Steven Kopitz Wrote:

We might expect that large-scale stimulus measures combined with a large number of job losses will lead to a surge in the trade deficit, and this is the case.

…

In extreme cases, such stimulus may even produce record levels of merchandise imports, and it has already done so.

…

The record import level will result in a record shipping level, and the flow at the port of entry in Los Angeles is about 15% higher than the previous peak. (Let me add here that U.S. shale oil production means that the oil trade deficit in U.S. history has disappeared. Since oil is mainly imported through Houston and several other ports-but not Los Angeles-the increase in port traffic is seen in commodities, Instead of oil, imports. That is, imports will be shipped to cargo ports such as Long Beach and Los Angeles.) These ports may not be able to handle the surge in cargo imports that are much higher than their historical peaks.

…

At the same time, unemployment accompanied by record-breaking stimulus measures may lead to weak exports, which is why exports are weak.

Let’s see if all of this makes sense. First, the “record-breaking” deficit? It’s affirmative in U.S. dollars—but it’s not in terms of a share of GDP.

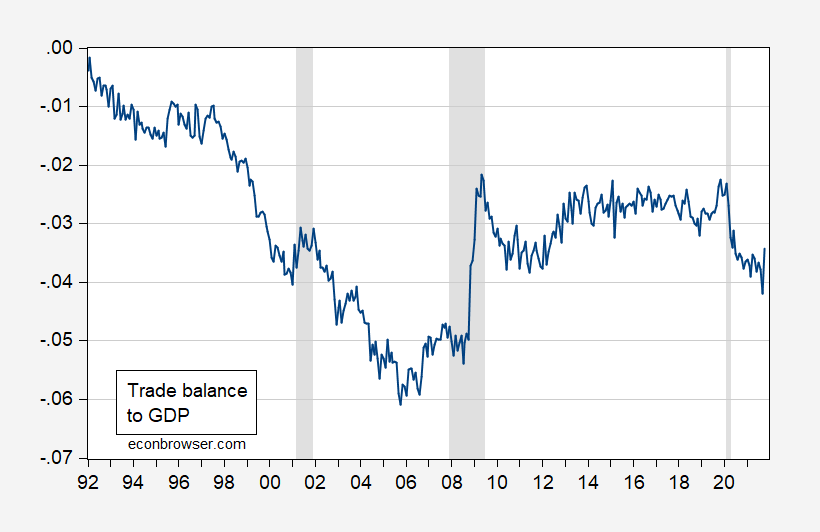

figure 1: Trade balance-goods and services (calculated in the balance of payments) as a share of GDP (blue line). Monthly GDP derived from quarterly GDP and SPF forecast for the fourth quarter of 2021. The NBER decline dates are shaded gray from peak to trough. Source: BEA/Census, BEA, Professional Forecaster Survey (November), NBER and author’s calculations.

In fact, the deficit calculated by GDP standardization did not set a record (which is very important), and the balance in October has actually been substantially restored.

Export collapse? Well, they did fall, but they are now rising sharply.

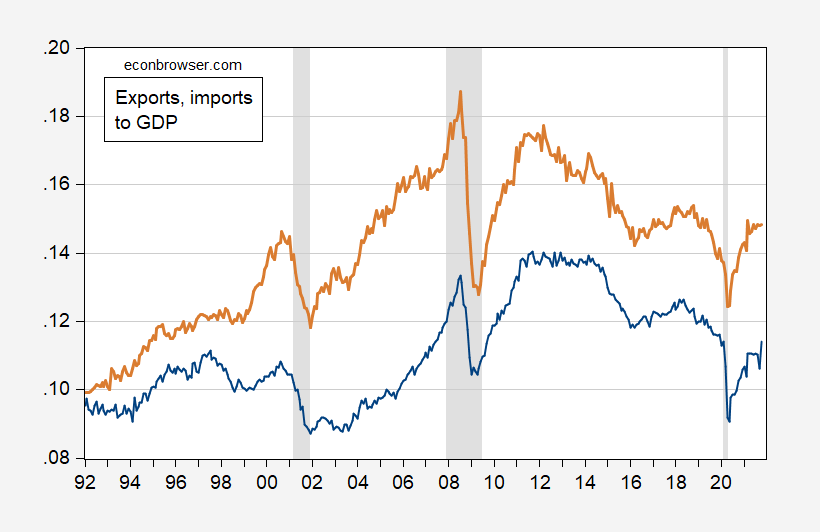

figure 2: Exports of goods and services (calculated in the balance of payments) as a share of GDP (blue line), imports (tan line). Monthly GDP derived from quarterly GDP and SPF forecast for the fourth quarter of 2021. The NBER decline dates are shaded gray from peak to trough. Source: BEA/Census, BEA, Professional Forecaster Survey (November), NBER and author’s calculations.

As part of nominal GDP, they are at the peak level of NBER, which is the share of 2020M02. Now, if anyone wants to argue that the stimulus measures transfer goods and services that could have been exported to domestic use, it certainly makes sense. However, the fact that imports fell at the same time weakened this argument.

So, what about the argument that unemployment associated with stimulus measures may weaken exports? I originally thought that given the continued growth of employment in the manufacturing industry, this would be an indisputable issue (the employment in this industry is only 2% below the peak NBER level). A more natural argument is that restricted demand for U.S. exports restricts actual exports — I’m not sure if I have seen an argument that stimulus (or enhanced welfare) somehow keeps workers away from manufacturing and other The work of the export department.

In other words, when people talk about “open economy macro”, they should probably learn one or two models that are applicable to open economy macro.

{kind=link}

{kind=link}