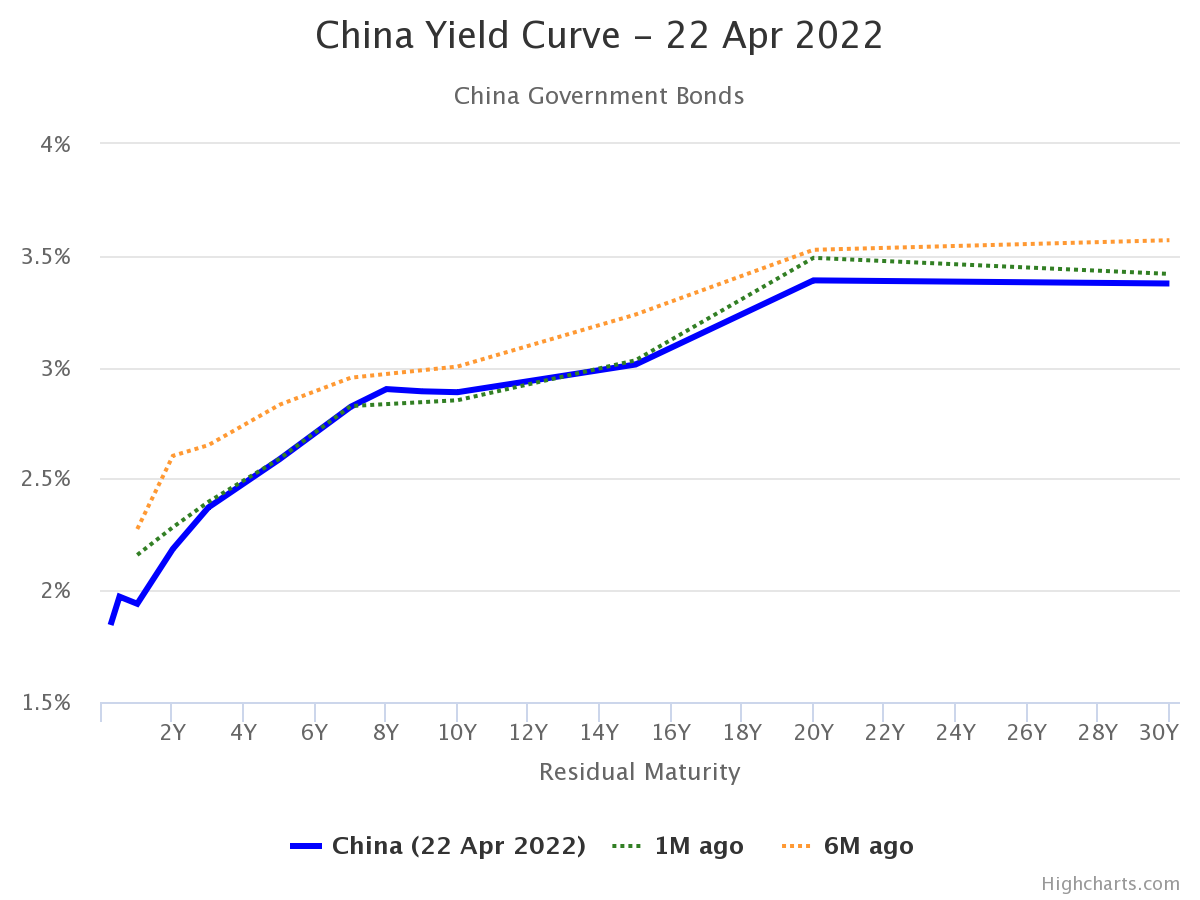

this government bond world The site offers 2s10s, 2s5s and 1s2s spreads for a whole bunch of countries (unfortunately, my favorite 3m10s is gone). Here’s China’s yield curve as of today:

source: worldofgovernmentbonds.com.

