have created a new video to update the material from the last time we ran the course .

All other videos are available only to participants in this course, but I decided to make this one generally available.

I had to do it very quickly yesterday (no script) and was out of my usual shooting location so I did a quick and dirty zoom recording (with any meeting attendees) this got the job done but the quality is in how it handles the video Synchronization with audio.

But regardless, it gets the message across.

in conclusion

The point of today’s blog post is that this inflation event is nothing like what the world experienced in the 1970s.

The problem is that central bankers have been citing wage price spirals and expectations to justify their decision to raise interest rates.

The reality is that these justifications are just smokescreens and there is no justification for what is being done on the back of monetary policy.

Enough for today!

(c) Copyright 2023 William Mitchell. all rights reserved.

{kind=link}