Co-authors present papers Laurent Ferrara and myself today International Symposium on Forecasting 2023…

Show a picture (details):

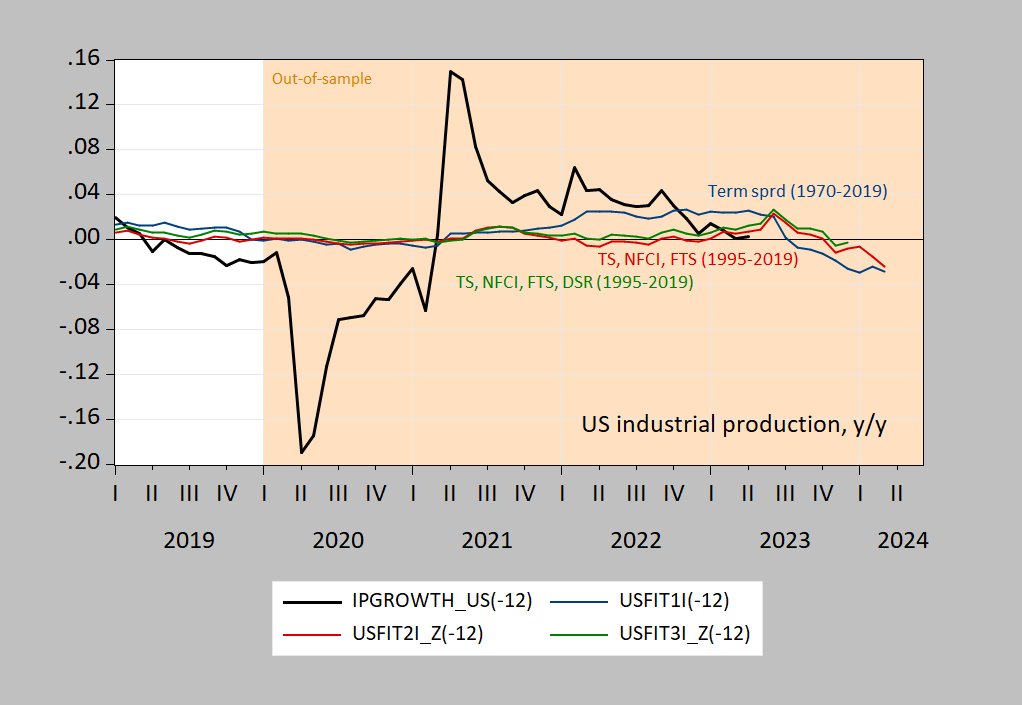

figure 1: Reported year-over-year industrial production (black), out-of-sample post-simulation of term spreads/short rates (blue), Chicago Fed NFCI and foreign term spread-enhanced specs (red), and specs but increased debt-service ratios (only until the end of 2022) (green).

Figure 1 differs slightly from the information reported in the paper, as I replaced the Aroggoni, Bobasu, Venditti equal-weighted FCI with the Chicago Fed NFCI available last month (Arrigoni et al.’s series is only available for 2020M05).

Recession forecast (recession is defined by NBER) here (in-sample fit).

The slides follow (and the paper to follow up later – post a comment).

{kind=link}

{kind=link}