I read an interesting report this morning that resonates with some other work I looked at earlier this week. The Australian Council of Social Services (ACOSS) released a report yesterday (September 27, 2023) – Inequality in Australia in 2023: An overview – This shows that “the gap between those with the most wealth and those with the least has widened over the past two decades, with the average wealth of the top 20% growing four times as fast as the bottom”. This is one of the manifestations of the neoliberal era, which is ultimately unsustainable. Earlier this week, I spent some time analyzing the latest data from the Federal Reserve on the distribution of wealth among U.S. households. The U.S. data goes a long way toward explaining why the recent rate hikes themselves stoked inflation.

Incidentally, a less often recognized feature of neoliberalism is the way it creates schizophrenic welfare institutions—institutions in which key organizations that provide or advocate for improved safety nets or poverty alleviation take internally inconsistent positions, And doesn’t seem to know it.

A clear example of this schizophrenic behavior in Australia over the past few decades has been the church-based welfare organizations that were roped in to tender contracts to deliver the government’s privatized employment services disaster, and became the focus of forced unemployment and reporting breaches. Frontline troops. Tests of income support activities are returned to the government, along with emergency food relief and more.

While they preach love and forgiveness, they have also become vehicles for the most vicious treatment of the most vulnerable in our society.

Earlier this week I commented on the federal government’s white paper on full employment – Australia’s new full employment white paper is useless and will only reinforce the failed NAIRU cult (September 26, 2023) —The title sums up my thoughts on this.

I didn’t expect Australia’s peak welfare body to praise this white paper.

ACOSS did just that when it released shocking wealth inequality data in the same week.

In its press statement (September 26, 2023) – The white paper lays a good foundation for full employment, clear goals and objectives are the missing planks – ACOSS is generally uncritical and seems unaware that the “missing plank” it identifies is precisely why the foundation laid by the White Paper is more similar to NAIRU neoliberalism.

The “missing plank” is the logical consequence of a supply-side approach that relies on a changing notion of maximum employment to justify not actually pursuing true full employment.

I’ve had a few radio interviews this week and I’ve been asked why the government doesn’t actually “fix” the full employment unemployment rate.

The reason is that they will be forced to leave the NAIRU world.

Anyway, this is a digression.

Australia’s inequality

ACOSS research (in collaboration with researchers at the University of New South Wales) reveals:

1. “Wealth inequality has increased dramatically over the past two decades.”

2. “From 2003 to 2022, the average wealth of the top 20% increased by 82%, the average wealth of the top 5% increased by 86%, the remaining middle 20% (increased by 61%) and The bottom 20% (increased 20%).”

3. “The overall increase in wealth inequality during this period was mainly driven by superannuation, which increased in value by 155% due to forced savings for real estate investment.”

4. “The richest 20% hold 82% of all investment properties by value.”

The fact that it is property investment that drives this wealth inequality reflects a bias in the tax structure that rewards holding a variety of properties through tax breaks.

The first thing the government should do is remove the so-called “negative gearing” provision in the tax code, which allows wealthy people to buy property and manipulate the cost of renting it to offset “lost” other income while the value of the property rises And accumulate huge capital gains.

Interestingly, this is exactly what resonates with US data, where the researchers found:

…the government’s timely pandemic response has reduced income inequality…In 2020-21, the average income of the bottom 20% of income groups increased by 5.3%, while the average income of the middle 20% of income groups increased by 2%, and the average income of the top 20% of income groups increased by 2% Average income increased by 2.4%, mainly due to the introduction of COVID-19 income support.

This tells us that well-targeted fiscal policy is a very effective tool to improve the lives of low-income families.

Although the dominant view is that fiscal policy is an inferior tool because households stop spending when running deficits because they fear higher taxes in the future and need to save to pay them, the evidence exposes these core mainstream views as false. economic proposition.

Additionally, the researchers found:

However, the removal of these income supports in 2021-22 has largely reversed these trends, returning income inequality to close to pre-COVID levels.

Incomes have fallen across the board, but more so for those with the lowest incomes. The average income of the bottom 20% fell by 3.5%, while the average income of the middle 20% fell by 0.5% and the average income of the top 20% fell by 0.1%.

There is therefore no doubt that the prevalence and persistence of poverty is a matter of policy choice.

A government that issues money can always eliminate poverty, just as it can always eliminate mass unemployment if it wants to (the two are intrinsically linked).

The conclusion, therefore, is that if we observe rising poverty and high unemployment, then the blame lies squarely with policy failures.

Most people don’t think so, and the reason is that they are seduced by the myths my profession spreads.

Current Fed Wealth Distribution Release

Earlier this week I took some time to look at the latest version (September 22, 2023) — Distribute Financial Account (DFA) – Published quarterly by the Federal Reserve.

DFA data integration:

1. “Quarterly data on total balance sheets of major sectors of the U.S. economy”—U.S. Financial Accounts.

2. “Three-year comprehensive microdata on assets and liabilities of a representative sample of U.S. households” – Survey of Consumer Finances (SCF).

The data reveals some alarming developments.

The table below shows wealth in trillions of dollars by wealth percentile group, with the share of the total in parentheses.

The data shows several things, including:

1. The richest American families have an increasing amount of control over total wealth, while the bottom 50% of American families have a decreasing share.

