Inflation data from the US Bureau of Labor Statistics yesterday (July 12, 2023) – Consumer Price Index Summary – June 2023 – Suggesting a further sharp decline in inflation, as some key supply-side drivers continue to weaken. Annual inflation is now back at 3% and is falling fast. The risk now is that the Fed’s actions will lead to a period of deflation in the US, with higher unemployment. Given that inflation peaks in the third quarter of 2022, wage growth is relatively weak, and the survey evidence for inflation expectations shows that no one really thinks inflation will persist, this means that the Fed’s logic is deeply flawed and does not hold. fit for purpose. They have been chasing an obsession that exists from the parallel universe to the real world. The risk is that they will continue to chase this obsession and use the fact that the unemployment rate has not risen much to claim that it must be higher. However, hopefully yesterday’s 3% inflation result will dispel any crazy talk that they have to cut inflation faster or risk a wage or expectations explosion. Of course not everything.

US Inflation Situation

The U.S. Bureau of Labor Statistics (BLS) released its latest monthly Consumer Price Index (CPI) yesterday, showing that for June 2023 (seasonally adjusted):

- The All Items CPI rose 0.2% MoM and 3% YoY (down from 4.1% in May).

- In June 2022, the peak monthly increase will be 1.2%.

The U.S. Bureau of Labor Statistics states:

The housing index was the largest contributor to the monthly increase in all items, accounting for more than 70% of the increase, and the motor vehicle insurance index also contributed.

The food index rose 0.1% in June after gaining 0.2% in the previous month… The energy index rose 0.6% in June, with the main energy component index mixed.

The all commodities index excluding food and energy rose 0.2% in June, the index’s smallest one-month gain since August 2021. …

The All Items Index rose 3.0% in the 12 months to June; The index for all items excluding food and energy has risen 4.8% over the past 12 months. The energy index fell 16.7 percent in the 12 months to June, while the food index rose 5.7 percent from a year earlier.

Abstract: Inflation in the United States is falling rapidly, largely reflecting the dynamics of energy prices, which not only contribute by themselves, but also affect other CPI components (such as food delivery costs, etc.).

Energy prices have fallen 16.5% since their peak in August 2022.

Food prices are still rising, albeit at a much slower pace, as the lagged effects of energy inflation are playing out.

This inflation episode, although distorted by events that no one saw coming (Ukraine), is clearly a blip.

When I first speculated about the sustainability of this episode, I was criticized.

As I said at the time, “temporarily” does not necessarily mean a short period of time.

Rather, it means that once the factors driving inflation have weakened, we will see a sharp decline in interest rates.

Another way to think about it is that a transient period is one in which there is no sustained inflation driven by real income headwinds from capital and labor.

Unlike the 1970s, there is clearly no wage factor driving inflation.

The only thing I would point out is that we also didn’t expect companies to blatantly push up margins, even with benign wage growth, which has led to a degree of persistence.

In May 2023, an interesting paper was published in the American Economic Association (AEA) Papers and Proceedings – The Wage Phillips Curve Under Labor Market Forces (Link to working paper version) Published July 2022.

The authors wonder why the U.S. (and certainly elsewhere) have seen “sluggish wage growth despite strong job growth”.

They point out that if the relationship between wage growth and unemployment becomes very flat (i.e., a sharp fall in unemployment does not trigger a rise in inflation), then attempts by central bankers to manipulate unemployment to curb inflation will be ineffective.

In theory, this calls the entire NAIRU story into question.

Pushing up unemployment only hurts those who have lost their jobs and homes to the loss of income and stigma, and it does nothing to lower inflation.

They “use online job openings in the U.S.” to:

…examining the interplay between labor market forces and monetary policy. Our experience shows that labor market forces amplify the impact of monetary policy on labor demand without disproportionately affecting wage growth.

They found:

1. “U.S. firms are known to have strong labor market power that allows them to ‘mark down’ wages from the marginal product of labor” – meaning that U.S. employers take advantage of unequal power in labor exchange to drive wages down below productivity Grow and claim more for yourself.

2. “Easy monetary policy can cause unemployment to fall, decoupling growth from wage growth” – meaning that when the economy grows, unemployment falls but wages grow very little.

3. This also means that when monetary policy pushes up unemployment, it has little effect on inflation.

This, in turn, means that central banks following the NAIRU narrative (inflation suppressed by rising unemployment) will continue to push interest rates higher until unemployment is substantially higher, in a vain pursuit of lowering inflation.

In the current context, where inflation is supply driven anyway and has little to do with wage pressures, such a pursuit by central banks would be hugely damaging to the unemployed, while inflation would fall independently (as supply forces weaken).

