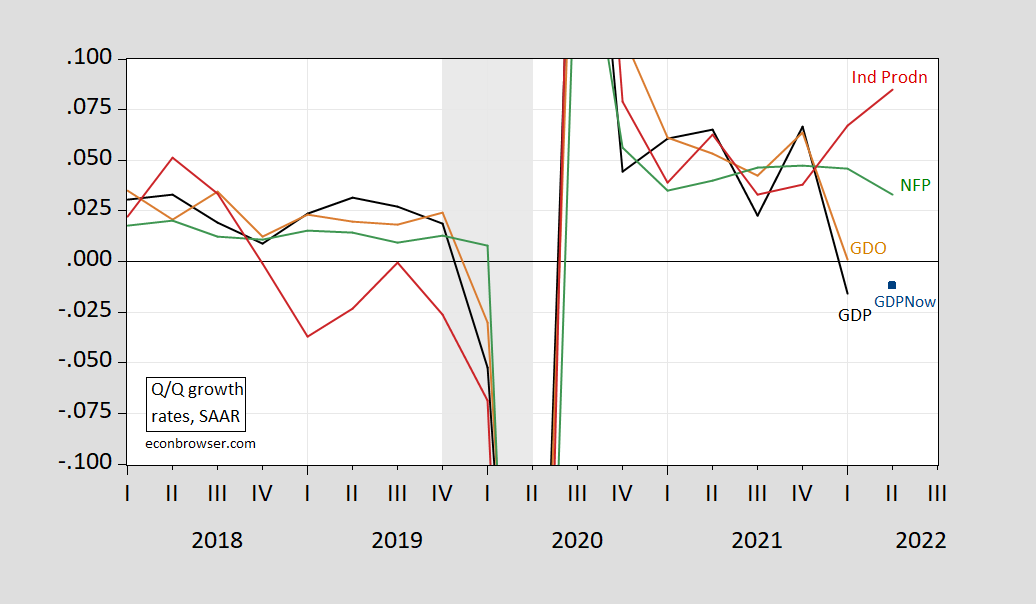

First, compare nonfarm employment and industrial production with GDP (and GDO):

figure 1: Annualized quarter-to-quarter growth in real GDP (black), GDPNow nowcast of 7/8 (blue squares), real GDO (tan), nonfarm payrolls (green), and industrial production (red), all using log differences Calculate. 2022Q2 industrial production is April, May. The NBER uses shades of grey to define the peak and trough dates of the recession. Source: BEA, BLS, and Federal Reserve via FRED, Atlanta Fed, NBER, and author’s calculations.

In short, both employment and industrial production are growing much faster than reported GDP. If one estimates the relationship between GDP (first log difference) on the one hand and non-farm employment and industrial production on the other (1986-2022Q1, adj.R2 = 0.83), one finds that the forecast GDP for the first quarter is 1.8 percentage points higher than the actual report released for the third time. Similar numbers apply to GDPNow data for the second quarter ended July 8.

Note that for the period ending 2018, the average absolute revision of the SAAR growth rate between the third edition and the final year was 1.23 percentage points (Bank of East Asia (2021)).

{kind=link}

{kind=link}