2. Although the initial roots of the crisis lay in financial markets, the global financial crisis had a disproportionate impact on the poorest American households, while the wealthiest households were far less affected.

| date | Top 0.1% | 99-99.9% | 90-99% | 50-90% | Bottom 50% |

| Third quarter of 1989 | $1.76 (8.6%) | $2.84 (13.9%) | $7.64 (37.4%) | $7.41 (36.3%) | $0.78 (3.8%) |

| 2000 first quarter | $4.61 (10.9%) | $7.12 (16.9%) | $14.74 (35.0%) | $14.27 (33.9%) | $1.37 (3.3%) |

| Fourth quarter 2007 | $7.79 (11.9%) | $11.14 (16.9%) | $24.95 (38.1%) | $20.67(31.7%) | $1.21 (1.6%) |

| Fourth quarter 2010 | $6.93 (11.1%) | $10/77 (17.3%) | $24.67 (39.5%) | $19.63 (31.5%) | $0.37 (0.6%) |

| Second quarter of 2023 | $18.63 (12.8%) | $27.15 (18.6%) | $54.81(37.6%) | $41.74 (28.6%) | $3.64 (2.5%) |

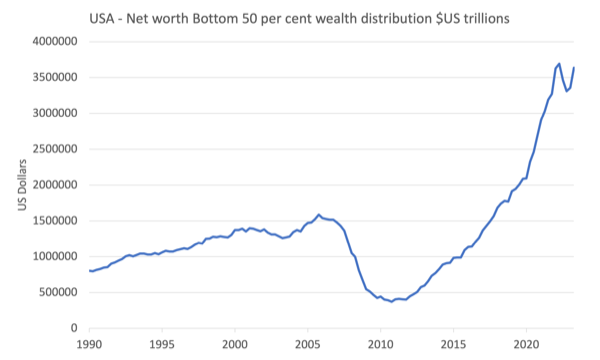

The chart below shows the net worth (in trillions of dollars) of the bottom 50% of U.S. households in the wealth distribution.

The negative impact of the global financial crisis was staggering, even though the decline in net worth began long before the crisis that disrupted financial markets.

Prior to the global financial crisis, the peak net worth of the bottom 50% of the population occurred in the fourth quarter of 2005.

Between then and the trough in the December 2010 quarter, the bottom 50% lost $1.21 trillion in wealth holdings, a 76.5% decline.

During this period, the total assets of the bottom 50% of the population fell $0.04 trillion while total liabilities increased $1.17 trillion

In more detail:

1. Real estate assets decreased by US$2.29 trillion, while consumer durables increased by US$1.12 trillion.

2. Home mortgage loans increased by US$80 trillion, and consumer credit increased by US$26 trillion.

So while debt has risen sharply, the asset backing it (housing) has fallen sharply in value.

There is also evidence that credit cards and loans are used to purchase consumer durables during periods of relatively flat income growth.

While the data is very complex and will take more time to really analyze, another thing that came out was the impact of fiscal intervention during the pandemic.

As can be roughly seen from the chart above, the net worth of the bottom 50% of the population increased sharply during the epidemic.

Expressed numerically:

1. From the March 2020 quarter to the March 2022 quarter, the net worth of the bottom 50% of U.S. households increased by $1.54 trillion, or 73.4%.

2. Total assets increased by US$2.3 trillion, and total liabilities increased by US$7.7 trillion.

3. Real estate main asset income is 1.3 trillion US dollars, and durable consumer goods are 0.49 trillion US dollars.

This period coincides with widespread financial support for American households.

But we need to be careful.

During the epidemic, most of the net worth growth of the bottom 50% of households in the United States came from the growth of home values, and home values skewed towards the high end of the bottom 50% of households.

This increase is only on paper until they sell, if they sell they will be entering an inflated market with a much higher mortgage servicing burden (due to higher home prices and higher interest rates).

In addition, the lower half of the bottom 50%, often renters, have been hit hard by both inflated property values and rising interest rates.

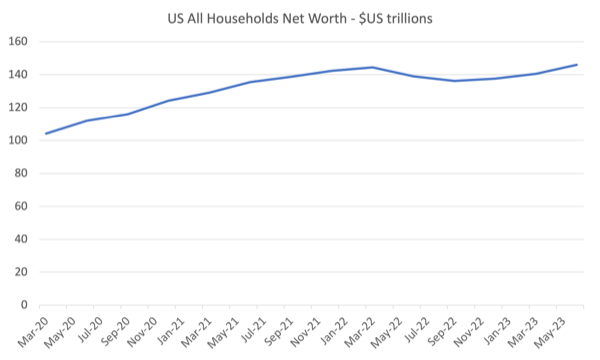

The final point I want to make at this stage is that total net worth has increased significantly across the board during the pandemic.

The chart below shows the March 2020 quarter to the June 2023 quarter.

We have noticed:

1. During this period, net assets increased by $40.3 trillion, or 36.7%.

2. Total assets increased by US$42.5 trillion, while total liabilities increased by only US$2.3 trillion.

3. The two main contributors to asset growth were real estate (up $11.8 trillion) and corporate and mutual fund stocks (up $18 trillion).

4. Of the $40.3 trillion increase in net assets:

– $6.4 trillion went to the top 0.1% of the wealth distribution.

– $9 trillion went to the 99th to 99.9th percentile group.

– $13.8 trillion went to the 90th to 99th percentile.

– $9.6 trillion goes to the next 40 countries.

– Only $1.5 trillion went to the bottom 50 people.

All of this occurred during a period of substantial fiscal expansion.

It tells me that the fiscal expansion has been poorly targeted, with wealthier American households owning real estate and financial assets (stocks, etc.) running wild while the bottom 50 households have stagnated.

in conclusion

This does help explain why rising interest rates have yet to lead to a sharp decline in spending or economic activity.

The net worth of people in the top 50% of the wealth distribution has increased rapidly during the epidemic, and as interest rates rise and their income increases, their spending power may also increase.

I would need to examine the income distribution data that accompanies this data set to draw further conclusions.

But overall very interesting.

That’s enough for today!

{kind=link}

{kind=link}