In my 2015 book – Eurozone dystopia: groupthink and mass denial (posted May 2015) – I trace in some detail the events and views that led to the establishment of the Economic and Monetary Union (EMU, aka the Eurozone), once the Maastricht Treaty as the most advanced neoliberal Form is propelled through time. EMU differs from other countries with neoliberal policies in that in the former case the ideology is rooted in treaties, i.e. in the constitutional system, which is almost impossible to change in any progressive way. In the latter case, voters can get rid of the ideology by voting to remove the party that promotes it. True, in the current period, even parties of the social-democratic tradition have become neoliberal and have little choice. But EMU is different, with the most destructive ideologies ingrained in its legal structure. We were reminded of this recently (April 26, 2023), when the European Commission published its latest letter – Commission proposes new economic governance rules fit for the future. Once implemented, the policies advocated in this new governance structure will ensure that Europeans again endure persistent and high levels of unemployment and a continued deterioration in the quality and extent of public infrastructure and welfare provision. The collapse of this ideological nightmare cannot come quickly enough.

.

unemployment correlation

To set the scene, here are some unemployment rates – EU27, EU20, Norway (a European country whose currency is not pegged to the euro), the US and Japan – from January 2000 (birth of the common currency) to 3 January 2023.

Right away, you can see the problem.

Unemployment in Europe has been much higher than in other countries since the adoption of the euro and the signing of the treaty in support of the euro by the other seven EU countries.

Even when the U.S. went through cyclical recessions—the 2008 global financial crisis and the pandemic—its unemployment rate quickly returned to trend levels.

Consider the global financial crisis.

Unemployment rates rose sharply to around 10% in both Europe and the US.

The U.S. government introduced fiscal stimulus to end the crisis.

In the first quarter of the global financial crisis, European member states also provided fiscal stimulus, which saw unemployment peak in early 2011 and start to fall again.

Enter the European Commission and its excessive deficit regime, once austerity was imposed on member states, the recovery stalled, reversed, and unemployment rose for another 3 years.

About 10 years later, interest rates are only slightly below where they were before the global financial crisis.

Japan clearly stands out.

It enforces zero interest rates through monetary policy through a large-scale public bond-buying program, a yield-curve control program (to ensure that government bond yields remain below 0.25%), and does not impose restrictive fiscal rules on its policy settings.

You see the results.

Another point to consider – if unemployment in Europe is now lower than it was before the GFC, how do we explain that?

Well, for two reasons:

1. In my view, the ECB has been violating the spirit of the treaty, ignoring the no-bailout clause, and effectively funding government deficits through a massive bond-buying program.

This has taken members’ fiscal policy out of the influence of private bond markets and allowed fiscal deficits to rise (albeit somewhat).

2. The suspension of the Stability and Growth Pact at the start of the pandemic meant that member states were likely to run larger than usual fiscal deficits and support their domestic economies more fully.

Even with the ECB backing liberal rule, most member states have not taken full advantage of the easing, partly because they may fear it will be more difficult to adjust back to austerity once the European Commission restores excess deficit mechanisms under fiscal rules.

Overall, unemployment, while still too high, has fallen to its lowest level since the introduction of the common currency at the turn of the century.

It just goes to show.

The current financial position of the European Monetary Union

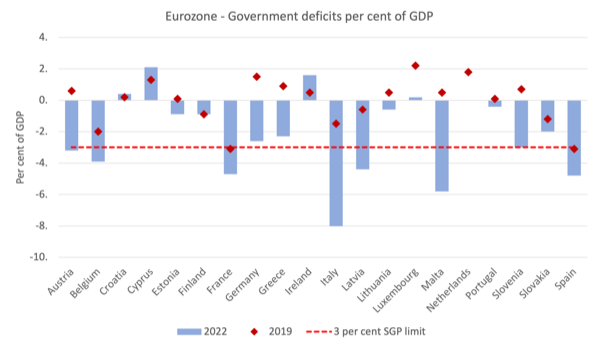

The chart below shows the current state of fiscal balances (% of GDP) of the euro area member states in 2019 and 2022.

The red diamond markers depict the pre-pandemic situation, while the blue bars depict the Eurostat results for 2022.

The red horizontal line is the Stability and Growth Pact’s 3% allowable ceiling on the fiscal deficit.

We do not yet have data for 2023 from Eurostat.

In 2019, after a long period of austerity following the global financial crisis, 2 member states were still in breach of the Stability and Growth Pact (France and Spain).

Seven member states are now in non-compliance by the end of 2022 following the introduction of fiscal policies in response to the pandemic.

I think that number will increase as we get more data for the first few months of 2023 and as GDP growth continues to slow.

For countries like France, Italy, Malta and Spain, any idea of getting back to the 3% threshold as quickly as possible, especially with a recession looming (ECB rate hikes and reduced public bond purchases), would be disastrous for the welfare of their citizens.

The French have risen.

That festers and spreads.

What is the public debt situation?