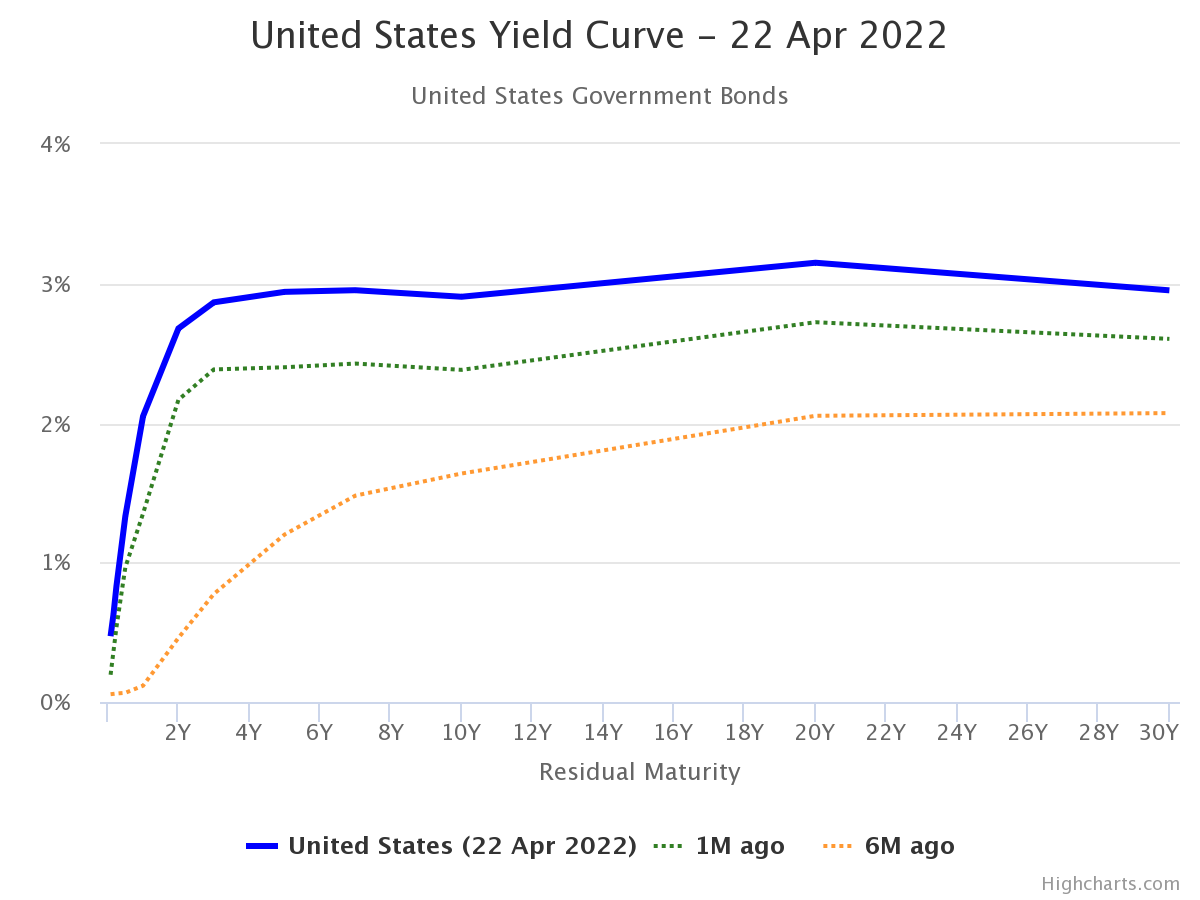

In comparison, this is the United States:

source: worldofgovernmentbonds.com.

It is this flattening of the U.S. yield curve that has prompted so many comments (see here).

Although this site tabulates these spreads as eg 10 years to 2 years (aka 2 years 10 years), do we know what this means for the country where the inversion occurs?

source: worldofgovernmentbonds.com.

