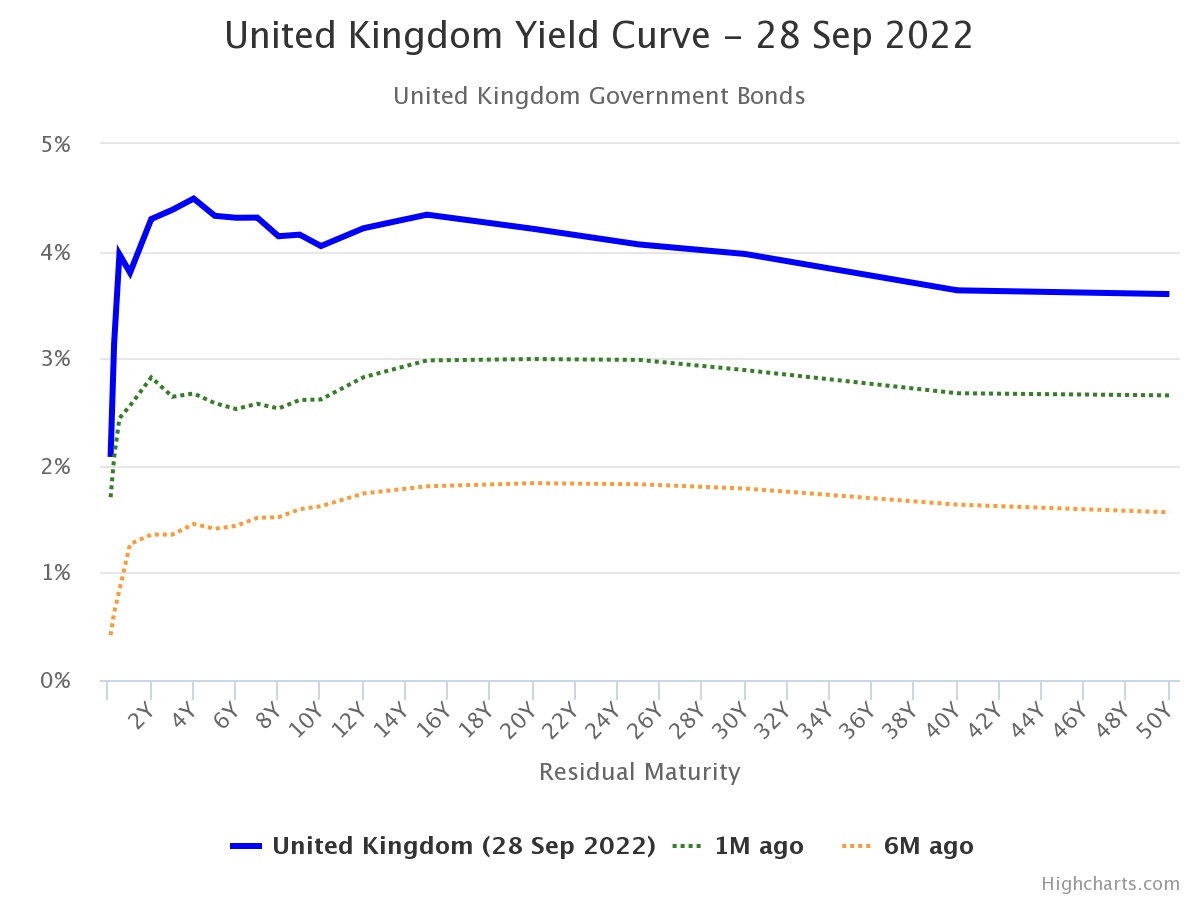

Recession coming? Or is it already here? Here’s a graph of the UK yield curve as of today, a month ago and 6 months ago:

resource: Worldofgovernmentbonds.comaccessed 28 September 2022.