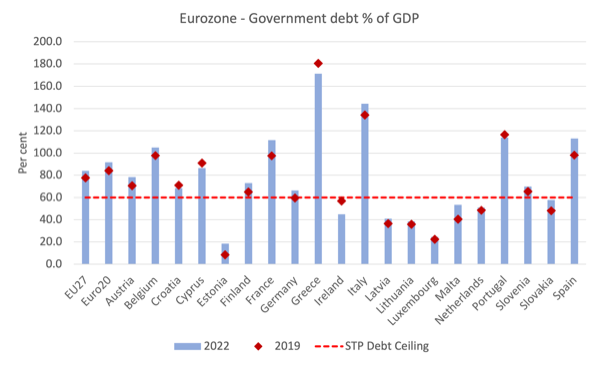

The chart below shows the current state of public debt (% of GDP) in the euro area and EU-27 in 2019 and 2022.

The red diamond markers depict the pre-pandemic situation, while the blue bars depict the Eurostat results for 2022.

The red horizontal line is the 60% limit allowed by the Stability and Growth Pact.

Before the pandemic, 11 of the 20 EMU member states were in breach of fiscal rules and four came close.

This number increases to 12 by the end of 2022.

Public debt ratios rose in 16 of 20 member states between 2019 and 2022.

Of the countries (11) already in non-compliance in 2019, public debt ratios increased in eight of them between 2019 and 2022.

Several countries (7) have debt ratios above 80%, while six countries have debt ratios above 100%.

In other words, it is almost impossible to restore fiscal discipline without broad and prolonged austerity.

It is doubtful that the social structures of these countries allow for such adjustments.

Unlikely, is my assessment.

oppression is about to return

As I mentioned above, unemployment (albeit still high) is at levels never seen in the history of the common currency, partly due to the loosening of fiscal rules, which has given countries more latitude.

Sixteen of the 20 member states widened their fiscal deficits between 2019 and 2020, although they could have widened more given unemployment remains fairly high.

A rather crude statistical analysis suggests that the fastest-expanding countries have seen the largest declines in official unemployment.

I’ll post it in due course when I have more time to conduct a deeper analysis with proper endogeneity controls.

So, with all of this in mind, why would the European Commission seek to reiterate fiscal rules that are sure to lead to higher unemployment and higher poverty rates?

Because that’s what they announced on April 26, 2023 in the statement cited in the introduction.

They claim the new “legislative proposals” will be “the most comprehensive reform of the EU’s economic governance rules since the economic and financial crisis”.

The usual narrative was used as the justification – “strengthening the sustainability of public debt and promoting sustainable and inclusive growth.”

The European Commission is good at using language that sounds like it benefits more people, when in fact the opposite is true.

The committee claims:

These proposals address shortcomings in the current framework. They take into account the need to reduce significantly increased public debt levels, draw lessons from EU policy responses to the COVID-19 crisis, and prepare the EU for future challenges by supporting progress towards green, digital, inclusive and resilient Prepare the economy and make the EU more competitive.

Then we cut to the chase:

The National Medium-Term Fiscal Structure Plan is the cornerstone of the Commission’s proposal.

In other words, member states’ fiscal policy proposals must be guided by the committee.

They will have to “integrate…fiscal, reform” goals and be subject to annual committee oversight.

So expect to see more benefit cuts, privatizations, outsourcing, pension cuts, wage limits – all under the banner of “reform”.

Reform sounds like progress.

Outside the EU, this means a malicious attack on the welfare of the working class.

More specifically, this so-called “state ownership” of increased fiscal trajectories must be undertaken within the scope of the restoration fiscal rules set by the Commission.

The committee noted:

For each member state with a government deficit of more than 3% of GDP or a public debt of more than 60% of GDP, the committee will publish a country-specific “technology trajectory”…

For member states with government deficits below 3% of GDP and public debt below 60% of GDP, the committee will provide technical information to member states to ensure that government deficits also remain below the reference value of 3% of GDP in the medium term.

In other words, if a member state breaches a Stability and Growth Pact threshold, the Commission will implement (the so-called “technical trajectory”) austerity policies to move that member state towards the threshold.

How much time does a country have?

Well, not much:

The public debt-to-GDP ratio must be lower at the end of the period covered by the plan than it was at the beginning of the period; as long as the deficit remains above 3 percent of GDP, a minimum fiscal adjustment of 0.5 percent of GDP per annum must be made.

And the adjustment must be immediate (“cannot be postponed until a foreign year”).

Take Italy, which currently has a fiscal deficit of 8% of GDP, as an example.

It must shrink its fiscal settings by at least 0.5% of GDP.

I did some calculations using the latest figures from Eurostat, which show that while real GDP rose in the last quarter of 2022, a 0.5% reduction in net spending as part of an austerity package would immediately push the economy into recession.

in conclusion

I will be doing more work on the concept of “technological trajectories”.

But that’s just another fancy term for austerity.

Types of prolonged high unemployment after the global financial crisis.

We learn from this that while people may think that lower unemployment is a good thing for them—they have an income, can manage risk, etc.—this is not the case for technocrats in Brussels.

They are running an ideological campaign to reassert their authority, and they are well aware that hundreds of thousands of Europeans will lose their jobs due to the imposition of these “technical trajectories”.

But their purpose will eventually be achieved.

At least until social instability causes the whole rotten system to collapse.

That’s not fast enough.

Enough for today!

(c) Copyright 2023 William Mitchell. all rights reserved.

{kind=link}