Due to the recent expected increase in inflation, the forecast price level (CPI) has been revised upwards. The recent GDP growth forecast has been revised upwards, but downside risks still exist. The output gap at the end of the year is expected to be small and positive.

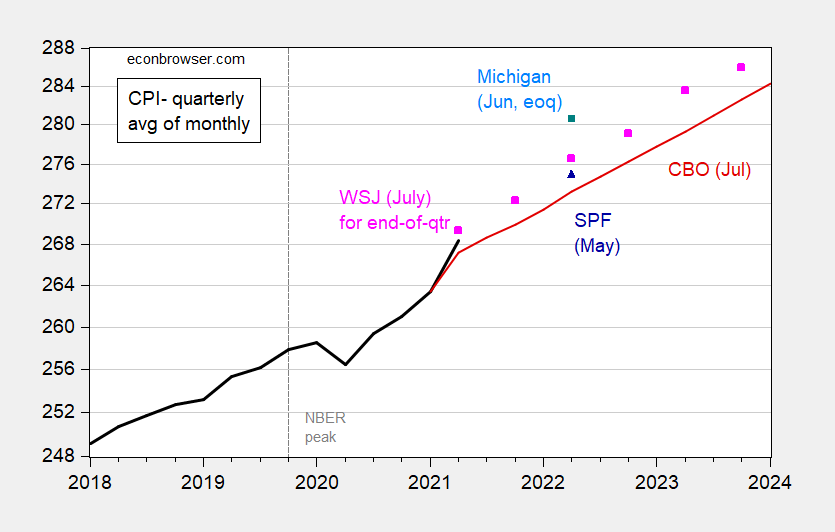

figure 1: CPI-All cities, quarterly average of monthly data (black bold), CBO forecast (red), Wall Street Journal survey average at the end of July (pink), Michigan consumer survey at the end of the quarter (blue square), The median of the survey of professional forecasters (blue triangle). The actual and implied levels of the CPI in the second quarter of June 2022 and the Michigan survey use Bloomberg’s consensus on the June 2021 CPI as of July 12th. NBER peak at the dotted line. Source: BLS via FRED, Wall Street Journal July survey, Michigan Consumer Survey, SPF/Philadelphia Federal Reserve, Bloomberg as of 7/12 and author’s calculations.

Please note that actual CPI data and CBO and SPF forecasts are quarterly averages for monthly data, while Michigan and Wall Street Journal forecasts are for the end of the quarter.

Show these in a comparable time series:

figure 2: CPI-All cities, quarter-end monthly data (black bold), CBO’s forecast of monthly data quarterly average (red), Wall Street Journal July quarter-end survey average (pink square), at the end of the Michigan Consumer Survey Quarter (blue triangle), Brian Wesbury, Robert Stein/First Trust Advisors (green +), Bill Diviney/ABN Amro (blue +). The June 2022 CPI actual and Michigan survey implied levels use Bloomberg’s consensus on June 2021 CPI as of July 12th. NBER peak at the dotted line. Source: BLS via FRED, Wall Street Journal July survey, Michigan Consumer Survey, Bloomberg as of 7/12 and author’s calculations.

The forecast means a slowdown in inflation (the index is on a logarithmic scale, so a flattened slope means a slower growth rate). Expectations of price increases vary considerably. Diviney/ABN Amro’s 90% lower limit (for next year’s inflation), and First Trust’s Wesbury and Stein top the list.

Note that Michigan’s y/y inflation estimate (4% in June) means that the CPI level is higher than the 90% upper limit of the CPI for professional forecasters.

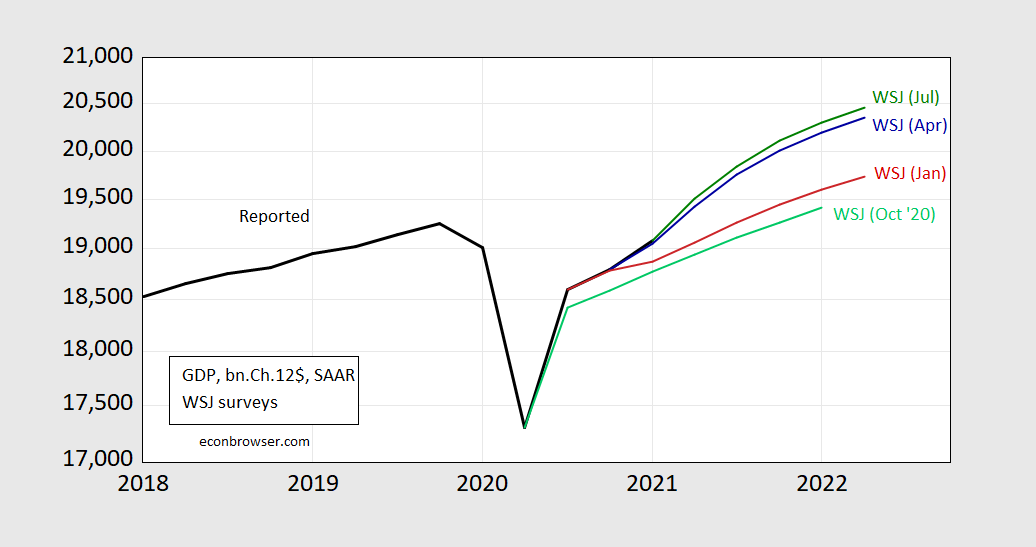

In terms of GDP, the forecast for GDP growth in the first quarter was raised again from April (The Wall Street Journal shifted from a monthly survey to a quarterly survey). The forecasts for the first quarter of 2020 in July, April, January and October are 9.11%, 8.15%, 4.91% and 3.72% (SAAR), respectively.

image 3: The reported GDP (black bold), the Wall Street Journal’s October 2020 survey (light green), January 2021 survey (red), April survey (dark blue), and July survey (green) are all expressed in ten. Millions of Ch. 2012 $ SAAR. Source: BEA, 3rd release in 2021Q1, “Wall Street Journal” survey of economists, various questions and author’s calculations.