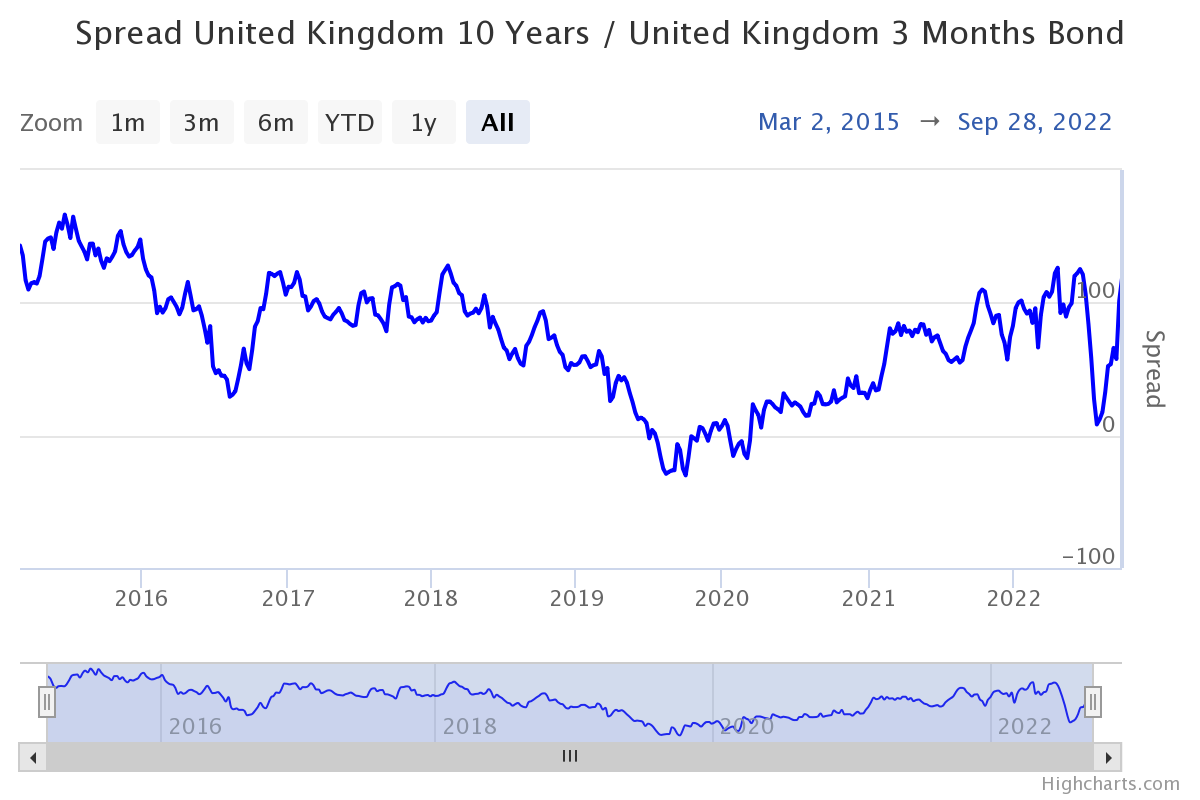

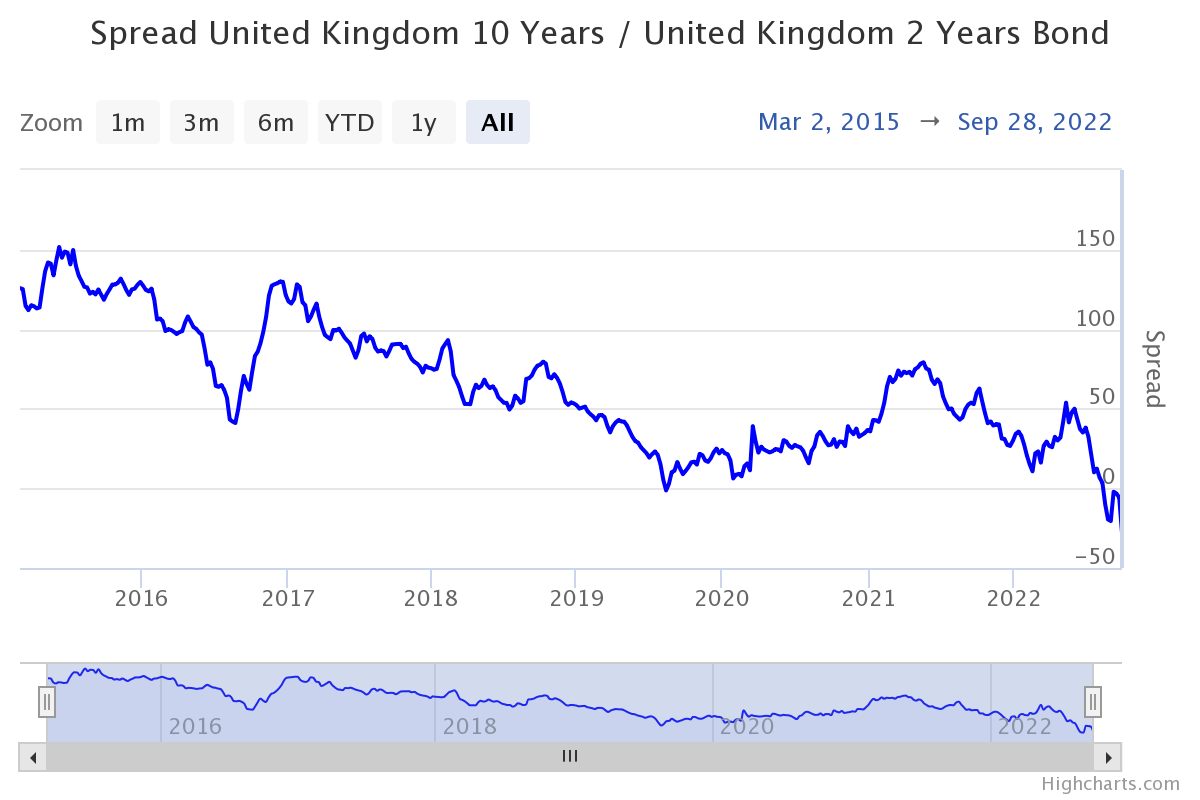

Below is a time series of two popular term spreads, 10-year to March and 10-year to 2 years:

resource: Worldofgovernmentbonds.comaccessed 28 September 2022.

resource: Worldofgovernmentbonds.comaccessed 28 September 2022.

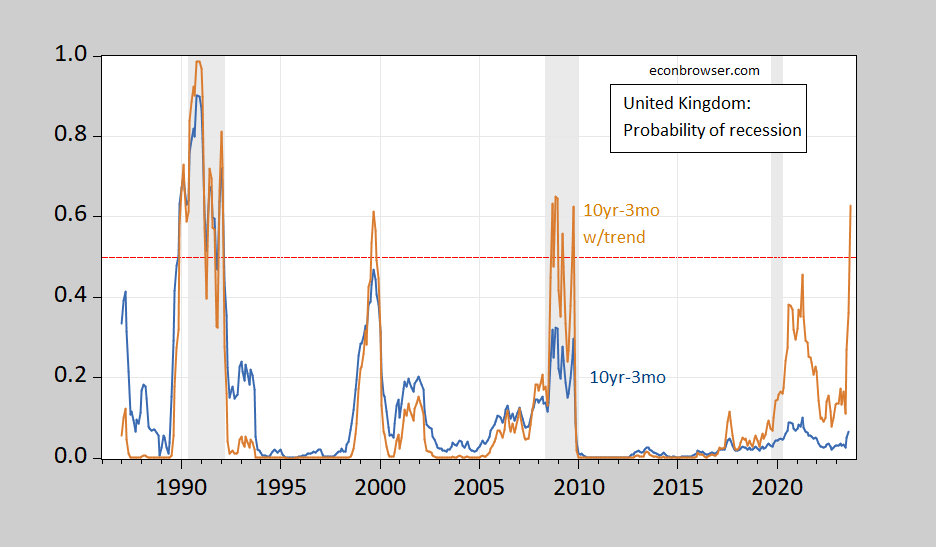

The 10yr-March and 10yr-2yr spreads were close to inverting in July – within basis points. For the UK, however, it is unclear what an inversion would mean for economic activity and/or a recession. Chin-Cuco (2015) No strong relationship was found for the UK. In an updated sample of 2022M08 (assuming no recession as of 2022M08), I found a statistically significant effect of the 10-year to 3-month term spread, McFadden R2 0.32. The blue line represents the recession probability implied by the normal probit model, using the 10yr-3mo (Interbank) spread without increasing.

figure 1: The probabilistic regression of recession indicators leads to a 12-month lead in recession probabilities compared to the 10-year to 3-month term difference (blue) and strengthens with a linear time trend (tan). The three-month rate is the interbank offered rate. ECRI defines the recession date from peak to trough, shaded in grey. Source: OECD calculations via FRED, invest.com, ECRI and authors.

Using this simple norm, the probability of a recession in 2020 is very low. However, the results are very sensitive to the inclusion of time trends (statistically significant coefficients). Time Trend Augmented Models with McFadden R2 0.44, which is more accurate in predicting a recession, although it incorrectly indicates the 1999/2000 recession (wrong in terms of ECRI).

Still, even the boosted regression implies a probability of only 12% in September 2022.In contrast, think tanks NIESR calls recession on Aug. 12based on changes in GDP.

{kind=link}

{kind=link}