Yesterday (February 6, 2024), the Reserve Bank of Australia (RBA) issued the so-called- Monetary Policy Statement – February 2024 – This is a quarterly statement that “sets out the RBA’s assessment of current economic and financial conditions and the outlook that the RBA Board considers when making interest rate decisions”. At the same time, the Reserve Bank of Australia also made the latest decision to keep the policy target interest rate unchanged at 4.25. However, the governor told the media that despite the rapid decline in inflation and strong signs that the economy is slowing rapidly, they did not rule out the possibility of further interest rate hikes. Just yesterday, ABS released the latest news— Australian retail industry – In December 2023, trade volume fell by 1.4% compared to the previous year. Volume increased 9.8% in Q9 2022 (a pandemic overshoot as restrictions eased). By the 12th quarter of 2023, sales growth was negative 1%, which was the third consecutive quarter of negative sales growth. It would be outrageous if the RBA considered raising interest rates further. But it has become a rogue organization, and its rhetoric shows how outrageous its reasoning has become.

On June 20, 2023, the incoming Governor of the Federal Reserve Bank of Australia delivered a speech— Achieving full employment – Newcastle – She outlines how the mainstream concept of non-accelerating inflationary unemployment (NAIRU) affects the RBA’s monetary policy decisions.

She claimed that with the official unemployment rate holding steady at around 3.5% or 3.6%, the Reserve Bank of Australia believes Australia's NAIRU is 4.5%.

She also said that this meant that the Reserve Bank of Australia must continue to raise interest rates and force the unemployment rate to rise to 4.5% (when the number of unemployed people exceeded 150,000) to stabilize inflation.

Inflation was about to peak and would soon fall sharply.

I pointed out at the time that NAIRU was unlikely to reach 4.5% if the unemployment rate stabilized around 3.5% and inflation declined.

I analyze that speech in this article – Mainstream logic should conclude that Australia's unemployment rate is higher than the NAIRU, not lower than the NAIRU as the Reserve Bank of Australia claims. (July 24, 2023).

Shortly after, the Reserve Bank of Australia lowered its NAIRU forecast to 4.25%, but the official unemployment rate is still well below 4%.

At this time, the inflation rate is continuing to decline, which makes the RBA's logic and reasons for raising interest rates ridiculed.

The quarterly Monetary Policy Statement (cited in the introduction) is even more illustrative of how lost the RBA has become – indulging in arrogant assertions of mainstream theoretical concepts and then abandoning them when the data defy “theory”.

inside – press conference – Explaining the monetary policy decision yesterday (February 6, 2024), the Governor admitted that the Reserve Bank of Australia does not know what full employment is (from 42 minutes).

She referred the news media to Chapter 4 of the statement, which provides a detailed discussion – “In-depth – Full Employment.”

They now claim NAIRU's previous statements cannot be taken seriously:

Given these constraints, the RBA does not set a fixed level of full employment.

Of course, the RBA Act 1959 requires the RBA to pursue full employment.

Therefore, they “maintain a set of models that provide a range of estimates of spare capacity in the labor market” – which is just a “general statement” of the NAIRU estimates.

They write:

These models use historical relationships and economic theory to estimate labor market outcomes consistent with full employment. These models primarily estimate unemployment or underutilization and do not put upward or downward pressure on inflation or labor cost growth.

In other words, NAIRU.

They acknowledged that “considerable uncertainty exists” in their model and estimates “around the center estimate.”

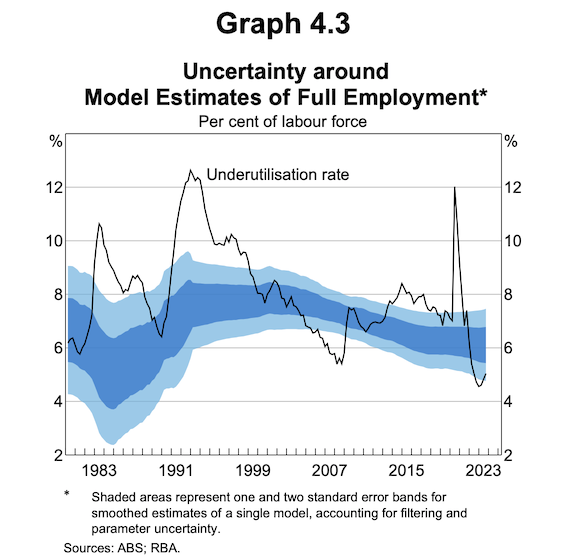

Here is the graph (4.3) they provided to demonstrate their model estimates.

