Today, we are delighted to receive from Jan Pam Jacobs University of Groningen, Samad Saferaz and Jan-Egbert Sturm Swiss Institute for Economic Research, and Simon of Norden HEC Montreal.

Two consecutive quarters of declines in real GDP are considered by many analysts to be a recession. But the latest GDP figures give conflicting signals.

Recessions are all about economic contractions—a drop in the rate of economic activity. That’s partly because the most popular recession indicator is real GDP falling for at least two consecutive quarters. on the basis of, Latest data from BEA It seems to indicate that the U.S. economy is in recession throughout the year: “headline” GDP contracted at an annual rate of 1.6% and 0.6% in the first and second quarters of 2022, respectively.

However, other metrics seem to tell a different story. During the same period, Inflation remains highThis Unemployment remains lowalthough employment , Personal consumption and Corporate profits continue to grow. These conflicting signals complicate the Fed’s task of achieving a “soft landing” while lowering inflation, clouding the rate outlook for borrowers and investors alike. How can they better understand how the economy is growing?

Part of the answer may be to look more closely at GDP data. It is understood that preliminary GDP data will be revised as more complete data become available. For example, the -0.6% figure for the second quarter mentioned above was revised from the original estimate of -0.9%. Further revisions are usually not enough to turn it into a positive value.[1] Yet another type of measurement error in GDP data is larger and has received far less attention. Differences between spending and income measures.

The basic principles of double-entry bookkeeping apply to GDP as they apply to the income statement of a company or household; every source of income is either spent or saved.This gives two different ways of measuring GDP: based on expenditure or based on income. “Title” GDP is expenditure based; it calculates GDP as the sum of personal consumption, private investment, net exports and government spending (Y = C + I + G + NX in your first economics textbook).But BEA also estimates GDI (gross domestic product) income), which includes wages and salaries, corporate profits, investment income, and some net transfers and taxes. If both GDI and GDP are measured correctly, they will give the same result. They are usually close; for example, GDI is estimated to be only 0.3% higher than GDP in 2019. Recently, however, the difference between the two has been greater, with GDI growing faster than GDP.[2] The latest figures show that GDI was 3.9% higher than GDP in the second quarter of 2022. Thus, while GDP contracted at an annual rate of 1.6% and 0.6% in the first and second quarters of 2022, GDI grown up It was 1.8% in the first quarter and 1.4% in the second quarter.[3]

So is the economy growing or shrinking? Which set of estimates should we trust? Part of the reason why “headline” GDP is based on expenditure estimates is that the BEA (like most other national statistical agencies) measures expenditure better than income.[4] However, this does not mean that GDI estimates should be ignored.due to earlier work Fixler and Nalewaik (2007) Regarding the usefulness of GDI, several studies have attempted to determine how much weight to assign to each of these two indicators to best estimate “real” GDP growth. Aruba et al. (2016) The proposal to slightly increase the weighting of GDI has led the Federal Reserve Bank of Philadelphia to issue what they call a composite estimate GDP plus. The estimate has remained positive since Q3 2020 and is at 1.8% in Q2 2022 (ie, even higher than GDI). The BEA has started publishing the growth rates of the simple averages of its GDP and GDI estimates, ie 0.1% and 0.4% in the first and second quarters, respectively.[5]