The forecasts vary considerably, especially on the downside. In other words, most respondents agree that the next quarter (Q2) and the near future will achieve rapid growth, but some people believe that the downside risks of growth still exist.

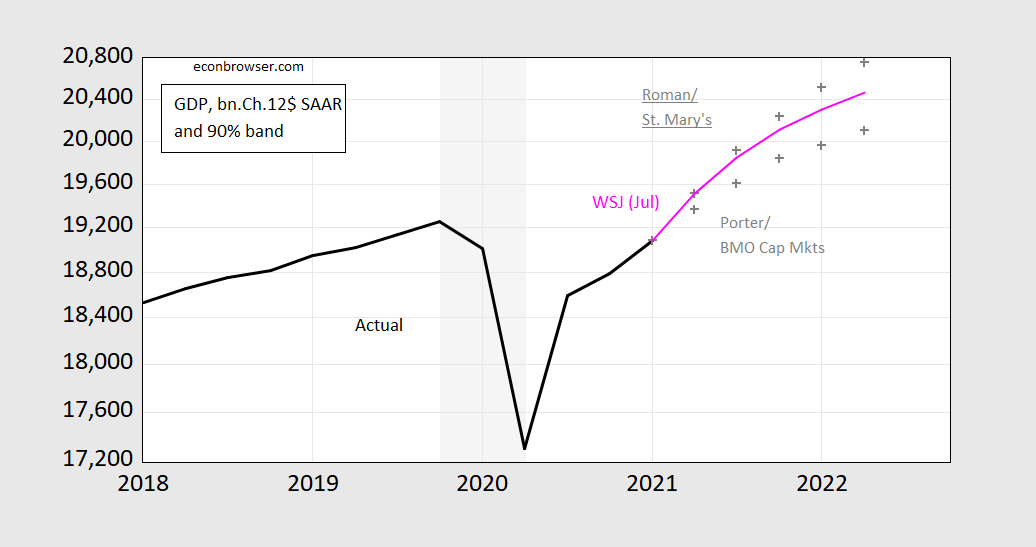

Figure 4: The reported GDP (black bold), July survey (pink), Belinda Roman (grey +), Doug Porter (grey +) are in the 90% range, all in billions of Ch.2012 $ SAAR. Source: Bureau of Economic Analysis, 3rd edition, first quarter of 2021, Wall Street Journal Economist Survey, July 2021, and author’s calculations.

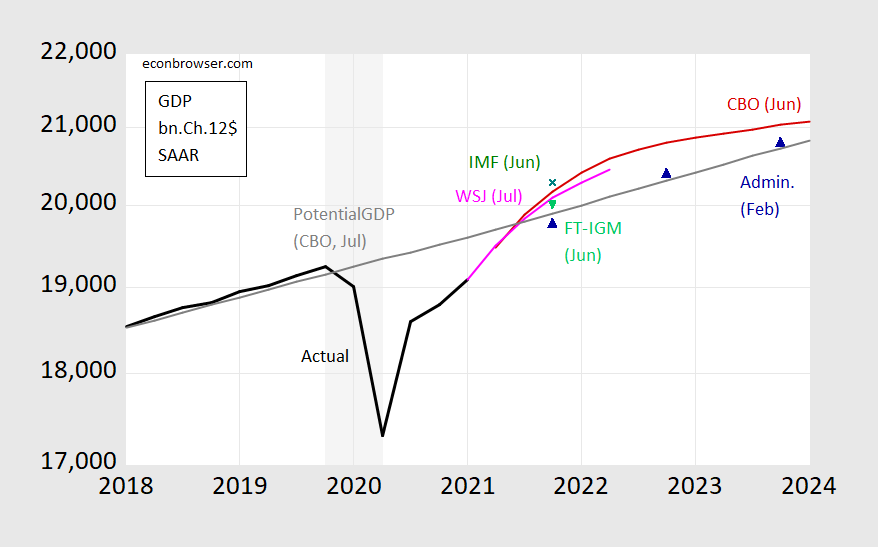

Figure 5: Reported GDP (black bold), WSJ July survey (pink), CBO (red), government department (blue triangle), IMF’s fourth article on the United States (green +), FT-IGM survey (light green) Triangle), all in billions of U.S. dollars. 2012 $ Sal. Source: BEA, 2021Q1 3rd release, WSJ economist survey, July 2021, IMF, FT-IGM June survey, and the author’s calculations.

Except for the government’s forecast, all forecasts imply a small positive output gap by the end of the year (using CBO’s estimate of potential).

{kind=link}

{kind=link}