February 11, 2024

Here's a screenshot from my journal showing all the trades I've made since Last trading post of the week (CAS is The calm after the storm & PB abbreviation Non-ADX 1,2,3,4 callback):

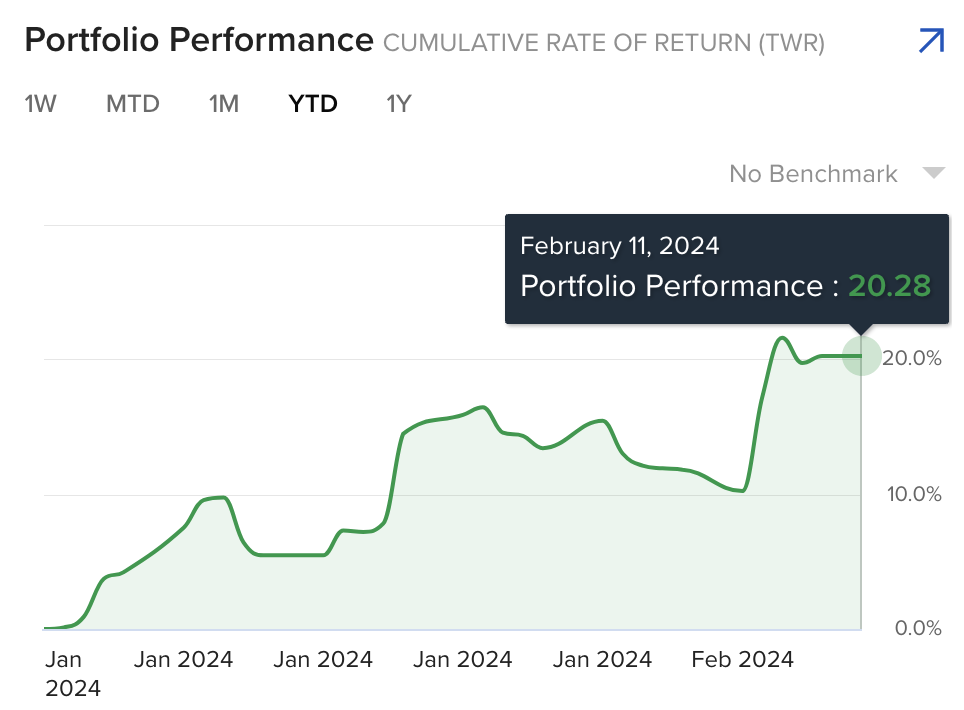

I highlighted two big winners, SMCI and IMNM… both of which I based on non-ADX 1, 2, 3, and 4 pullback signals. Another thing I pointed out was 4 consecutive 1R+ losing trades. (They are not exactly Continuous… The logs are sorted by entry time, but exit times are not consecutive. You can see the impact of the period between SMCI and IMNM in my stock curve – my year-to-date returns slipped from 16.5% to 10.2% before IMNM helped push it above 20%:

