We are still determining the content of the BBB bill, but it is similar to the content currently discussed. It is combined with the Infrastructure Investment and Employment Act (IIJA) and is unlikely to cause too much pressure on the credit market and prices The upward pressure is because it is largely paid.Here (while we wait for the CBO) is Moody’s analysis forecast (As of 11/4).

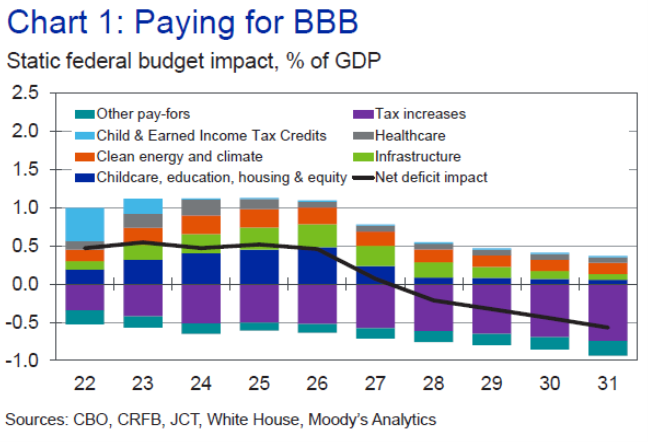

First, the net impact of BBB alone on the budget deficit.

source: Zandi (November 2021).

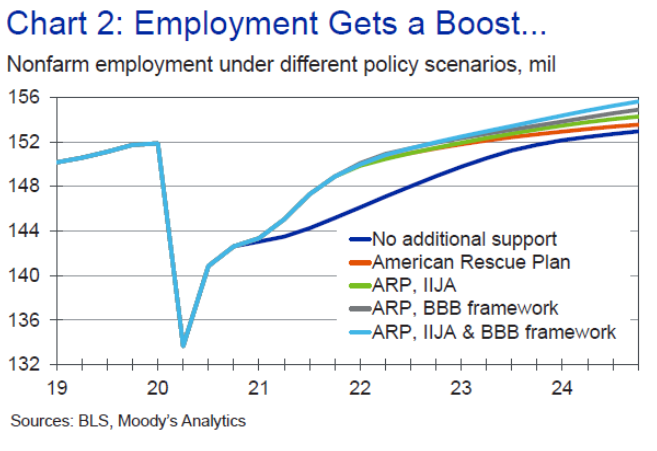

Next, the impact on the number of non-agricultural employment in the baseline, and certain combinations (the American Rescue Plan (ARP) has been passed, so it can be regarded as a benchmark for comparing ARP+IIJA, ARP+BBB and ARP) +IIJA+BBB .

source: Zandi (November 2021).

If only IIJA is implemented, the employment rate by the end of 2023 will only be slightly higher (relative to ARP). Obviously, with the passing of the BBB and IIJA, the employment rate will increase significantly.

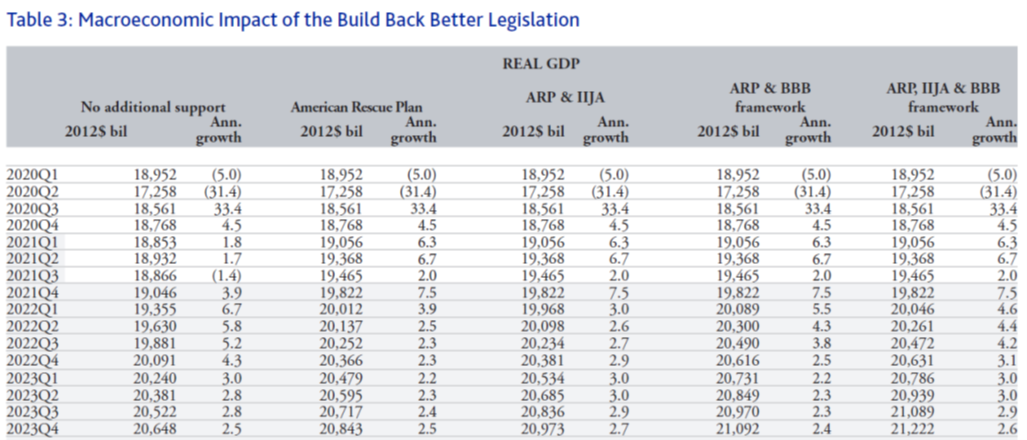

What about GDP and components?Table 3 Zandi (November 2021) The impact is outlined. I have extracted the GDP impact as of the fourth quarter of 2023.

source: Zandi (November 2021).

As of the fourth quarter of 2023, with the implementation of IIJA and BBB, actual GDP will be about 1.8% higher than the forecast of ARP alone.

Obviously, one must believe in the assumptions used to regulate the model (rest of the world, monetary policy, the evolution of Covid-19, etc.) and the model itself.

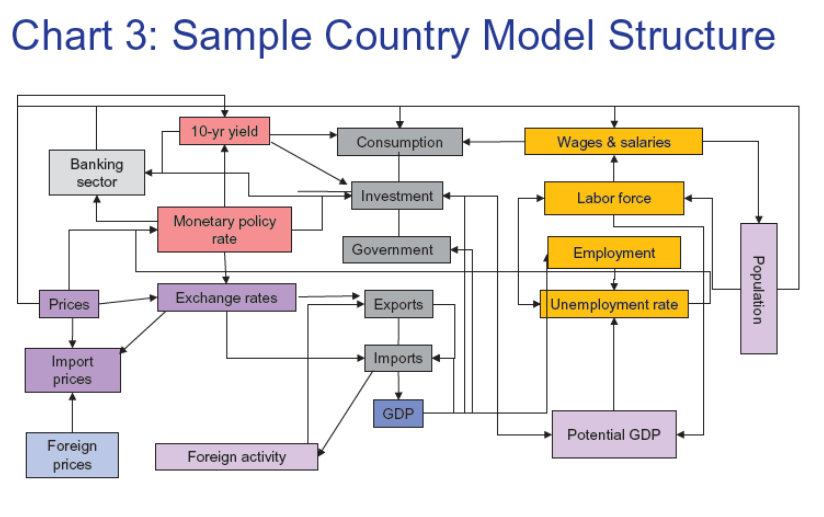

Moody’s analysis of the global macroeconomic model appears to be a large-scale multi-equation (thousands) macroeconomic econometric model in which the functional equation has been estimated (rather than calibrated).The summary of the model description is hereThe diagram in the description is as follows:

source: Hopkins (2018).

For a discussion of the differences between macroeconomic econometric models, dynamic stochastic general equilibrium models and VARS, please refer to this (2009) postalPlease note that some models fall between two categories; for example, Federal Reserve FRB/United States The model contains some calibrated parameters, but there are many estimation equations, and the Fed’s SIGMA and EDO models are DSGE.

For congressional debates, the official arbiter of budget deficit and economic output impact is the Congressional Budget Office (for budget deficit/income/expenditure impact, CBO and Joint Taxation Commission, JCT). The prediction model of CBO is described in Arnold (2018). This is why CBO is working overtime now.

{kind=link}

{kind=link}