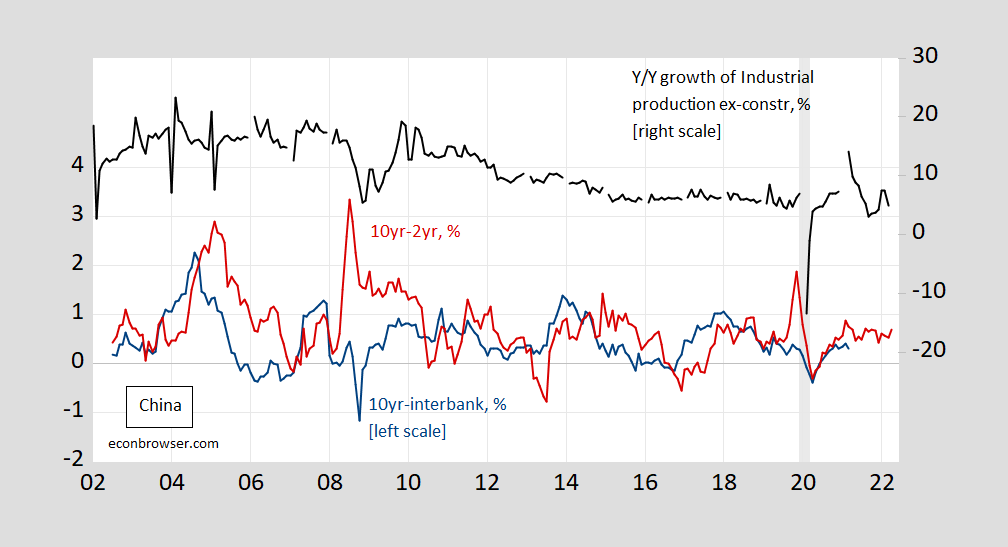

Here is a time-series graph of year-over-year growth in spreads and industrial production.

figure 1: 10- to 2-year Chinese government bond spreads (red, left scale), 10-year overnight interbank spread (blue, left scale), and industrial production year-on-year growth, % (black, right scale). ECRI-defined recession dates are shaded from peak to trough in gray. Source: invest.com, OECD via FRED, ECRI and author’s calculations.

The peak year-over-year IP growth at the start of the sample is due to the Lunar New Year holiday moving between January and February.

You’ll be forgiven for having a hard time finding the relationship between the lag term spread and 12-month IP growth visually. A simple regression yields:

Δipt+12 = 8.73 + 2.62spread10-2 yearsTon

adjust -R2 = 0.12, SER = 4.80, DW = 0.29, N = 212, where bold 5% significance was expressed using HAC robust standard errors.

However, the results are not robust to inclusion trends (which are evident in industrial production growth).

Δipt+12 = 152.68 + 0.43spread10-2 yearsTon – 0.06timeTon

adjust -R2 = 0.68, SER = 2.88, DW = 0.74, N = 212, where bold Indicates significance at 5% msl using HAC robust standard error.

The results are also not very robust for a truncated 2014 sample (IP growth is somewhat stable).

Δipt+12?sub> = 6.10 + -0.51spread10-2 yearsTon

adjust -R2 = -0.01, SER = 2.76, DW = 0.51, N = 79, where bold Indicates significance at 5% msl using HAC robust standard error.

Given the segmented nature of the Chinese government bond market, there are many reasons to believe that, in the case of the United States, the predictive power of term spreads will not transfer to China.as in Chen et al. (2019), the market is highly segmented, with little liquidity, until recently on longer maturities (eg 10 years). Most deals have a maturity date of 3 years. As far as I know, there are no studies evaluating the predictive power of long spreads;

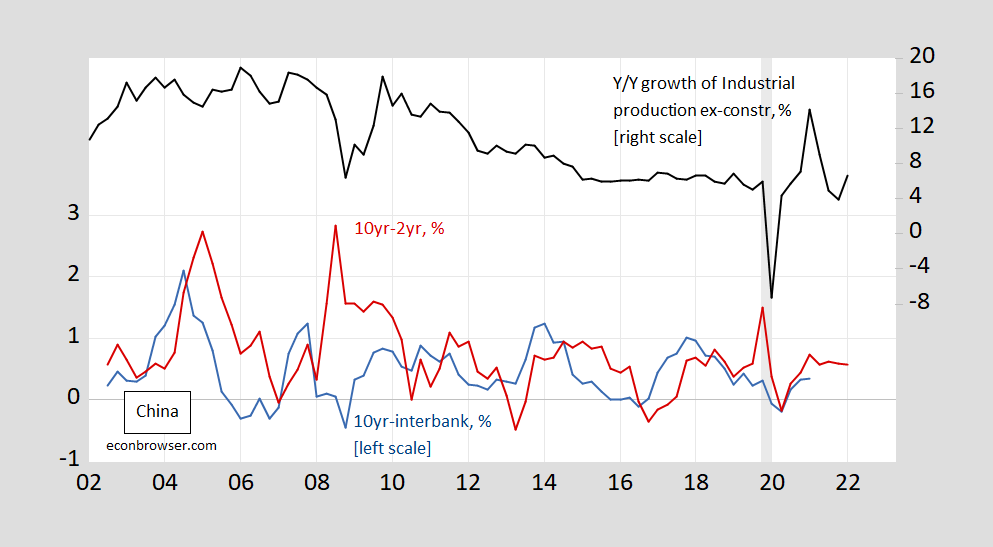

Turning to quarterly data:

figure 2: 10- to 2-year Chinese government bond spreads (red, left scale), 10-year overnight interbank spread (blue, left scale), and industrial production year-on-year growth, % (black, right scale). ECRI-defined recession dates are shaded from peak to trough in gray. Source: invest.com, OECD via FRED, ECRI and author’s calculations.

