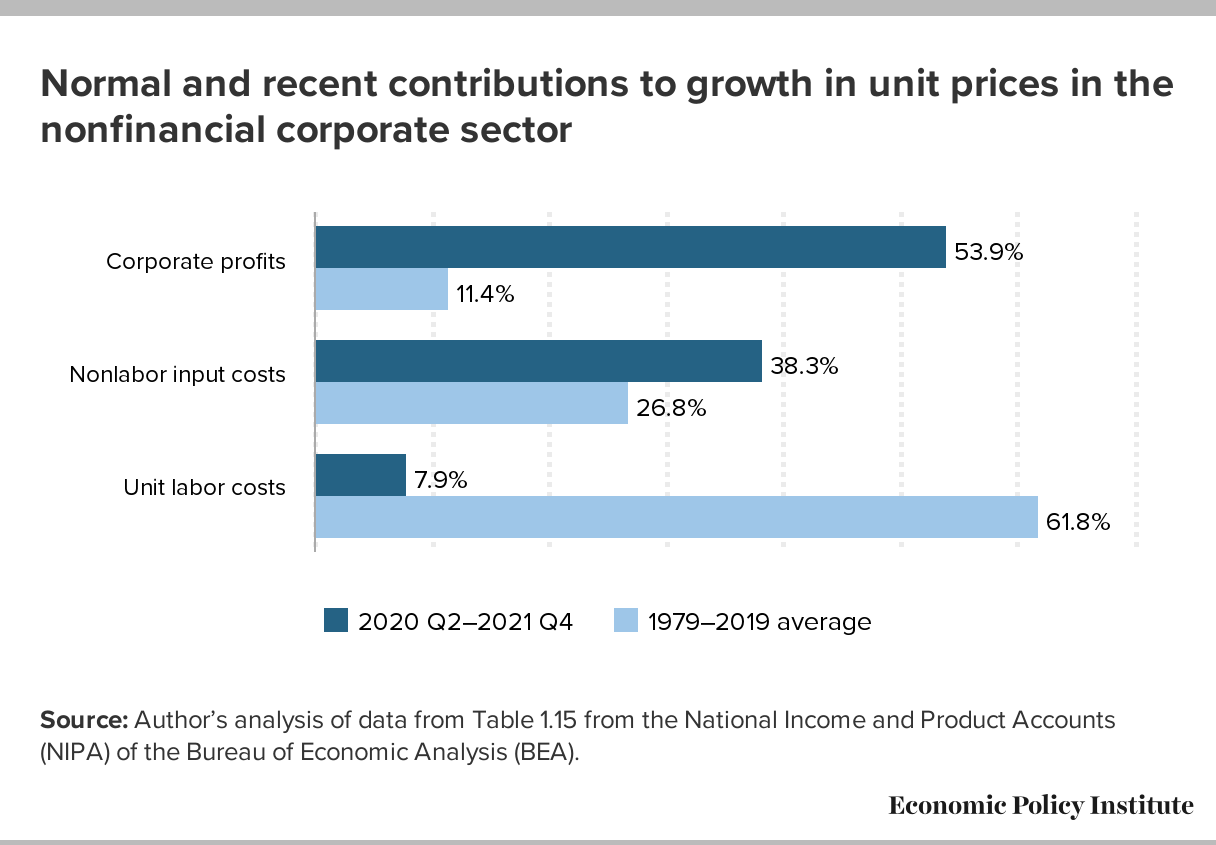

Josh Bivens of EPI It has recently been proposed to decompose price changes into changes attributable to price-cost margins (i.e. approximate profits), labor and non-labor input prices, namely:

source: EPIApril 2023.

former fed governor brainard also Paul Krugman commented on this price-price spiral (although I think the latter is mostly less explicit about whether he thinks this constitutes an inflationary impulse).

While disaggregation is interesting (it is disaggregation after all), I’m not sure what Bivens is making is an argument that isn’t demand pressure (aka overheating). While in very early NK models the elasticity of demand for differentiated goods was constant across the business cycle, and thus the price-cost margin was constant, more recent work (eg, Nakardo and Ramey, JMCB 2020) point out that, depending on the type of shock, the rate of profit can be procyclical.

It may be useful to consider price changes in the presence of stickiness. When inflation is fast, the deviation from the optimal price at any given time between price resets will be greater, leading to a greater loss of profit. Assuming that expected inflation in the current event occurs faster than in previous periods, this implies that firms reset prices faster in larger increments. From this perspective, I might expect a larger mechanically defined contribution to profits, especially if the company overestimates inflation.

The preceding arguments rely on Calvo’s pricing perspective. If price changes are staggered, an alternative explanation is that strategic complementarity that slows price adjustments during periods of low inflation is weakened when firms agree on faster inflation rates.

These are not strict (i.e. general equilibrium) arguments for a higher rate of profit; they simply express our uncertainty about whether the higher rate of profit is due to higher aggregate demand.

How fast is the company CEO expecting inflation? Coibion and Gorodnichenko Provide answers in their survey of firm inflation expectations.

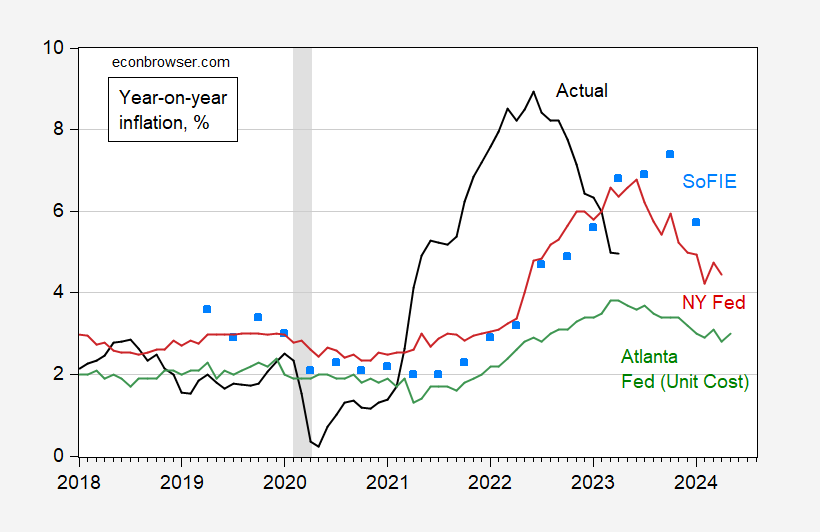

figure 2: Actual CPI inflation, y/y (black), New York Fed’s consumer inflation expectations for the year ahead (red), Atlanta Fed’s unit cost inflation for the year ahead (green), and firm expectations for year-ahead inflation ( azure square), all in %. Dates of peak-to-trough recessions as defined by the NBER are shaded in gray. Source: U.S. Bureau of Labor Statistics, the fed, Federal Reserve Bank of Atlanta, Kobion GorodnichenkoNBER and author’s calculations.

Our last look at firm expectations is the January 2023 forecast for January 2024 year-over-year inflation. Interestingly, in the November and January surveys, firm expected inflation beat consumer expectations (which in turn beat economists’ expectations). In other words, companies expect inflation to rise rapidly (although not as quickly as it actually turned out, but until April’s numbers). Note that the Atlanta Fed’s measure of expected unit cost inflation is different from its sample of corporate inflation, so direct comparisons are not possible.

None of the above is to say that the profits currently enjoyed by businesses are “good”. Instead, I’d just say that it’s not clear whether a demand shock can be inferred from margins to drive the results.

{kind=link}

{kind=link}