The U.S. Bureau of Labor Statistics released the latest U.S. inflation data last week (August 10, 2023)—— Consumer Price Index Summary – This points to a monthly headline inflation rate of 0.2%, mainly driven by the housing market. And, once we understand how the housing component is calculated, there is every reason to believe that this major driver of the current inflation rate will weaken significantly in the coming months. The rent component of the CPI has a big impact on headline inflation, and Fed rate hikes push headline inflation higher.

US Inflation Situation – Summary

The U.S. Bureau of Labor Statistics (BLS) released its latest monthly Consumer Price Index (CPI) yesterday, showing that for July 2023 (seasonally adjusted):

- The CPI for all items rose 0.2% MoM and 3.2% for the year (3% in June).

- In July 2022, the peak monthly increase will be 1.2%.

- The biggest contributor is housing (sort of).

The U.S. Bureau of Labor Statistics states:

The housing index was by far the largest contributor to growth for all items each month, accounting for more than 90% of the increase, and the motor vehicle insurance index also contributed.

Abstract: The supply-side inflation triggered by this event has now become a housing problem, reflecting poor overall policy design.

Energy prices had been an important driver, falling 12.5% in the 12 months to July.

Fuel prices have dropped 26.5% over the past 12 months.

The overall monthly increase was fairly modest.

Interestingly, housing inflation is much lower where municipalities provide social housing opportunities (affordable housing).

In the Bloomberg article (August 9, 2023) – First U.S. city to tame inflation credits its success to affordable housing – we read:

Nowhere in America has inflation been factored into the rearview mirror at such a rapid pace as Minneapolis.

In May, the Twin Cities became the first major metropolitan area to have annual inflation below the Fed’s 2% target. Its 1.8% price increase was the slowest of any region for the month…

Long before pandemic-related supply chain disruptions and labor shortages disrupted the economy, the city of Minneapolis eliminated zoning that only allowed the construction of single-family homes and has invested $320 million since 2018 in rental assistance and subsidy……

Housing initiatives — including the Itasca Project, the region’s coalition of business, philanthropy and public sectors pushing to build at least 18,000 new homes a year by 2030 — have picked up the hole left by the Fed’s tightening monetary policy, Shows the role of the state and local policies can play a role in curbing inflation.

So we see very clearly how insightful policy design can be very effective in removing supply bottlenecks that drive inflation.

While this blog post is about the situation in the US, there was an important event in Australia last Friday, following on from the comments above, about a more than neo-Keynesian approach to dampening financial investment in infrastructure, especially accessible social housing. Comments on a good way to deal with inflation and rely on raising interest rates to deal with inflationary pressures.

Clearly, raising interest rates is not an effective anti-inflationary tool when supply factors or international factors are driving the pressure.

All the talk of fighting inflation by driving unemployment into the “mysterious” NAIRU (core of New Keynesian orthodoxy) is just a hoax.

Central bankers know little about what’s going on in NAIRU, and little is known about the eventual net distributional impact of a rate hike.

They just hope and pray.

Last Friday (August 11, 2023), the outgoing Governor of the Reserve Bank of Australia (who was effectively sacked by the federal government – in the sense that he was not re-elected) appeared with the House Standing Committee on Economics last meeting.

in his – Opening address to the House Standing Committee on Economics – He goes through the usual woes.

But in a question-and-answer session (full transcript not yet available), the outgoing governor said that relying on rate hikes, a “blunt instrument”, was not the best way to deal with inflation.

He indicated that a range of fiscal tools could be better utilized:

…at a very high level, I still think it is worth considering the coordination between monetary and fiscal policy…

His excuse for using blunt hiking tools:

The reason monetary policy is really assigned to independent central banks is because the political class has a hard time doing what we’re currently doing. That is, raising interest rates…

Because monetary policy is blunt and … unbalanced, some people think it’s unfair, and I understand how people feel.

In principle, I think there are better ways to do this, but it’s difficult because of governance issues and when you limit the economy you can be unpopular, very unpopular.

But he acknowledged that his policy decisions had caused great pain to low-income families, but claimed he was more likely to be unpopular than the “political class”.

Why?

In his words because:

…the central bank…don’t have to worry about re-election and popularity,

But he also noted that some Asian countries were showing “closer cooperation between fiscal authorities and central banks”.

