It’s Wednesday, and as usual, as a pioneer of the music section, I’ve considered some topics that go deeper than a blog post. Inflation data from the U.S. Bureau of Labor Statistics released yesterday (June 13, 2023) – Consumer Price Index Summary – May 2023 – Suggesting a further notable decline in inflation, as some key supply-side drivers continue to weaken. All the data point to the fact that the Fed’s logic is deeply flawed and unfit for purpose. Today, I also discuss the imminent start of follies again in Europe, as the European Commission begins to flex its muscles after announcing to member states that it will return to austerity by the end of the year. Finally, some beauties from Europe in the music field.

US inflation

The BLS released its latest monthly CPI yesterday, showing May 2023 (seasonally adjusted):

- The All Items CPI rose 0.1% for the month (down from 0.4% in April) and 4.1% for the year (down from 5% in April and 6.4% in January).

- The peak monthly gain in June 2022 is 1.2%.

The U.S. Bureau of Labor Statistics states:

The housing index was the largest contributor to the monthly increase across all items, followed by gains in the used car and truck index. The food index rose 0.2% in May after remaining unchanged in the previous two months…In contrast, the energy index fell 3.6% in May as the main energy component index fell…

The All Items Index rose 4.0% in the 12 months to May; this was the smallest 12-month gain since the end of March 2021.

The chart below shows the importance of energy prices to the overall US inflation rate.

A simple regression line (dashed line) produces an R2 0.48. This means that about 48% of the change in the headline CPI was driven by changes in energy prices.

It’s a bit more complicated than statistical terms, but the rough figure is a good guide to the influence of energy prices.

In fact, the sharp drop in U.S. inflation has been attributed to sharp drops in energy and gasoline prices.

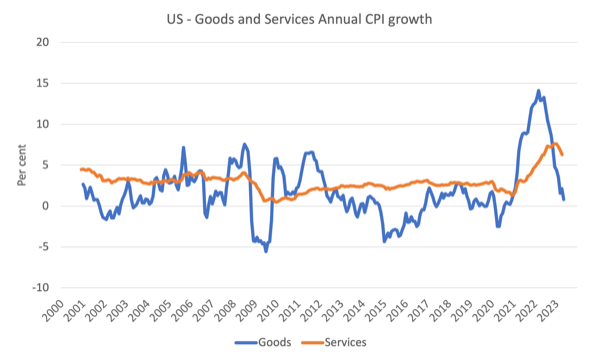

The chart below shows the change in annual price increases from 2000 to May 2023 for the goods and services industries.

The argument has been that inflation is largely driven and instigated by supply factors that limit the economy’s ability to meet demand for goods – Covid factories and transport disruptions, among others.

The graph clearly shows that these factors have been fading since the second half of 2022 as supply chain constraints ease.

As a derivative of the supply driver, the services sector has lagged behind the commodity sector and while still recording higher inflation than the commodity sector, it now appears to have peaked and is also declining.

Inflation has been falling sharply amid a fairly stable U.S. labor market.

In this blog post I analyze the latest Bureau of Labor Statistics employment release – The U.S. Labor Market—Maybe at an Inflection Point With Rising Unemployment (June 5, 2023).

While job growth has slowed slightly, there are no signs of a serious recession-style slowdown.

Crucially, the lack of correspondence between labor market dynamics and inflation dynamics suggests an anemic logic for the Fed to justify its rate hikes.

The logic of the Fed is all about the strength of the labor market (they think the real unemployment rate is below NAIRU), which drives them keen to create more unemployment and kill wage growth, which in turn keeps inflation at bay. .

We also know that household consumption spending is not going to fall anytime soon.

Therefore, these data are not friendly to the logic of the Fed.

The employment data also suggests that real wage cuts are continuing (while slowing down), which does take wages out of the equation when assessing the current CPI dynamics.

Inflation has come down fairly quickly because the main driver, which is not particularly sensitive to interest rates, is falling.

One rule for some (most) and another for others (few)

For some time now, I’ve been analyzing comments provided by RBA Governor Philip Lowe on how he justified Australia’s ridiculously excessive rate hikes.