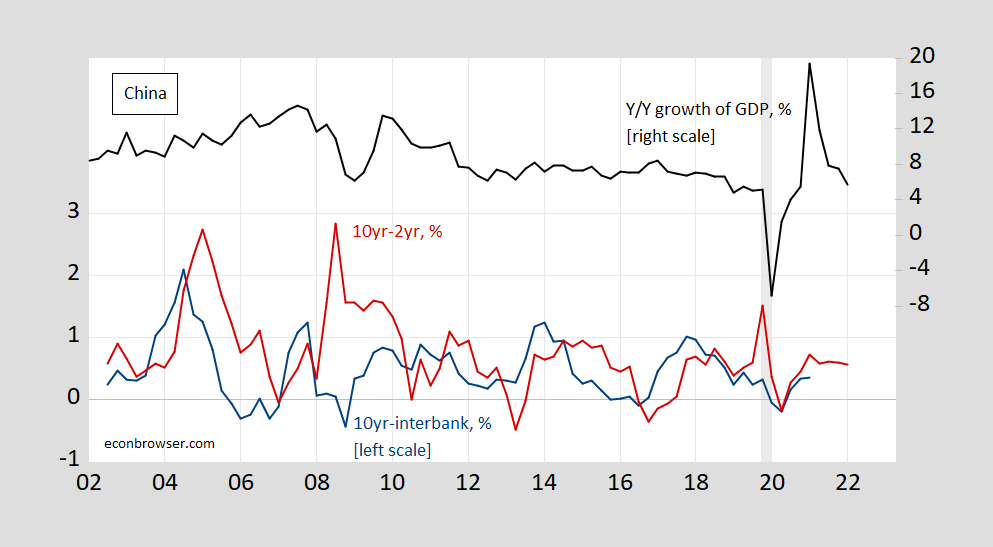

image 3: 10-year to 2-year Chinese government bond spreads (red, left scale), 10-year overnight interbank rate (blue, left scale), and year-on-year GDP growth, % (black, right scale). Nominal GDP is deflated by a deflator interpolated from an annual series of peaks to troughs on recession dates as defined by WEO ECRI, shaded in grey. Source: invest.com, National Bureau of Statistics, IMF WEO (April 2022), ECRI, and authors’ calculations.

Similar fragility results can be obtained using industrial production or GDP; the results are very sensitive to the inclusion of time trends. The most positive results (in terms of finding the role of term spread) were:

Δyest+4Ton = 7.60 + 1.43spread10-2 yearsTon

adjust -R2 = 0.06, SER = 3.40, DW = 0.78, N = 75, where bold Indicates significance at 5% msl using HAC robust standard error.

The spread coefficient drops to statistical non-significance when time trends are included. Enter the 2014-2022 shift period:

Δyest+4Ton = 9.35 + 0.71spread10-2 yearsTon – 3.11Fake2014-2022Ton

adjust -R2 = 0.22, SER = 3.09, DW = 0.90, N = 75, where bold 5% significance was expressed using the HAC robust standard error, and italic underline Indicates significance at 17% msl using HAC robust standard error.

Failed to find similar systematic relationships with developed countries (review Chin and Cuco (International Fin.2015) Given the existing literature (as far as I know; flour(open reactor2009) Investigating 5yr-3mo in emerging markets, while Haubrich (Pastor Ann2021) [ungated 2020 wp version] review some recent evidence).although Sowmya and Prasanna (references2018) Find the relationship between the slope and the subsequent output, it is a negative relationship. Zhang, Mattson and Tang (IJFS2019) Find larger adjusted one-year interbank spread forecasts Slower output growth. Interestingly, Jiang, Guo and Zhang (economic model.2017) Don’t use the spread as one of the useful growth predictors.

So, bottom line: you can calculate spreads, but the big question is whether they mean anything (for growth).

{kind=link}

{kind=link}