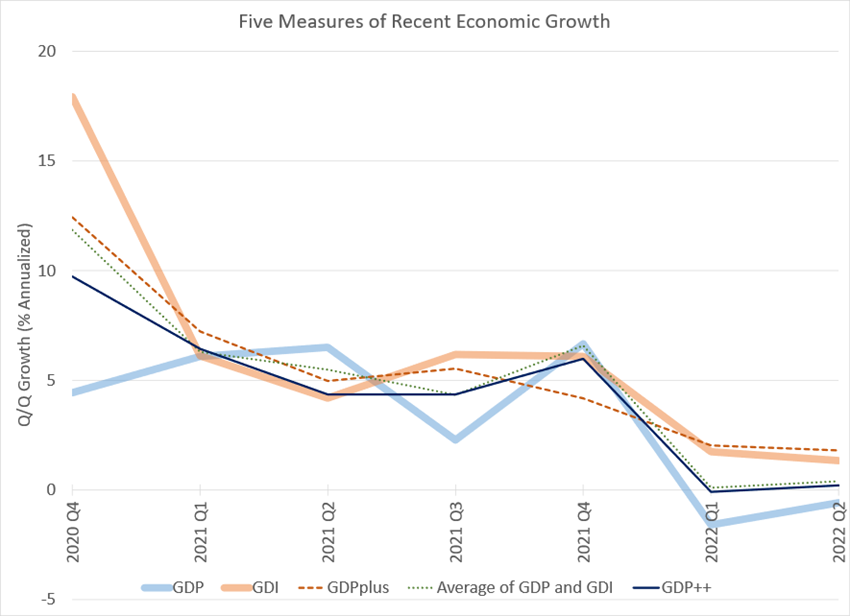

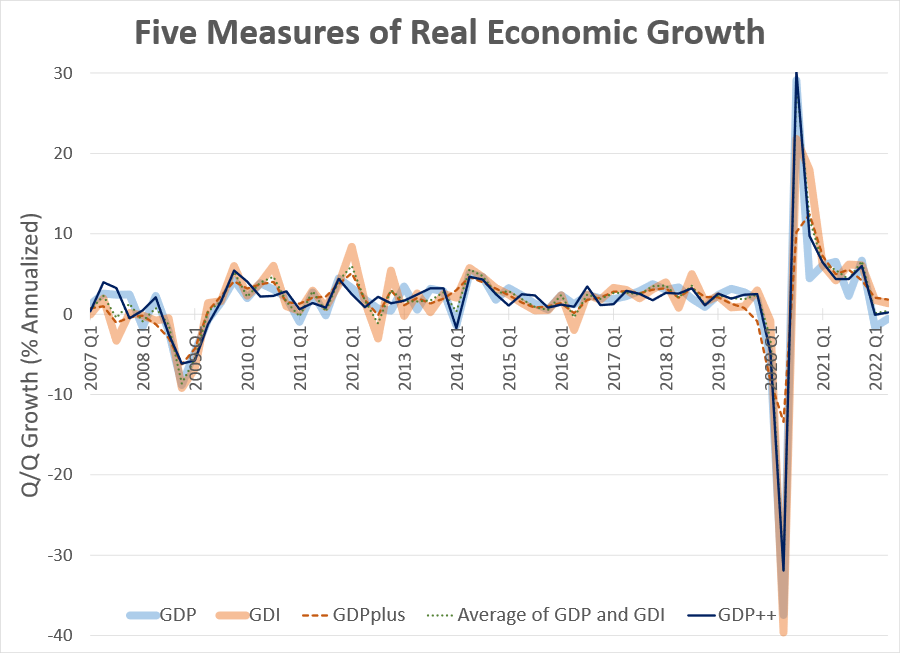

in a recent paper, we show how GDP and GDI revisions over time can be used to help assess how informative each version of these series is and how we should weigh them accordingly. The resulting measure, which we call GDP++tends to be closer than GDP growth GDP plus. It also allows us to place error bands around the estimate. The chart above compares these different growth metrics. It shows that while they’re all highly correlated, the size differences we’ve seen in recent quarters tend to crop up from time to time. The drastic movement in 2020 also highlights a striking feature of GDPplus; it produces a more durable measure of growth and is more resilient to COVID shocks than others.[6]

The second graph shows the same series from Q4 2020. Although the gap between GDP and GDI estimates has widened since the end of 2021, it remains small compared to the gap in the fourth quarter of 2020. By early 2022, GDPplus, GDP++ The averages of GDP and GDI give very similar estimates, but now GDPplus is much higher than the others.gross domestic product++ It is expected to be -0.1% in the first quarter of 2022 and 0.2% in the second quarter, which is in line with estimates of near-zero growth as measured by the BEA average.Perhaps equally important, however, is the statistical uncertainty surrounding GDP++, the 90% error band ranges from -0.9% to 0.7% in the first quarter and -0.6% to 0.9% in the second quarter. In other words, while “headline” GDP seems to suggest that a (mild?) recession has begun, a closer look at its statistical uncertainty shows that these figures are also consistent with only two quarters of weak but sustained growth.

[1] For an in-depth look at revisions to GDP, GDI and their components, see Francis and the Channel’s Fixler (2021).

[2] Look hereTable 7, line 20.

[3] Look hereTable 1, lines 1 and 27.

[4] Another reason is that GDI estimates are only available one to two months after the initial release of GDP.

[5] Look hereTable 1, line 28.

[6] This may also be the reason why it estimates growth in the second quarter of 2022 to be higher than GDI or GDP estimates.

{kind=link}

{kind=link}