He dodges and dives as one storyline doesn’t match reality, but a fairly constant narrative is that unless workers actually cut wages, the RBA will raise rates more than it is doing now because wage growth will threaten the inflation target.

Sometimes he puts this in the context of real wage growth – which is his productivity storyline, in which he rightly points out that any country needs such growth to raise real living standards.

But recently he has used the productivity line to claim that without productivity growth, real wages must fall – a subtle shift.

The shift is from productivity growth providing the non-inflationary space for nominal wages to grow faster than inflation to nominal wages requiring productivity growth to grow as fast as inflation.

The former argument is correct, the latter except that the RBA Governor believes that business is reasonable in times of inflation Increase their profit margins.

The Premier has been claiming wage growth will hurt the fight against inflation, even claiming last week that rising wages given to minimum wage workers was a factor in the RBA’s decision to raise interest rates further given the latest increase in the minimum wage.

Well, I wonder when he will comment on the latest data on executive compensation.

Today (June 14, 2023), – Australian Institute of Governancereleased their latest report – 2023 Board and Executive Compensation Report.

The Governance Institute, formerly the Australian Institute of Chartered Secretaries, focuses on “promoting good practice in governance and risk management”, which includes monitoring CEO pay.

While workers’ wages are currently being severely slashed in terms of real purchasing power, and the RBA governor wants tougher wage outcomes – or he’ll swing his stick further – the bosses are throwing a party.

The Governance Institute report surveyed the boards of directors of many companies, nonprofits, and public organizations.

It found:

1. “Over the past 12 months, ASX 200 companies have seen significant pay increases, with 42% of ASX board directors and 71% of ASX senior managers receiving a pay increase.”

2. “Company secretary remuneration was one of the growth areas, with an average pay increase of 11%. Specifically, for ASX 200 companies, the increase was higher at 13%, while for company secretaries of large listed companies, That’s a 24% increase.”

3. “Risk managers also saw their average compensation increase by 15% last year.”

4. “Higher bonuses (potentially the highest bonuses available) are also offered to these professions, with risk managers from ASX 200 companies able to receive bonuses of up to 45% of their fixed salaries. Likewise, general counsel and company secretaries overall average That’s a 49% increase.”

Try to rationalize the RBA governor’s insistence that workers must tighten their belts and take real pay cuts.

And try to rationalize this based on demands from large employer groups and companies that the Fair Work Commission increase the minimum wage by more than 3% in nominal terms, which of course represents a substantial cut in real wages.

Impossible to rationalize.

For some (most of us) it’s one law, for others (top of town) it’s another law.

A media commentary (from a usually business-biased newspaper) wrote today (source):

…Boards of tone-deaf companies that award these base salary increases to senior executives are risking a community backlash and possibly some pushback from shareholders.

Corporate generosity to executives is all the more objectionable at a time when companies have been pushing back against calls to pay workers more to match inflation. Working people are told to play by the rules and try to avoid a wage spiral that feeds and fuels inflation.

Research by the Institute for Governance shows that senior executives are already well paid enough to insulate them from the cost-of-living pressures felt by many wage earners, but they are being overcompensated by inflation.

We certainly live in obscene times.

I urge all readers to write to the Australian companies that pay their CEOs and other executives these lucrative incentives and tell them that you are organizing a widespread boycott of their products through social networking.

This disgusting act of generosity will continue until we are truly organized as consumers.

I’m doing more research on this issue to get a list of worst offenders.

Music – Ola Gjeilo

Here’s what I’ve been listening to this morning at work.

The first time I heard this album—— winter song – Long haul flight from Japan. The album was released in 2017 by Decca.

It comes from the Norwegian composer — Olajilo – He works with various string ensembles and choirs, creating very modern classical music.

On this track—The Rose II—he combines— 12 ensembles – with cellist Max Ruisi.

Very sophisticated way of looking at inflation data.

If chorus is your thing, Royal Holloway’s treatment of the song is a treat:

Enough for today!

(c) Copyright 2023 William Mitchell. all rights reserved.

{kind=link}