that’s the subtitle NBER working paper by Charles Gray, Abby E. Alpert, and Neeraj Sood. The authors examine recent mergers between pharmacy benefit managers (PBMs) and health insurers. On the one hand, consolidation may be good for consumers. It can: (i) improve operational efficiency, and (ii) better align PBM incentives with health plan incentives (eg, better accounting for healthcare cost offsets). However, the authors also point out that there are two avenues through which consolidation may make consumers worse off: (i) investment foreclosures and (ii) customer foreclosures.

Input foreclosures occur when an insurer owns a PBM that increases the cost or reduces the quality of service provided to an insurer that competes with its parent insurer. For example, a PBM could pass a larger share of manufacturer rebates to its parent insurer than to a competitor insurer. The degree to which you commit to foreclosure depends on the level of competition in the PBM market. If there are many competitors in the PBM market, then input cancellations are less likely because a competitor health plan experiencing input cancellations can switch to one of many independent PBMs. However, if the PBM market is highly concentrated, then there is a greater chance of putting into foreclosure because competitors plan to switch to another PBM with limited options. In contrast, customer foreclosure occurs when a downstream firm of a merged entity no longer buys inputs from its upstream competitor. For example, when an insurance company and a PBM merge, the insurance company’s health plan will always use the services of its own PBM, thereby reducing the number of potential customers for the stand-alone PBM. The reduction in the potential customer base may eventually lead to the exit of independent PBMs from the market, which will further increase the concentration of PBMs.

The authors used a number of different datasets, including (i) the publicly available CMS PDP Landscape document dataset on Medicare Part D plan characteristics and enrollment (2010-2018), (ii) CMS Part D contracts and enrollment data containing information about plans Annual Registration Information, (iii) Decision Resource Group

(DRG) Manage Market Surveyors (MMS) (2010-2018) to determine which PBM each Part D program uses.

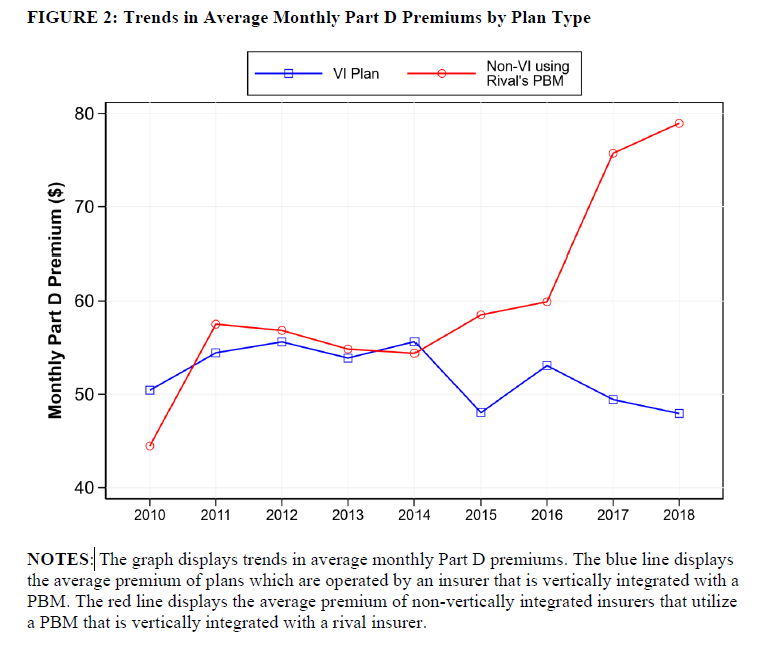

They then performed a difference-in-differences (DD) analysis of the Part D market before and after the 2015 merger of large insurers and PBMs (UnitedHealth-Catamaran), which the authors claim “eliminated the last significant stand-alone PBM and shifted more insurers Contract with a vertically integrated PBM.” The before-and-after analysis compared premium changes for vertically integrated plans (ie, plans to have their own PBM) versus non-vertically integrated plans.

Using this approach, the authors found that:

…non-vertical insurers saw premium growth 36% Compared to vertically integrated insurance companies. These findings are consistent with vertically integrated PBMs participating in input blockade. Specifically, vertically integrated PBMs have more incentive to drive up competitors’ costs when competitors lose the ability to substitute stand-alone PBMs.

The graph below shows that (i) vertically integrated plans are beginning to dominate the market and (ii) non-vertically integrated plans have seen higher price increases than vertically integrated plans.

{kind=link}