If central bankers don’t stop raising rates, that’s where we’re headed.

Anyway, back to the current data release.

The chart below shows the importance of energy prices to the overall US inflation rate.

The simple regression line (dashed line) yields R2 0.48. This means that about 48% of the change in headline CPI is driven by changes in energy prices.

It’s a bit more complicated than statistical terms, but this rough figure can be a good guide to the influence of energy prices.

In fact, the sharp drop in U.S. inflation has been attributed to sharp falls in energy and gasoline prices.

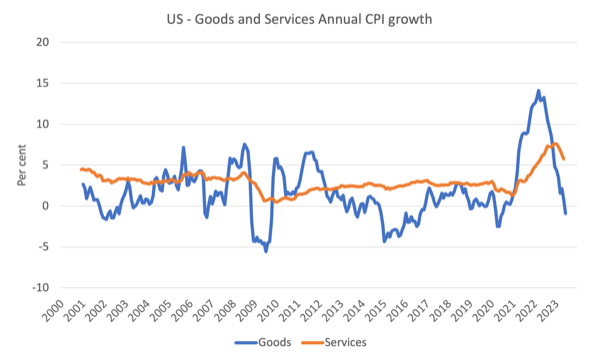

The chart below shows the evolution of annual price increases in the goods and services sectors since 2000 until June 2023.

Inflation has long been thought to be largely driven and instigated by supply factors that limit the economy’s ability to meet demand for goods — COVID-19 disruptions to factories and transportation, among others.

The graph clearly shows that these factors have been fading since the second half of 2022 as supply chain constraints ease.

The services sector, a derivative of supply drivers, has lagged behind the goods sector, which, while still recording higher inflation than the goods sector, has now peaked and is declining.

Inflation has fallen sharply, while the U.S. labor market has remained fairly stable.

In this blog post I analyze the latest jobs release from the Bureau of Labor Statistics — U.S. labor market softens – job vacancies fall, underemployment rises (July 10, 2023).

While job growth has slowed slightly, there are no signs of a recession-style significant slowdown.

Crucially, the lack of correspondence between labor market dynamics and inflation dynamics suggests the anemic logic the Fed will use to justify its rate hikes.

The research paper I discussed above reinforces this point.

The logic of the Fed is about the strength of the labor market (they think the real unemployment rate is lower than NAIRU), which drives them keen to create more unemployment and suppress wage growth, thus preventing the development of inflation.

Therefore, these data are not friendly to the logic of the Fed.

Inflation is coming down fairly quickly because the main drivers that are not particularly sensitive to interest rates are coming down.

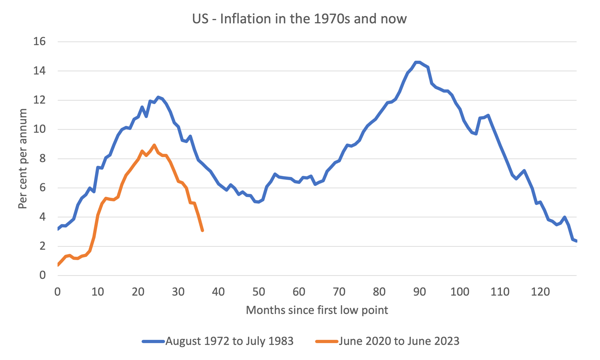

Consider the next chart which shows the 1970s inflation period from October 1972 to July 1983 which actually lasted just under 11 years and the current inflation period from June 2020 By June 2023 (current data).

The horizontal axis starts each series with the month the inflation event actually started and then tracks the evolution over the following months.

In the first episode, the trajectory is from the initial low point (October 1972) to the next time inflation returns to that level (July 1983).

That event was delayed.

Inflationary pressures had already emerged in the late 1960s due to spending related to the Vietnam War.

It began to weaken in early 1972, but really accelerated after the first OPEC oil crisis in October 1973.

As you can see, wage price pressures pushed up inflation until the situation was resolved, exacerbated by the second OPEC oil crisis in late 1978 as the Iranian revolution disrupted oil supplies.

In stark contrast, current supply-driven events without any additional transmission mechanisms at play (e.g., wage pressures following supply-side shocks) imply that inflation is not anywhere near the levels reached in the 1970s And quickly turn around and come down.

It will run out in about 40 months.

in conclusion

Inflation will soon disappear.

I think my assessment that this will always be a transition period for inflation is borne out by the data.

I also think that our understanding and practice of monetary policy has reached the peak of madness.

Enough for today!

(c) Copyright 2023 William Mitchell. all rights reserved.

{kind=link}