The solid line is the actual rate of labor underutilization adjusted for hours worked, taking into account official unemployment and underemployment (adjusted for the amount of overtime workers are willing to work).

I actually think their estimates of labor utilization are severely biased downwards.

For example, in May 2023 (when detailed hours worked are available), there were 1,594,400 underemployed workers.

The ABS reports that about 45% of workers want to work full-time, and on average, all underemployed workers want to work 11 more hours a week.

In the same month, there were 520,000 unemployed workers, 350,000 of whom wanted to work full-time.

A rough calculation shows that this wasted but usable labor accounts for about 7% of the labor force.

The Reserve Bank of Australia estimated at the time that “labor underutilization” was about 5%.

Bias downward.

The blue shaded area contains the confidence interval for the NAIRU estimate, with the point estimate in the middle of the dark blue or inner shaded area.

What do these straps mean?

The widest range is the 95% confidence interval, which means you are equally sure that the true rate lies between the upper and lower bounds, with an error change of 5%.

Therefore, in the current period, the RBA's estimate of full employment is likely to be 7.5%, with a labor underutilization rate of 5%.

They were equally “sure” about both.

This means that for policy-making purposes, this approach makes no sense.

Why?

Because if the economy is operating above “full employment,” then any inflationary pressure will be a sign of excess demand.

But how will they decide?

What if the actual underutilization rate is 7% (well above the lower end of its estimated range)?

Should policy be tightened (ignoring whether tightening monetary policy is effective)?

They concluded no.

But if they use the cap, their answer is yes.

Therefore, this exercise provides no real guidance at all and is largely smoke and mirrors.

This problem would have been more pronounced in the 1980s, when their margins of error were much wider—for example, they were unable to identify the full employment rate around 1984, which was around 2.3% or closer to 8%.

The statement said:

Given the large uncertainty involved in the estimates of each model, labor market conditions may already be consistent with full employment, but the chance is relatively small.

The Governor said at the press conference that although she claimed last year that the unemployment rate must rise to 4.5% to stabilize inflation, the current unemployment rate of 3.9% is no longer considered a problem.

The point is that the RBA is now a rogue organization that previously pretended to make decisions based on economic concepts such as NAIRU, but now admits it no longer has any accuracy to those concepts after the facts exposed that logic.

However, according to its own forecasts, inflation will enter the target range (2-3%) by December 2025, and the official unemployment rate is expected to be 4.4%.

If the RBA's forecast is correct, an additional 130,000 jobs will be lost (relative to December 2023).

But the point here is that this must also be their NAIRU forecast because, according to their logic, full employment is defined as an unemployment rate consistent with stable inflation.

These 130,000 job opportunities are for real people.

The smug governor can laugh at press conferences (if you watch them) and pretend to be thoughtful and analytical, but the RBA is taking a policy approach that will address at least 130,000 job losses, Because they admitted to the media yesterday that they really don't know what the unemployment rate is consistent with full employment.

In my opinion, this is a shame.

in conclusion

The Reserve Bank of Australia also admitted that as a result of rising interest rates, the proportion of debt holders currently paying interest has increased significantly, which is unsustainable by any measure for an increasing number of citizens.

The Reserve Bank of Australia is still unclear about the lagging impact of its previous interest rate decision, but threatened to take more measures.

When you think about it, the ABS's most recent (monthly) inflation estimate suggests that the annual rate has fallen to 3.4% (and that's a steep decline), it seems extremely disingenuous to further threaten people with more rate hikes.

Especially when their statements show that the RBA has no coherent logic that stands up to empirical testing.

As I said before, the governor's salary should be tied to the unemployment rate and then I guess the threat would be reduced.

That's enough for today!

(c) Copyright 2024 William Mitchell. all rights reserved.

{kind=link}

{kind=link}