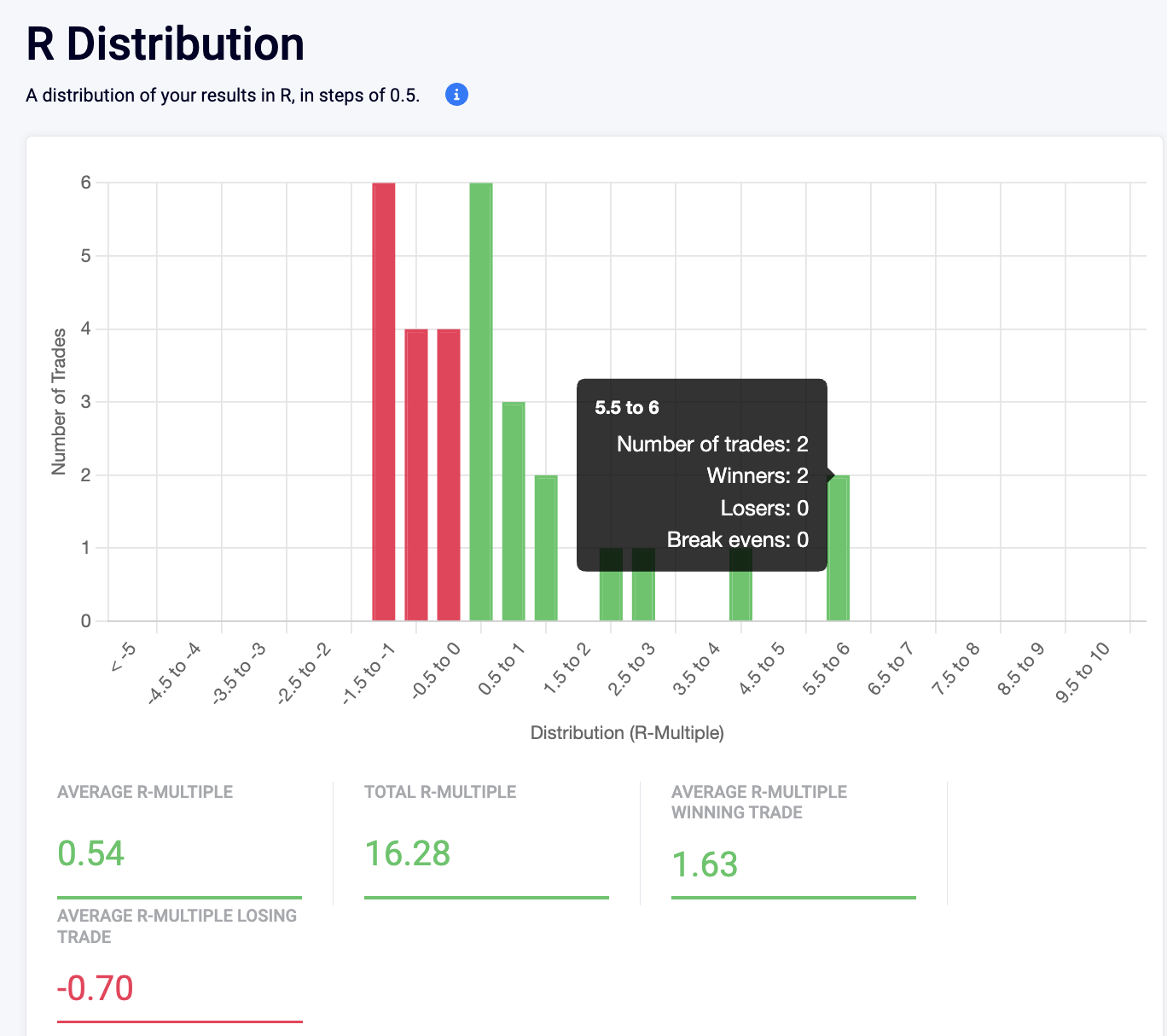

One comparison I'm excited to make with 2023 is my R distribution. I have no trades in 2023 with returns higher than 4.5R, and I already have 2 trades in 2024. Losses must be kept small to allow for easy recovery.

An interesting comparison to 2023 is which settings work for me. Non-ADX 1, 2, 3, 4 moved up to #1 and the “Best Setting Average” is now the “MA Bounce”. To my surprise, “The Calm After the Storm” dropped from first place to last place! I'm 0 for 3 on CAS trades so far, but it's still early in the year and the sample size is small. I can't wait to do this comparison again in a few months.

