Do you use…inflation or price levels to calculate inflation differentials?follow up on this debate Started over a year ago.

Here is a time-series plot of the log ratio of US CPI to Eurozone’s 19-year HICP (seasonally adjusted by the authors using X13) (blue line, left scale), and the annualized month-to-month inflation differential (tan line, right scale).

figure 1: Log ratio of CPI for all US cities to Eurozone 19 HICP (blue line, left scale) and month-to-month annualized inflation differential in % (brown line, right scale). HICP uses X13 logarithmic transformation for seasonal adjustment, X11 ARIMA seasonal adjustment. Inflation difference calculated using first difference of logarithms. Sources: BLS, EC via FRED, and authors’ calculations.

Summary of log ratio results:

- ADF unit root test: failed to reject 10% msl.

- DF-GLS (ERS) unit root test: failed to reject 10% msl.

- KPSS Trend Stationarity Test: Rejection of 1% msl.

- The Bai-Perron structural fracture test of L+1 and L sequentially identifies fractures: no fractures selected.

Summary of test results for m/m inflation rate differences:

- ADF unit root test: Reject 1% msl.

- DF-GLS (ERS) unit root test: 1% msl rejected.

- KPSS Trend Stationarity Test: Failed to reject 10% msl.

- The Bai-Perron structural fracture test of L+1 and L sequentially identifies fractures: no fractures selected.

What about the core?

figure 2: Log ratio of US core CPI to Eurozone 19-year HICP core (blue line, left scale) and month-on-month annualized inflation differential in % (brown line, right scale). HICP uses X13 logarithmic transformation for seasonal adjustment, X11 ARIMA seasonal adjustment. Inflation difference calculated using first difference of logarithms. Sources: BLS, EC via FRED, TradingEconomics and authors’ calculations.

Summary of core log ratio results:

- ADF unit root test: failed to reject 10% msl.

- DF-GLS (ERS) unit root test: failed to reject 10% msl.

- KPSS Trend Stationarity Test: Rejection of 1% msl.

- Bai-Perron Structural Fracture Test L+1 vs. L order to determine fractures: 5 fractures selected; last one at 2019M05.

Summary of test results for core m/m inflation difference:

- ADF unit root test: Reject 1% msl.

- DF-GLS (ERS) unit root test: 1% msl rejected.

- KPSS Trend Stationary Test: Failed to reject at 1% msl, rejected at 5% msl.

- Bai-Perron Structural Fracture Test L+1 vs. L order to determine fractures: select 2 fractures; last one at 2013M04.

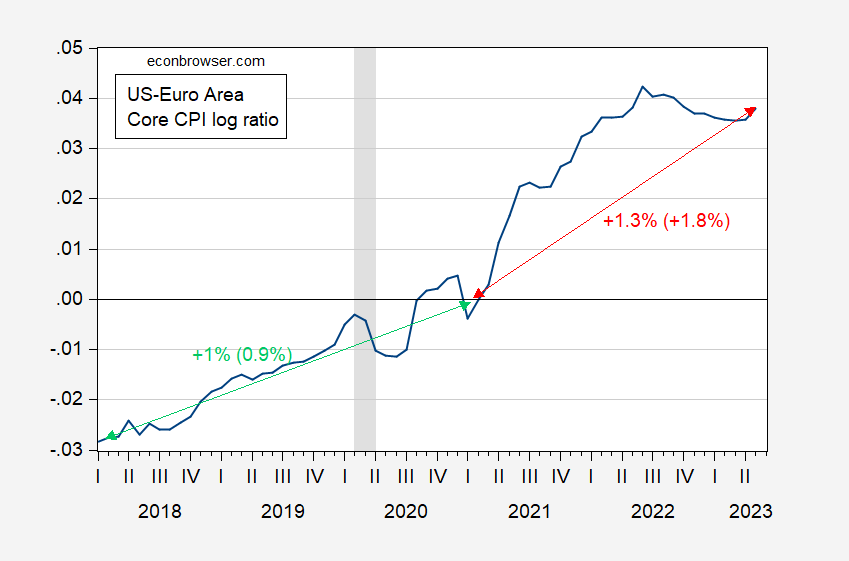

While the trend break in 2021M02/03 is not statistically significant for the core (using dummy variables for inflation differences, or dummy variables interacting with the price ratio trend), you can see an acceleration relative to the core.

image 3: Log ratio of US core prices to Eurozone-19, 2020M02=0 (blue). Green (red) arrows are deterministic trends, numbers (in brackets) indicate deterministic (stochastic) trend growth rates. Dates of peak-to-trough recessions as defined by NBER are shaded in gray. Sources: BLS and EC via FRED, TradingEconomics, NBER and author’s calculations.

Literally looking at the segmented trend, starting from February 2021, the core CPI growth rate in the United States will be 0.3 percentage points faster than that in the euro zone.

For more information on deterministic, random, and segmented trend tests , see Cheung and Chinn (Oxford Economics Papers, 1996), Cheung and Chinn (JBES, 1997)and Cheung, Chinn and Tran (AEL, 1995).

{kind=link}

{kind=link}