Here are some indicators of the weekly frequency of the real economy.

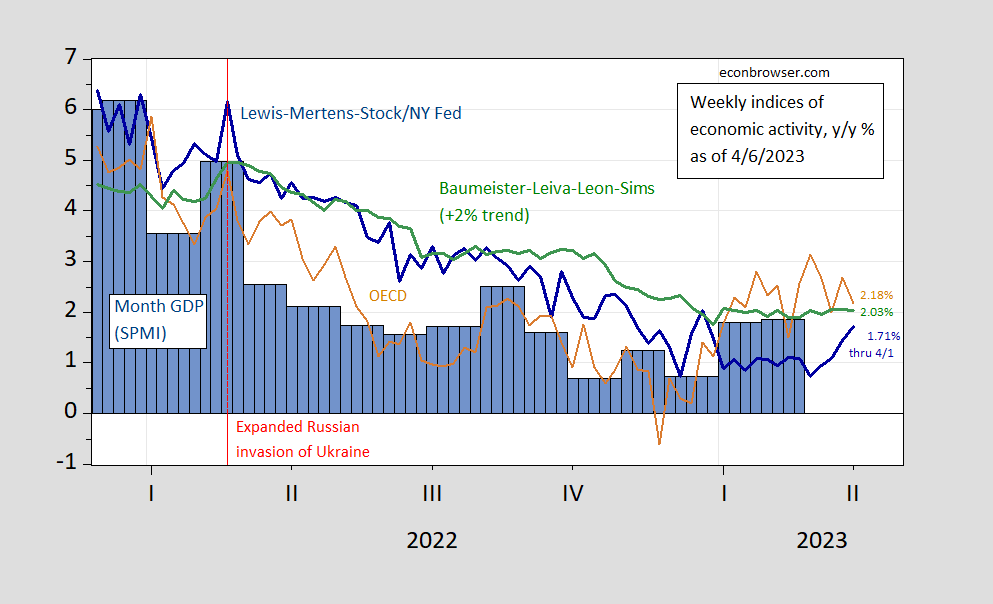

figure 1: Lewis-Mertens-Stock weekly economic index (blue), OECD weekly tracker (tan), Baumeister-Leiva-Leon-Sims weekly U.S. economic conditions index plus 2% trend (green), S&P Market Intelligence monthly GDP (blue bars), all growth rates (%).Source: S&P Market Intelligence, via NY Fed fred, OECD, WECIaccess 4/6, and author’s calculations.

The Weekly Tracker continued to grow at 2.18% for the week ended April 1, about the same as WECI +2% (2.03%). A WEI reading of 1.71% for the week ended April 1 could be interpreted as a 1.71% year-on-year increase if the 1.71% reading persisted throughout the quarter. Baumeister et al. A reading of 0.03% is interpreted as a growth rate of 0.03% above the long-term trend growth rate. US GDP growth averaged around 2% over the period 2000-19, so this translates to an annual growth rate of 1.97% as of April 1. The OECD weekly tracking index reading of 2.18% can be interpreted as a year-on-year growth rate of 2.18% as of April 1.

Recall that WEI relies on correlations of ten series available at weekly frequencies (e.g., unemployment claims, fuel sales, retail sales), while WECI relies on a mixed-frequency dynamic factor model. Weekly Tracker is a “big data” approach that uses Google Trends and machine learning to track GDP. As such, it does not itself depend on actual economic indicators.

If applied to Q1, the WEI reading implies 1.64% (q/q SAAR). As of April 5, GDPNow is 1.5% (q/q SAAR). That compared with 1.9 percent tracked by S&P Market Insights (nee Macro Advisers/IHS Markit).

{kind=link}

{kind=link}