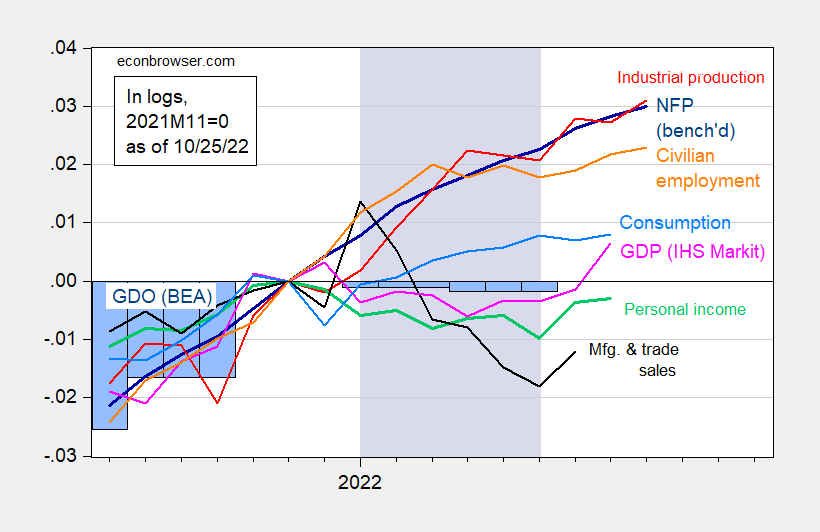

Monthly indicators followed by the NBER Business Cycle Measurement Committee, plus GDP and GDO, and IHS-Markit (nee Macroeconomic Advisers) monthly GDP:

figure 1: Nonfarm payrolls (dark blue), Bloomberg’s nonfarm payrolls (blue+), civilian employment (orange), industrial production (red), excluding 2012 transfers of personal income (green) as of October 25 , Manufacturing and Trade Consensus Sales in 2012 Dollars (black), Consumption in 2012 Dollars (light blue), Monthly GDP in 2012 Dollars (pink), Official GDP (blue bars), all logarithms Normalized to 2021M11=0. The lilac shading indicates dates associated with the H1 hypothetical recession. Source: BLS, Federal Reserve, BEA, via FRED, IHS Markit (nee Macroeconomic Advisers) (published October 4, 2022), and author’s calculations.

figure 2: As implied by preliminary benchmark revisions (dark blue), civilian employment (orange), industrial production (red), personal income excluding transfers in 2012 dollars (green), manufacturing and trade sales in 2012 dollars (black) nonfarm payrolls), consumption in 2012 dollars (light blue) and monthly GDP in 2012 dollars (pink), official GDO (blue bars), all logs normalized to 2021M11=0. The lilac shading indicates dates associated with the H1 hypothetical recession. Source: BLS, Federal Reserve, BEA, via FRED, IHS Markit (nee Macroeconomic Advisers) (published October 4, 2022), and author’s calculations.

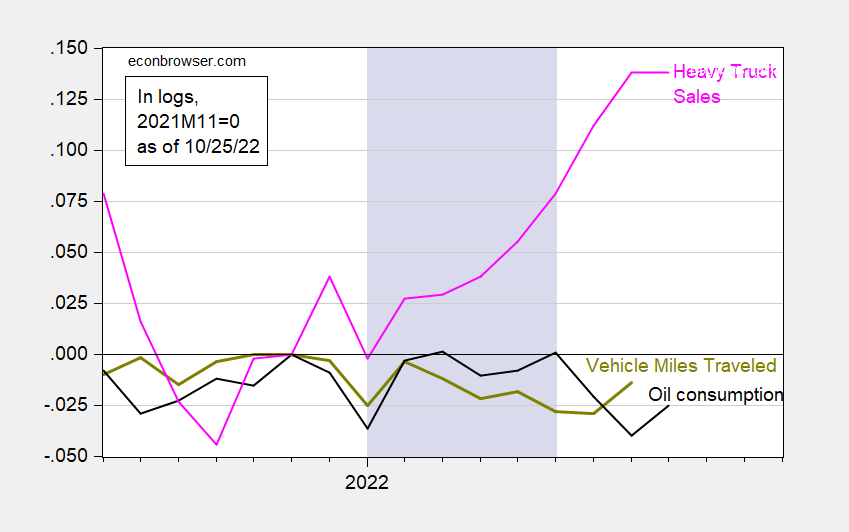

It’s interesting to recall what led to the recession in the first half of 2022. For some, this is a negative reading of GDP.For others, it’s vehicle miles driven, or fuel consumption (both from Steven Kopitz).Here are the two metrics (concurrent or lagging I think) and heavy truck sales (by Calculate risk).

image 3: Vehicle miles driven, seasonally adjusted (yellow-green), oil consumption in millions of barrels per day (black) and heavy-duty truck annual sales in millions (pink), all log normalized to 2021M11=0. The lilac shading indicates dates associated with the H1 hypothetical recession. Source: BTS, EIA, Via FRED Bank of East Asiaand the authors’ calculations.

as i am in this postal, vehicle mileage, regardless of the transition, is a very poor metric and certainly outperforms heavy-duty truck sales. So the flat trajectory of VMT and oil consumption seems interesting, but not conclusive to me. The rise in heavy-duty truck sales appears to refute the argument for a recession in the first half of the year.

What about the GDP series? First, note that the NBER BCDC does not place a major weight on GDP. Second, the decline in GDO is much smaller than that of GDP.Third, GDP is constantly revised over time; therefore, the contours of GDP may look quite different in a few years, and many like the recession of 2001 (This ultimately doesn’t meet the “two consecutive quarters” rule of thumb).

Looking ahead, the Bloomberg consensus as of today is 2.4%, GDPNow is 2.9% (10/19) and the St. Louis Fed “News” index is 1.3% (10/21).

{kind=link}

{kind=link}