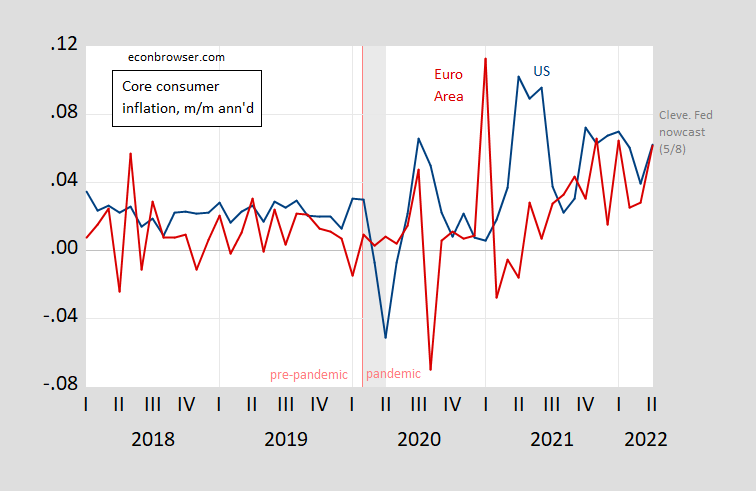

The April HICP data for the Eurozone has been released. The US will release April CPI on Wednesday.use Cleveland Fed nowcast For April core data (0.52% m/m, Bloomberg consensus 0.4%), we have the following picture.

figure 1: Month-on-month annualized core inflation in the United States (blue) and the euro area (red), calculated using log-differences. The authors seasonally adjusted core HICP for the euro area using geometric census X-12. April US core CPI uses a 5/8 Cleveland Fed nowcast. The NBER uses shades of grey to define the peak and trough dates of the recession. Source: BLS, Eurostat via FRED, Cleveland FedNBER, and the authors’ calculations.

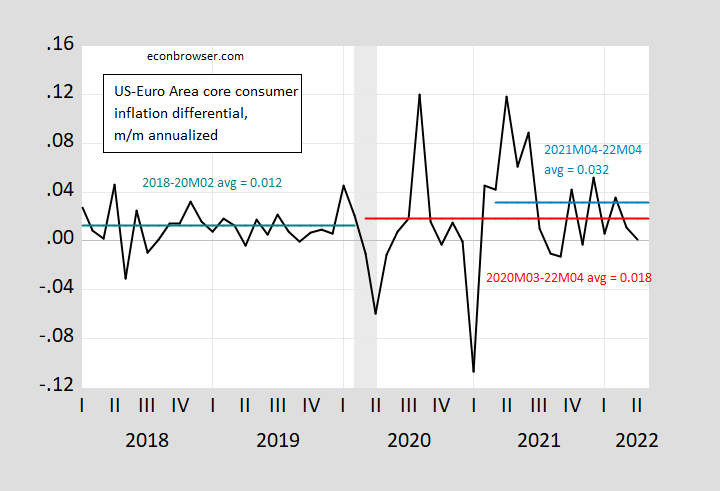

To get an idea of when core inflation in the US accelerated relative to the euro area, I show the difference below.

figure 2: Month-on-month annualized core inflation differentials (black) in the US minus the euro area, calculated using log differentials. The authors seasonally adjusted core HICP for the euro area using geometric census X-12. April US core CPI uses a 5/8 Cleveland Fed nowcast. The cyan line is the 2018-2020M02 average, the red line is the 2020M03-2022M04 average, and the light blue line is the 2021M04-2022M04 average. The NBER uses shades of grey to define the peak and trough dates of the recession. Source: BLS, Eurostat via FRED, Cleveland FedNBER, and the authors’ calculations.

Obviously, there will be a slight acceleration from the 2020M03. However, this acceleration is not statistically significant, considering inflation as stationary (and the price level as non-stationary). A statistically significant acceleration from 2021 on M04 is much better (2.1 percentage points relative to 2018-2021 M03 acceleration, 15% msl significance using HAC robust standard errors). In my opinion, 2.1 ppt makes economic sense, even if it is not statistically significant in this case. Given the timing, this is likely to come from a demand pull (or at least a combination of commodity demand pull and capacity) rather than a cost push shock.As mentioned, this timing is also consistent with a smaller (absolute) output gap between the US and the euro area in 2021 here.

(The log price ratio can be treated as an I(0) series versus an I(1) series with structural breaks using the Bai-Perron test. Statistically significant breaks can then be rejected in favor; see this postal.)

{kind=link}

{kind=link}