One of my takeaways from looking back at 2023 is:

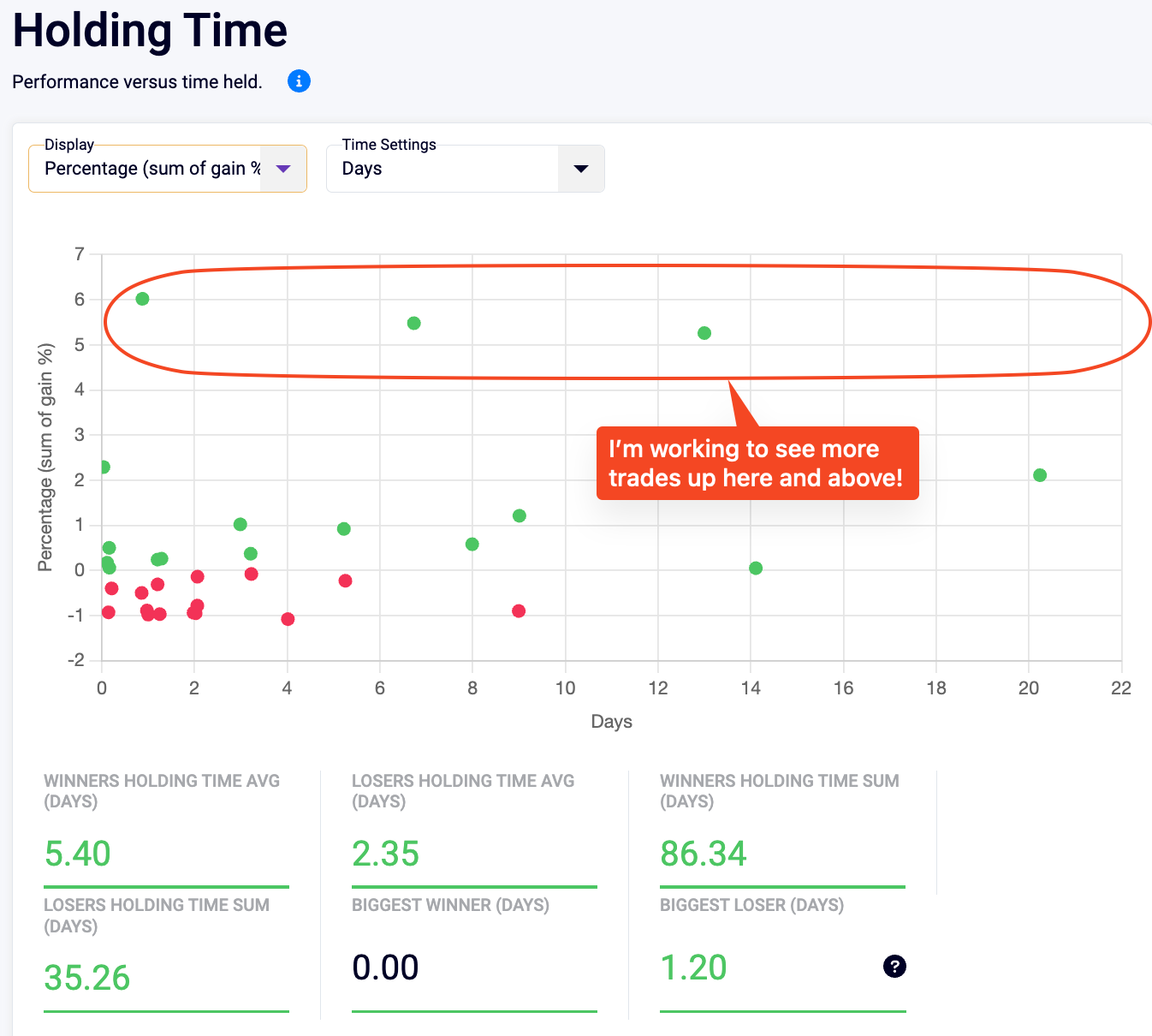

I want to see bigger “biggest winners” so I need to work on holding longer.

So far, the distribution is roughly the same as in 2023. My “Average Winner Hold Time” actually dropped by a day. This hold time issue has been bothering me for the past few weeks due to my SMCI trades.