He did not mention Japan, but the Bank of Japan and the Ministry of Finance have developed fairer and more effective measures to counter the supply side, showing a willingness to cooperate and not follow the Western consensus on raising interest rates. Drivers of current inflationary pressures.

Unfortunately, House committee members did not clarify this further.

But this is clearly an acknowledgment that, because elected governments do not have enough insight to use fiscal policy in any other way than to glorify surplus creation, the central bank is forced to use the only tool it has, however unjust and unfair it may be. This may not be valid.

As a professional economist, I read his opinion between the lines as an admission that New Keynesian macroeconomics is flawed and ill-suited for its purpose.

Nothing new there.

Unfortunately, the committee did not question the Governor about the RBA’s role in driving up inflationary pressures, even though the initial drivers had subsided.

We now see clear evidence that rate hikes are themselves inflationary, a further indication of the poverty of current macroeconomic orthodoxy.

Current data release

Anyway, back to the current data release.

The first graph shows the evolution of monthly inflation rates since early 2015.

Even with housing, the overall picture is contained for now, in large part because energy prices have fallen sharply.

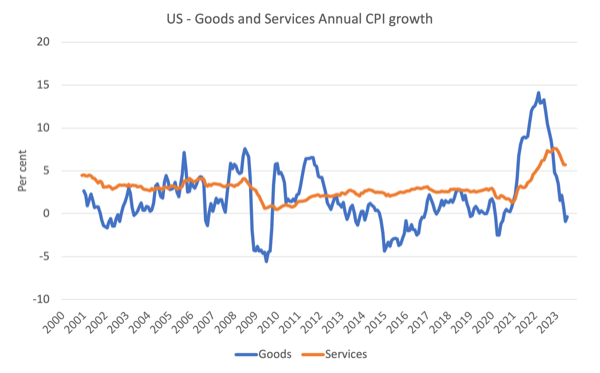

The chart below shows the evolution of annual price increases in the goods and services sectors since 2000 until July 2023.

Inflation has long been thought to be largely driven and instigated by supply factors that limit the economy’s ability to meet demand for goods — COVID-19 disruptions to factories and transportation, among others.

The graph clearly shows that these factors have been fading since the second half of 2022 as supply chain constraints ease.

The services sector, a derivative of supply drivers, has lagged behind the goods sector, which, while still recording higher inflation than the goods sector, has now peaked and is declining.

Cargo time series is now recorded monthly deflation past two consecutive months.

Another point worth noting (as mentioned above) is that rent inflation has been a big part of the overall inflation story.

There are two related aspects.

First, it’s a component driven by Fed rate hikes.

In a fairly tight rental market, landlords facing higher mortgage costs can easily pass on rate hikes to higher rents.

This is the only way a central bank can actually cause inflation in the process of taming it.

But, secondly, there’s an interesting part of the way the BLS measures the rent component, and it tells me that inflation in the US is going to come down fairly quickly.

Since the end of 2021, the rental vacancy rate, which measures the proportion of rental inventory that is vacant for rent, has risen from 5.6% to 6.3% in the June 2023 quarter (source).

Another point to note is that the way the Bureau of Labor Statistics measures changes in rental prices is through a monthly measurement to capture the “year” of price impact – that is, the results released each month include new leases plus past leases

So there’s a lag effect in operations, as the new lease rental amount declines, the overall series declines more slowly.

This BLS Spotlight Statistics Page – Residential Rentals in the US Rental Market – provides a more detailed explanation of all this.

It will take about 12 months for the series to reflect what new leases look like in the current CPI results.

We know rents are coming down for new leases.

Data via Zillow (August 10, 2023) – Headline inflation rose less than expected in July, limiting gains in Treasury yields and mortgage rates – Reveal:

While core inflation remains high relative to the Fed’s target and housing costs remain the largest contributor to the monthly increase in core CPI, the rent component of the CPI is expected to continue to trend lower. This is because rent increases have fallen far more than reflected in the CPI calculations. Annual growth in the Zillow Observed Rent Index (or ZORI), a measure of market rents, has slowed to 3.6% from a peak of 16% in February 2022.

As a result, we expect the housing component of the US CPI to decline and headline inflation to decline substantially in the coming months.

in conclusion

Inflation will soon disappear.

My conclusion is that this brief period of inflation is coming to an end.

Enough for today!

(c) Copyright 2023 William Mitchell. all rights reserved.

{kind=link}