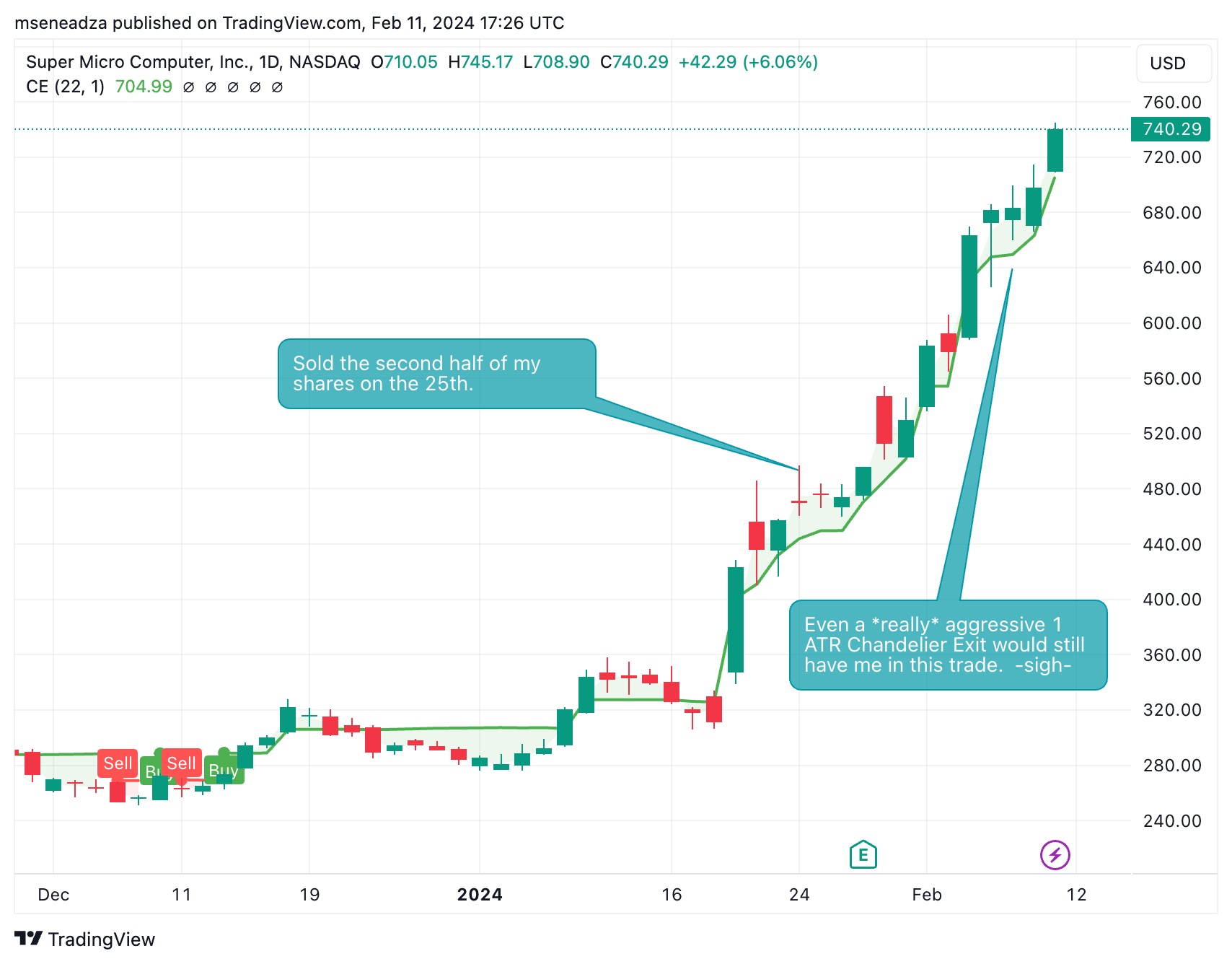

If I had just exited using a simple chandelier exit, I would still have continued trading and my account earnings would have increased by 14.4% instead of the 5.5% locked in. It was an expensive lesson, but one I won't soon forget. I would definitely use some kind of trailing stop on a future mover like this.